- Weekly global market focus

- US/Chinese trade talks hinge on top-level meetings this month

- Strong U.S. economic data causes the markets to turn a bit less dovish on Fed policy

- Q4 earnings are coming in strong but market is looking ahead to earnings downshift in 2019

Weekly global market focus — The U.S. markets this week will focus on (1) the US/Chinese trade talks with only 3-1/2 weeks left until the March 1 deadline, (2) whether there will be another U.S. government shutdown when the current continuing resolution expires next Friday (Feb 15), (3) four appearances by Fed officials this week and further analysis of the Fed’s interest rate pause after last Friday’s stronger-than-expected U.S. payroll and ISM manufacturing data, (4) this week’s $84 billion quarterly refunding operation of 3-year, 10-year and 30-year securities, (5) another busy earnings week with 96 of the S&P 500 companies scheduled to report, and (6) oil prices as the markets continue to watch U.S. pressure on Venezuela’s Maduro regime.

In Europe, the focus will be on any Brexit progress and on Thursday’s Bank of England meeting. The BOE at its meeting on Thursday is unanimously expected to leave its policy unchanged as it waits to see if there will be a no-deal Brexit disaster on March 29. The European Commission on Thursday will release its latest economic forecasts for the Eurozone countries, which are likely to highlight the recent Eurozone economic weakness in which Italy saw a technical recession and Eurozone Q4 GDP was weak at only +0.2% q/q (+0.8% annualized).

UK Prime Minister May this week will continue to pester EU to relent on the Irish border backstop after Parliament last Tuesday voted for a revised Brexit separation plan calling for “alternative arrangements” for the Irish border. The EU has so far flatly rejected Ms. May’s efforts to water down the Irish backstop. There are now only 7-1/2 weeks until the March 29 Brexit deadline. The betting odds are currently at 33% that the UK will leave the EU with no deal by April 1.

The Asian markets will be quiet this week with market closures for the Lunar New Year. The Chinese markets are closed all week and the Hong Kong markets will be closed on Monday through Thursday. The Bank of Australia at its policy meeting on Tuesday is expected to leave its key interest target rate unchanged at 1.5%. The Reserve Bank of India at its meeting on Thursday is expected to adopt a more dovish policy and there is even a chance for an interest rate cut.

US/Chinese trade talks hinge on top-level meetings this month — The markets are waiting for details on the next top-level meetings on the US/Chinese trade talks. USTR Lighthizer and Treasury Secretary Mnuchin are expected to travel to China within the next two weeks for another round of high-level talks. The big question is whether there will be a definitive meeting scheduled for Presidents Trump and Xi in late February. The South China Morning Post on Saturday reported that a Trump-Xi meeting is being considered for February 27-28 in Da Nang, Vietnam to coincide with Mr. Trump’s expected summit in late February with North Korean leader Kim Jong Un.

The definitive scheduling of a Trump-Xi meeting would be a favorable sign since neither of the leaders would presumably want to show up for a meeting that ends in failure. There are still many issues outstanding, which means that a complete US/Chinese trade agreement before the March 1 deadline seems unlikely, although the markets will be happy if there is at least enough progress that President Trump extends the March 1 deadline by another few months.

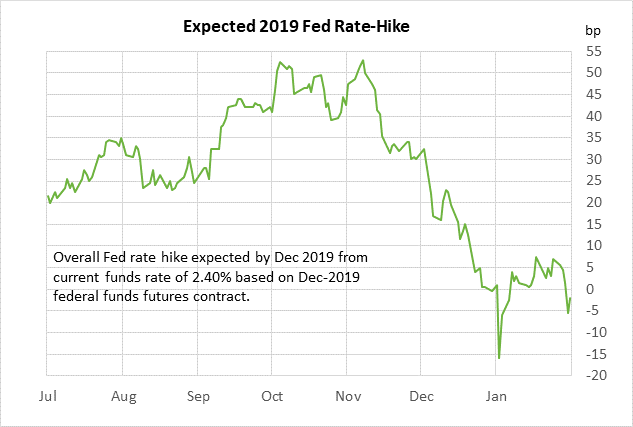

Strong U.S. economic data causes the markets to turn a bit less dovish on Fed policy — The federal funds futures curve last Friday turned more hawkish by 3 bp for the end-2019 contracts and by 6 bp for the end-2020 contracts due to the stronger-than-expected Jan payroll report (+304,000) and Jan ISM manufacturing report (+2.3 to 56.6). The stronger reports put the U.S. economy in a stronger light than the Fed likely anticipated when it moved last week to a fully-neutral policy and dropped its reference to continued slow interest rate hikes.

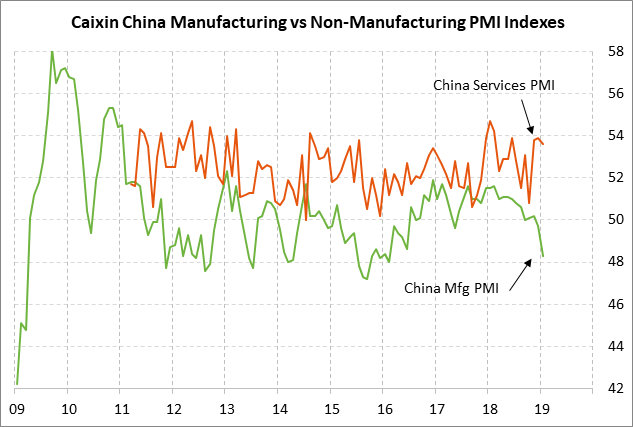

Despite last Friday’s mildly hawkish shift, the market is not expecting a Fed interest rate hike this year and is discounting an 80% chance of a rate cut in 2020. On the global economic front, the markets were somewhat alarmed by last Thursday’s -1.4 point decline in the Jan Caixin China manufacturing PMI index to a 3-year low of 48.3, although Friday’s services PMI fell by only -0.3 points to 53.6.

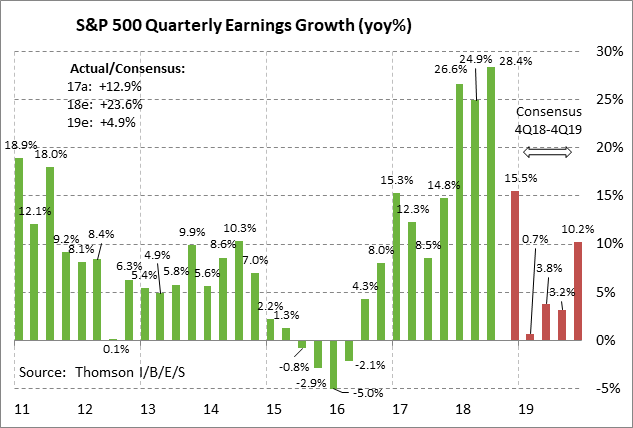

Q4 earnings are coming in strong but market is looking ahead to earnings downshift in 2019 — Q4 earnings season is still in high gear with 97 of the S&P 500 companies reporting this week, although last week’s peak reporting week is now past. Notable reports this week include Alphabet on Monday; Disney and Allstate on Tuesday; GM on Wednesday; and Twitter, Expedia, Yum Brands, and Kellogg on Thursday.

The consensus is for Q4 earnings growth for the S&P 500 companies of +15.5% y/y, according to Thomson Reuters Refinitiv. However, this will be the last quarter of stellar earnings growth stemming from the Jan 1, 2018 tax cut. On a calendar year basis, the market is expecting SPX earnings growth to ease to +4.9% in 2019 from +23.6% in 2018.

Q4 earnings have been favorable with 70.9% of the 234 reporting SPX companies having beaten earnings expectations, above the long-term average of 64% but below the 4-quarter average of 78%, according to Refinitiv. Of reporting companies, 61.5% have beaten revenue expectations, slightly above the long-term average of 60% but below the 4-quarter average of 72%. The markets are on guard for Q4 earnings disappointments tied to various factors including slower growth in China and Europe, higher corporate costs from steel and other tariffs on U.S. imports, and sales shortfalls caused by retaliatory tariffs on U.S. exports.