- ECB meeting expected to have a dovish tone

- Shutdown’s political freeze is slowly thawing

- BOJ leaves policy unchanged but cuts inflation forecast

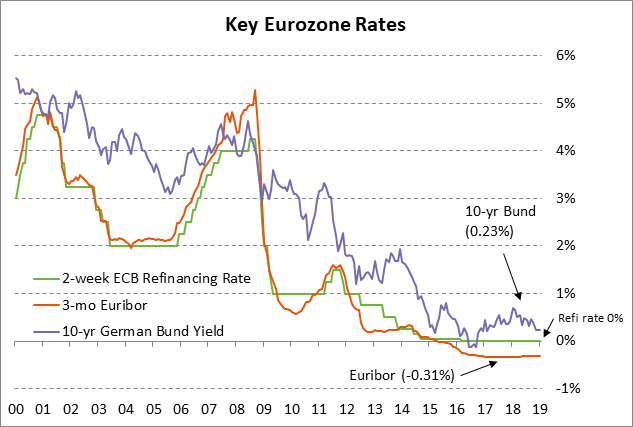

ECB meeting expected to have a dovish tone — The ECB at its meeting today will not make any changes in its key policy variables with the refinancing rate remaining at zero and the deposit rate at -0.40%. However, ECB President Draghi today in his post-meeting conference may acknowledge that the risks are pointing to the downside due to the recent weak Eurozone economic data.

German and Italian GDP were both slightly negative in Q3, raising the risk for a technical recession if either of those countries report another negative GDP figure in Q4. However, the consensus is that the negative one-time factors for Germany and Italy will subside and that growth will resume in 2019. The market consensus is for Eurozone GDP growth to stabilize at +1.3% y/y in Q4-2018 and Q1-2019 after sliding from the stronger rates of +2.2% in Q2-2018 and +1.6% in Q3-2018.

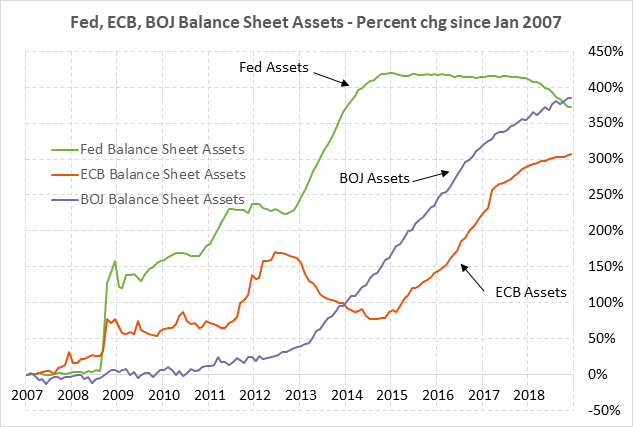

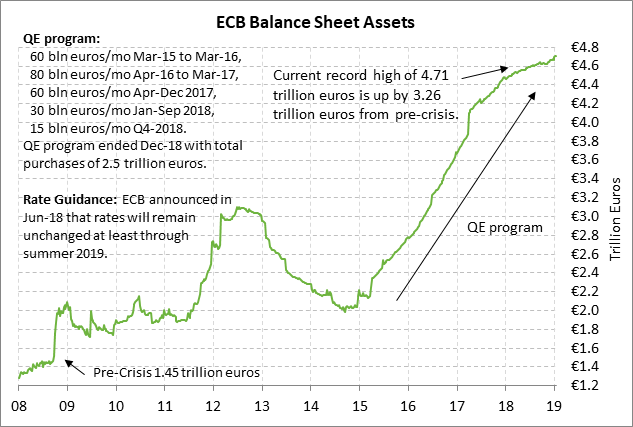

The ECB today is not expected to shift its balance sheet guidance. The ECB’s QE program ended on December 31, but the ECB promised to leave its balance sheet unchanged via reinvestment of maturing securities for an “extended period” past the first rate hike. That could be a matter of 2-3 years considering that the Fed kept its balance sheet unchanged for 3 years after its QE3 program ended.

The ECB today is expected to discuss the roll-over of the targeted longer-term refinancing operation loans (TLTRO II) that the ECB granted to banks starting in June 2016 and that will mature in 2020. The TLTRO-II loans are massive at 489 billion euros, equivalent to nearly 11% of the ECB’s balance sheet. If the ECB does not begin rolling over those loans, then its balance sheet would drop and bank liquidity would tighten up. The market is generally expecting the ECB to make an announcement on new TLTRO operations at its next meeting in March.

The ECB today is not expected to make any major shift in its interest rate guidance. The ECB’s current guidance is that rates will remain low at least through this summer. A recent survey by Bloomberg found a market consensus that the ECB will first raise its current -0.40% deposit rate by 10 bp to -0.30% in October, but will wait for a +25 bp hike in the refinancing rate until March 2020.

Shutdown’s political freeze is slowly thawing — The Senate today is scheduled to vote on two bills that would reopen the government. However, neither of those bills is expected to get the 60 votes necessary for cloture, leaving the bills dead in the water. That would leave the Senate back where it started but with both sides at least clarifying the level of support for their respective positions.

The first bill is President Trump’s proposal for $5.7 billion in wall funding in return for a 3-year extension of protection for DACA dreamers. However, there isn’t likely to be even close to enough Democratic support to get to 60 votes on that bill since the legislation also makes it more difficult for new dreamers to apply for DACA protection and imposes significant new restrictions on asylum. In addition, the Supreme Court on Tuesday refused to take up the current DACA rulings, meaning that DACA dreamers will remain protected by current court rulings at least through the end of this year and that immediate Congressional action to protect them isn’t required.

The second bill is a clean continuing resolution (CR) to temporarily fund the government through February 8 without wall funding. That same bill has already been passed by the House. Senate Democrats will vote in favor of that bill, but the bill is not likely to get enough Republican cross-over support to get to 60 votes. If some miracle occurred and enough Senate Republicans voted in favor of the CR, then the bill would go straight to President Trump for his signature. While that might be somewhat awkward, Mr. Trump has already said that he would veto any bill that doesn’t have his $5.7 billion in wall funding.

While the Senate prepares to take its test votes, there were reports late Wednesday that House Democrats may be ready to offer to raise the level of funding for border security to as much as $5.7 billion from the current level of $1.6 billion, although the building of a wall would still be prohibited. Mr. Trump is not likely to accept that offer. However, the movement on both sides is at least a step in the right direction towards what will inevitably have to be a compromise.

White House economist Hassett on Wednesday said that Q1 GDP could end up being zero if the shutdown lasts through March. Mr. Hassett recently raised his estimate of the shutdown impact to a loss of 0.13 percentage points of GDP per week. That totals up to 0.65 percentage points so far since the shutdown will be 5 weeks old on Friday.

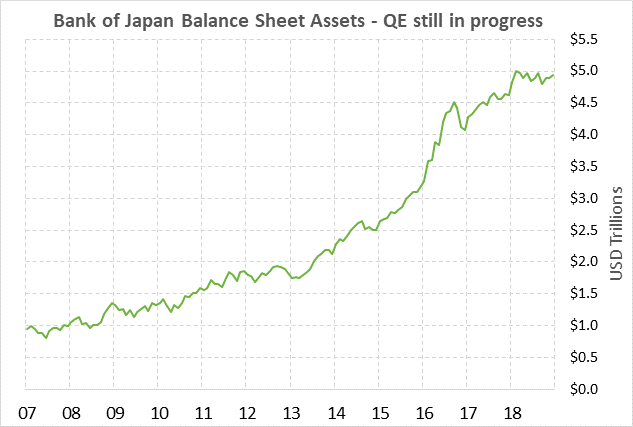

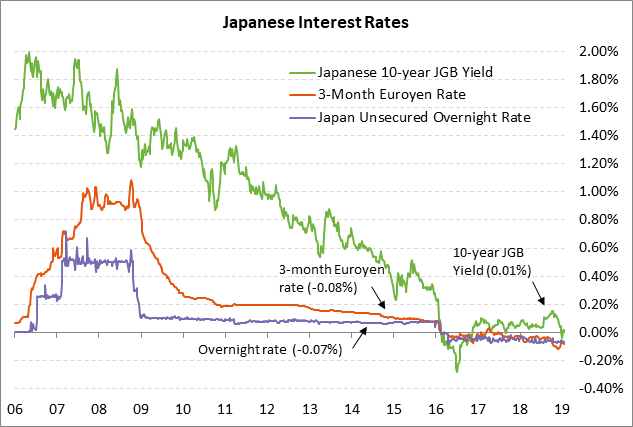

BOJ leaves policy unchanged but cuts inflation forecast — The Bank of Japan at Wednesday’s policy meeting left its key policy variables unchanged with the policy balance rate at -0.10% and its 10-year JGB yield target at zero. The BOJ back in July 2018 expanded the permissible range around the JGB target to +/- 0.20% from +/- 0.10%, which resulted in the 10-year JGB yield rising as high as 0.16% in October 2018. However, the JGB yield has since fallen back to zero due to slower global economic growth and the fall in U.S., European, and Chinese bond yields.

The BOJ on Wednesday cut its FY2019 core CPI forecast to +0.9% from +1.4%, which means the day is even farther away when the BOJ will meet its goal of pushing inflation up to 2.0%. The BOJ is not expected to make any tightening moves ahead of this October when the Japanese government is scheduled to raise the sales tax to 10% from 8%. The BOJ will have to wait until late this year to see if a Japanese recession results from the sales tax hike before it starts to even think about raising interest rates.