- Market reaction to today’s Brexit vote depends on size of the defeat

- U.S. government shutdown continues even as the House votes today on a Feb 1 CR

- PPI expected to be strong and buck other inflation indicators

Market reaction to today’s Brexit vote depends on size of the defeat — The market’s reaction to today’s vote in Parliament on Prime Minister May’s Brexit separation agreement depends mainly on the size of the defeat. The defeat itself is not in question considering that the betting odds are at 99% for a defeat, according to PredictIt.org.

Ms. May could declare somewhat of a victory if her plan to goes down to defeat with a margin of 60 votes or less. In that case, she might still have a chance of getting her plan approved with a repeat vote in Parliament in coming weeks if she can get some additional concessions from the EU and if more members of Parliament view Ms. May’s plan as the only way to avoid a no-deal exit as the March 29 Brexit date approaches.

However, there is talk that Ms. May could go down to defeat with a vote margin of 100-200 votes. A defeat by a margin of 200 votes would be an epic defeat that would normally bring down a government.

The big question is what happens after today’s expected defeat. EU officials are being quoted in the media as saying that they now expect to receive a request from Ms. May for a delay in the Article 50 Brexit deadline from March 29 to perhaps July. That would give Ms. May more time to come up with a plan that could pass Parliament and still avoid a hard border for Northern Ireland.

More drastic outcomes today could be a shock move by Ms. May to resign or call for new elections. Other possibilities include a no-confidence vote in Parliament or a second referendum. However, the more likely outcome is that Ms. May will simply soldier on by trying to get more concessions for Europe and having Parliament vote again on her separation agreement when the threat grows closer to a no-deal Brexit by March 29. If that doesn’t work, she could always ask for a delay in the Brexit deadline later.

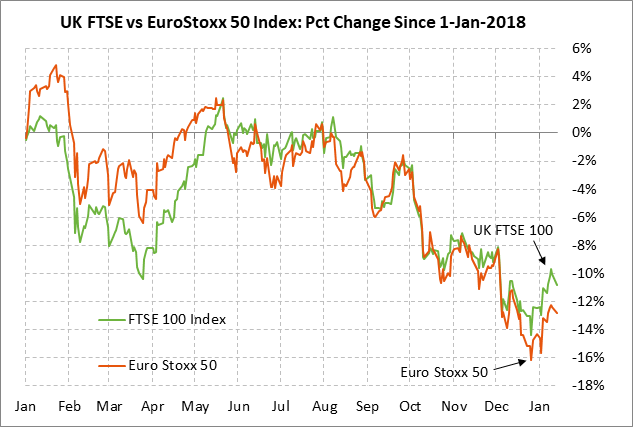

Sterling on Monday rallied to a 2-month high, further recovering from the 1-3/4 year low posted earlier this month. Sterling traders seem ready to take today’s Brexit vote in stride, as long as the loss isn’t by a margin of much more than about 100 members. The FTSE 100 index on Monday closed -0.91% in sympathy with the rest of the global stock markets on the weak Chinese trade data. However, the FTSE-100 has actually done better than the Euro Stoxx 50 index since mid-December, suggesting that stock traders are also taking a rather sanguine view towards Brexit at present.

U.S. government shutdown continues even as the House votes today on a Feb 1 CR — The House today is expected to vote on a continuing resolution (CR) to reopen the government through February 1. The House later this week is then expected to vote on another CR to reopen the government through Feb 28. Senate Majority Leader McConnell will ignore both of these bills since he has said that he will only allow the Senate to vote on a spending bill that is agreed upon by both Democrats and the White House and that can get 60 votes for cloture in the Senate.

Meanwhile, President Trump on Monday quickly shot down Senate Lindsey Graham’s proposal for a 3-week reopening of the government to allow for negotiations on border security. If those negotiations do not produce any funding for a border wall, then Mr. Graham recommended that Mr. Trump at that time could follow through with his threat to declare a national emergency and try to have the military build his wall.

President Trump on Monday said that he is “not looking to declare a national emergency,” repeating his statement last Friday that he is not going to declare an emergency “so fast.” There are various attempts in Congress to come up with a compromise, but so far neither the Congressional Democrats nor President Trump seem willing to compromise. A bipartisan group of Senators including Joe Manchin (D-WVa) were scheduled to meet Monday night to discuss possible solutions.

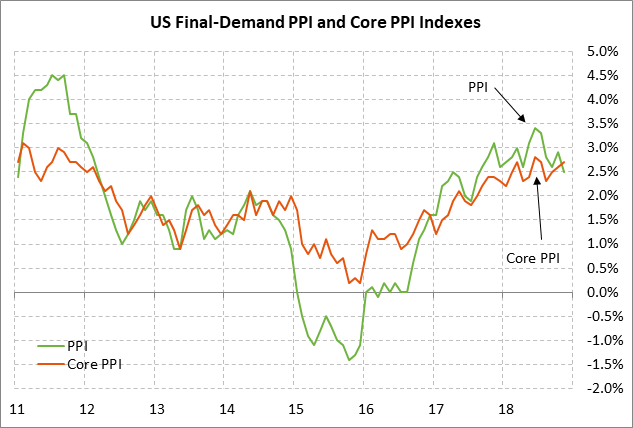

PPI expected to be strong and buck other inflation indicators — The market consensus is for today’s Dec final-demand PPI to be unchanged from Nov at +2.5% and for the core PPI to strengthen to +3.0% y/y from Nov’s +2.7%. Today’s PPI report is not going in the softer direction suggested by the CPI and breakeven rates.

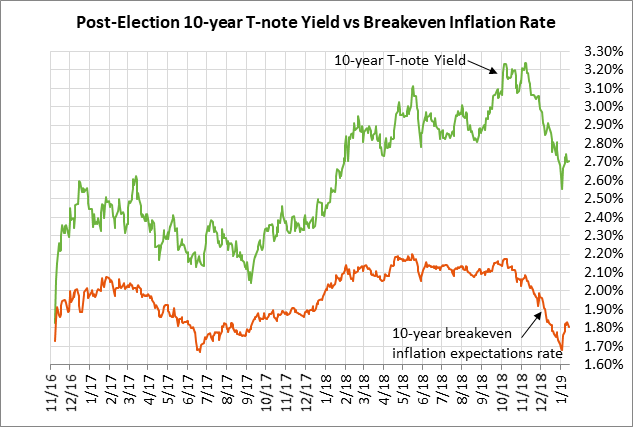

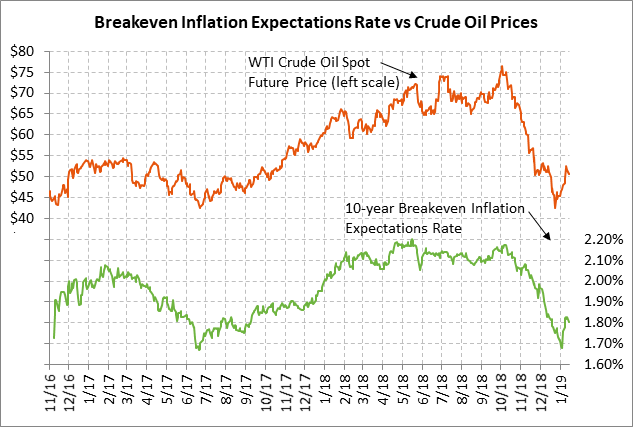

In fact, last week’s Dec CPI index eased to +1.9% y/y from Nov’s +2.2% due to lower oil prices and the core CPI was unchanged at +2.2% y/y. Meanwhile, the breakeven rate illustrates how market expectations for inflation have dropped substantially in recent months. The 10-year breakeven inflation expectations rate has fallen sharply by -38 bp to the current level of 1.83% from last May’s 4-1/4 year high of 2.21%. That shows that 10-year inflation expectations at present are comfortably below the Fed’s 2.0% inflation target.

The decline in the 10-year breakeven rate has been driven in part by weaker U.S. and global economic data but mainly by the sharp drop in crude oil prices. The nearby chart illustrates the clear correlation between oil prices and the 10-year breakeven inflation expectations rate.

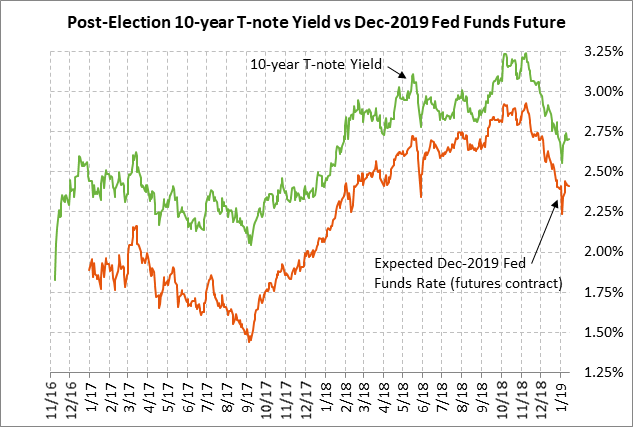

The decline in the breakeven rate has been a key factor causing the sharp drop in the 10-year T-note yield, along with sharply dovish turn in market expectations for Fed policy. The market is now expecting no rate changes by the Fed in 2019 versus expectations as recently as November for a +50 bp rate hike. The 10-year T-note yield in the past 2 months has plunged by -56 bp to the current level of 2.70% from the early-October 7-1/2 year high of 3.26%.