- Today’s Dec FOMC minutes won’t be as dovish as Powell’s recent comments

- 10-year T-note auction to yield near 2.73%

- US/Chinese trade talks reportedly have a long way to go but are making progress

- President Trump calls a third meeting with Congressional leaders

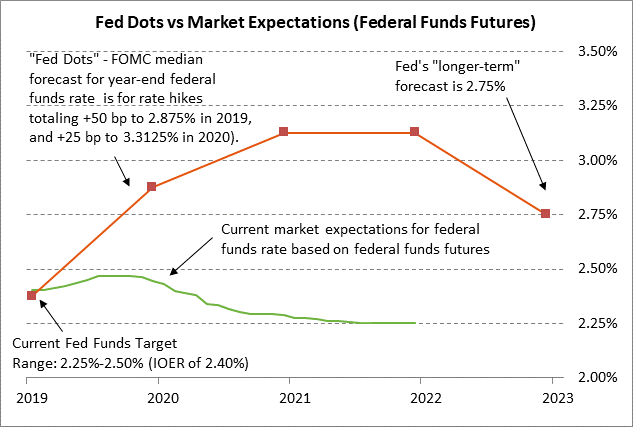

Today’s Dec FOMC minutes won’t be as dovish as Powell’s recent comments — Today’s minutes from the Dec 18-19 FOMC meeting are not likely to show much of a dovish shift among Fed officials. The FOMC at its Dec 18-19 meeting implemented its fourth rate hike of 2018 and issued Fed-dot median forecasts for two more rate hikes in 2019 and one more rate hike in 2020 to a funds rate target range of 3.00%/3.25%.

The FOMC minutes will certainly not go as far as Fed Chair Powell did last Friday when he said that the Fed is listening to the markets and suggested that the Fed might be willing to pause its rate-hike regime. Mr. Powell’s verbal policy capitulation didn’t come until after the Dec 18-19 FOMC meeting and after the negative events in the latter half of December that included (1) weak global economic data, (2) the sharp sell-off in U.S. and global stocks to new lows in late December, (3) the controversy over reports that President Trump wanted to fire Fed Chair Powell, (4) Treasury Secretary Mnuchin’s late-December liquidity welfare check on U.S. large-bank CEOs, and (5) the U.S. government shutdown that started on Dec 22.

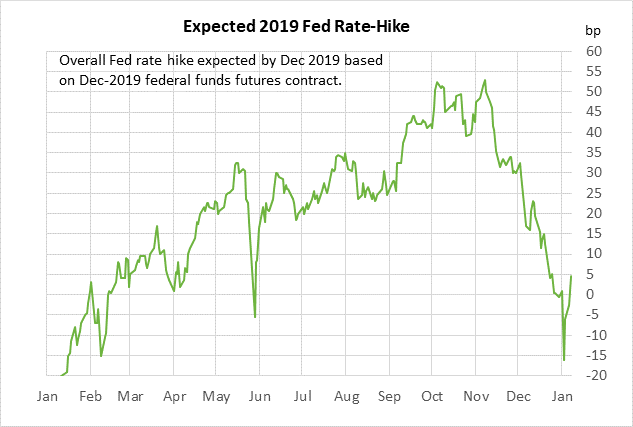

The market has become a little less dovish about Fed policy in the past week due to the upward rebound in the U.S. stock market and some optimism about the US/Chinese trade talks. The Dec 2019 federal funds rate on a yield basis fell to a low of 2.24% last Thursday, reflecting a 64% chance of a 25 bp rate hike this year. However, the Dec 2019 funds rate contract has since rebounded higher to 2.375%, which is only 2.5 bp below the current effective funds rate of 2.40% and indicates that the market is now discounting a 10% chance for a Fed rate cut in 2019. The market is discounting an 84% chance of one -25 bp rate cut by the end of 2020.

While the Fed may be willing to pause its rate hike regime for perhaps the first half of this year, we believe the Fed will still want to eventually raise the funds rate target to at least the 2.75% level that the Fed has pegged as the neutral rate, which is +35 bp higher than the current effective fed funds rate of 2.40%.

10-year T-note auction to yield near 2.73% — The Treasury today will sell $24 billion of 10-year T-notes in the second and final reopening of the 3-1/8% note of November 2028, which was first sold last November. The Treasury will conclude this week’s $78 billion coupon package by selling $16 billion of reopened 30-year T-bonds on Thursday.

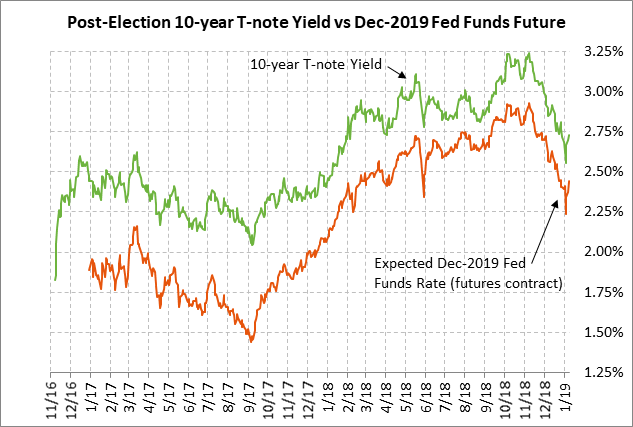

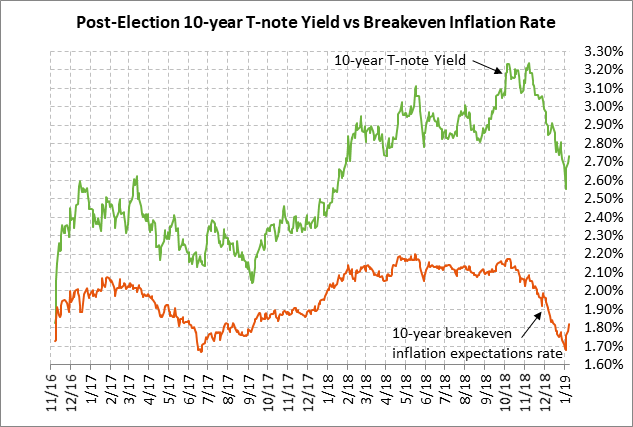

Today’s 10-year T-note issue was trading at 2.73% in when-issued trading late yesterday afternoon, which is up by +19 bp from last Friday’s 1-year low of 2.54%. The 10-year T-note yield has rebounded higher this week due to (1) reduced safe-haven demand as the U.S. stock market rebounds higher and as the prospects improve for a US/Chinese trade deal, (2) a less dovish view of Fed policy, and (3) the +15 bp upward rebound in the 10-year breakeven inflation expectations rate to 1.82% from last Friday’s 1-1/2 year low of 1.67%, mainly because of the $7.50 per barrel rally in Feb crude oil prices seen since late-December.

The 12-auction averages for the 10-year are as follows: 2.51 bid cover ratio, $22 million in non-competitive bids to mostly retail investors, 4.5 bp tail to the median yield, 22.0 bp tail to the low yield, and 31% taken at the high yield. The 10-year is a little above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 64.1% of the last twelve 10-year T-note auctions, mildly above the median of 63.6% for all recent coupons.

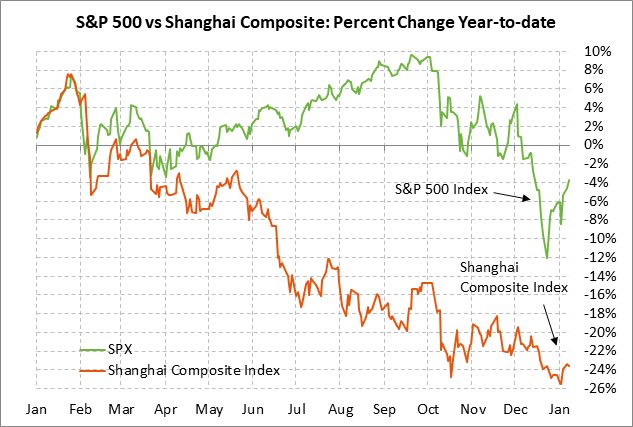

US/Chinese trade talks reportedly have a long way to go but are making progress — The US/Chinese trade talks seem to be going well although the WSJ on Tuesday reported that the two sides are still far from striking a deal. President Trump on Tuesday also fueled some market optimism when he tweeted, “Talks with China are going very well!”

The US/Chinese talks among mid-level officials held on Monday and Tuesday were extended into a third day on Wednesday, which suggested that progress is being made. The next major step is that Chinese Vice Premier Liu, President Xi’s top economic advisor, is due to travel to Washington for talks with USTR Lighthizer later this month. There are only 7 weeks left until the March 1 deadline for the talks, when President Trump has said he will boost the tariff to 25% from 10% on $200 billion of Chinese goods if there is no trade agreement.

We believe the odds have improved significantly for a US/Chinese trade agreement. Chinese officials are under heavy pressure to get a deal since the trade tensions are causing significant stress for the Chinese economy and stock market. Meanwhile, the Trump administration is also under pressure to get a deal due to the U.S. stock market correction and the fact that time is starting to run out for President Trump’s first term.

However, the markets may not get the solid trade deal they are hoping for since there are reports that the U.S. is only considering a phased drawdown of punitive U.S. tariffs on Chinese goods depending on China hitting trade agreement milestones such as U.S. goods purchases and policy changes. That suggests that President Trump may continue to engage in various trade threats against China even after any agreement is reached.

President Trump calls a third meeting with Congressional leaders — President Trump will meet today with Congressional leaders for another negotiating session about the partial U.S. government shutdown. Mr. Trump is due to visit the border on Thursday.