- Weekly market focus

- Trump claims “big progress” on US/Chinese trade deal

- Market adopts pessimistic economic view for 2019 with no Fed rate hikes

- U.S. government shutdown awaits resolution by the new Congress

Weekly market focus — The U.S. markets this week will focus on (1) the prospects for ending the partial U.S. government shutdown when the new Congress takes control on Thursday, (2) US/Chinese trade tensions after President Trump on Saturday said he had a long call with President Xi and that “big progress” is being made on a trade deal, (3) Fed policy and whether the market is right to have reduced the chances for a rate hike in 2019 to nearly zero, (4) any new comments by President Trump about Fed Chair Powell or interest rates, (5) crude oil prices, which stabilized late last week after posting a 1-1/2 year low last Monday, (6) whether the extreme stock market volatility continues this week during the thin holiday markets.

In Europe, the focus will be on the stock market gyrations, today’s official end of the ECB’s QE program, and CPI data late in the week. The markets will watch Italian politics after weekend Italian newspaper reports saying that Finance Minister Tria will resign in January after the torturous process of getting Italy’s 2019 budget approved by the EU.

In Asia, the focus will be whether Chinese stocks can avoid further losses, US/Chinese trade and tech tensions, and Chinese PMI data.

Trump claims “big progress” on US/Chinese trade deal — President Trump on Saturday tweeted that he had a long telephone call with Chinese President Xi and that: “Deal is moving along very well. If made, it will be very comprehensive, covering all subjects, areas, and points of dispute. Big progress being made!”

A U.S. trade delegation of mid-level officials, led by Deputy USTR Gerrish, will travel to Beijing next week for trade talks. Those will be the first face-to-face trade talks since Presidents Trump and Xi on Dec 1 agreed to a 90-day ceasefire, although there have recently been a series of telephone calls about trade. There is little time to lose because the 90-day ceasefire that ends March 1 is already a third over.

The odds for a US/Chinese trade deal seem to have improved because China has taken a number of measures to placate the U.S. such as buying U.S. soybeans and LNG, passing stronger IP enforcement penalties, dropping the penalty tariff on U.S. autos, implementing a third round of cuts in import and export tariffs in an economy-opening initiative, and expressing some willingness to water down its “Made in China 2025” industrial program.

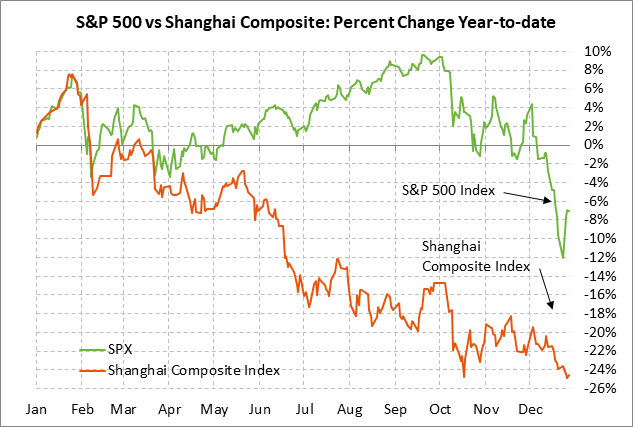

Meanwhile, the Trump administration’s hand has weakened due to December’s sharp sell-off in the U.S. stock market. Since Dec 1, the S&P 500 index has fallen by -9.9%, which is significantly more than the -3.6% sell-off in the Shanghai Composite index over the same period.

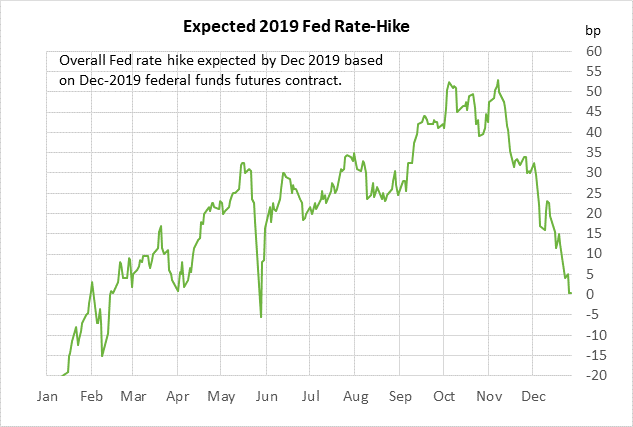

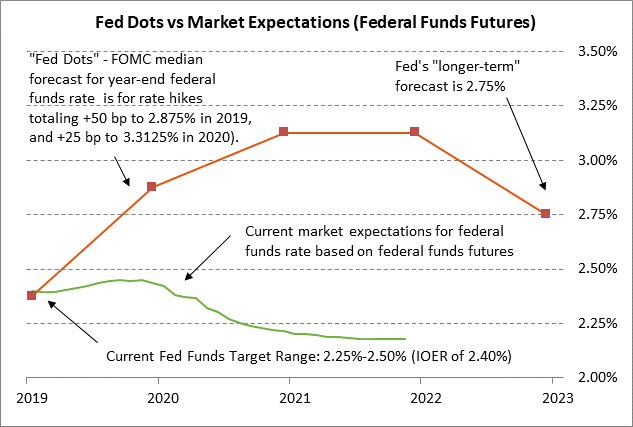

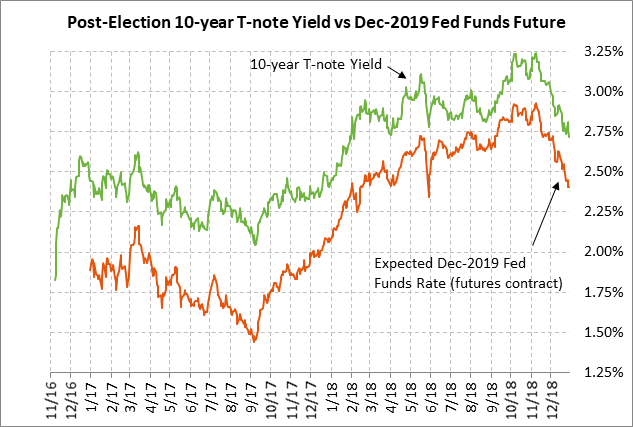

Market adopts pessimistic economic view for 2019 with no Fed rate hikes — The federal funds futures market last week reduced expectations for a rate hike in 2019 to nearly zero due to December’s sharp stock market correction and talk about a recession. The Dec 2019 federal funds futures contract is discounting only a +0.5 bp higher funds rate versus the current effective funds rate of 2.40%, which translates to a 2% chance for a rate hike in 2019. Not only is the market expecting no rate hikes in 2019, the market is also discounting the possibility of a rate cut in 2020.

By contrast, the Fed-dots are still forecasting two rate hikes in 2019 and one rate hike in 2020, which is far more hawkish than the market. The Fed will not halt its rate-hike regime just because of weakness in the stock market, which was likely caused in part by heavy year-end liquidation by investors. For the Fed to halt its rate hike regime, the U.S. economy would have to weaken to a GDP rate of well below the potential rate of +1.9%. At this point, the market consensus is still for U.S. GDP growth to remain solid at +2.6% in 2019 and +1.9% in 2020.

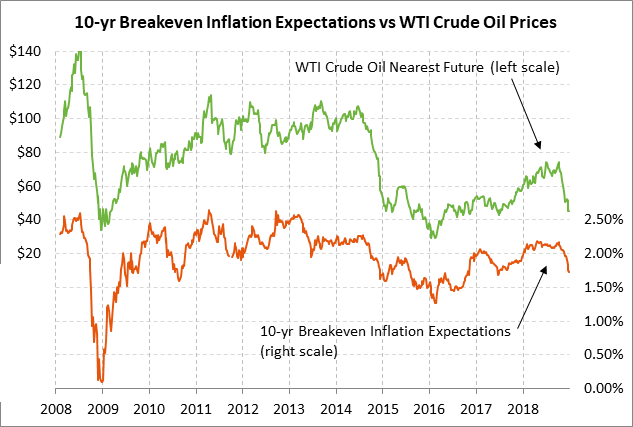

The Fed would also need to see the core PCE deflator ease to at least +1.5% y/y from the current level of 1.9%. The U.S. 10-year breakeven inflation expectations rate has plunged by 44 bp in the past 2-1/2 months to last week’s 1-1/2 year low of 1.73%. However, the breakeven rate has fallen mainly because of the plunge in oil prices and it is doubtful that the core PCE deflator will fall by as much as the breakeven rate, thus keeping the Fed on its toes about inflation.

U.S. government shutdown awaits resolution by the new Congress — The U.S. government has been partially shut down since the continuing resolution expired on Dec 21. The markets are not expecting any movement at least until the new Congress begins this Thursday at noon.

The new Democratically-controlled House on Thursday is expected to first vote for Nancy Pelosi as the new Speaker. The Democrats then have several bills they want to pass right off the bat, one of which being new spending authority to reopen the government. Democratic leaders are reportedly considering passing three different types of spending bills late this week. None of those bills will include any funding for President Trump’s wall, although the bill will likely include the $1.3 billion in border security that was included in the previous bipartisan continuing resolution.

Once the House passes its funding bill, then the ball will be in Senate Majority Leader McConnell’s court. Mr. McConnell has said that the Senate will not vote on a bill until there is a bipartisan agreement between the White House and Democrats that can get 60 votes in the Senate for cloture. At some point, either the White House or Congressional Democrats, or both, will have to blink in order to reopen the government. In the meantime, the partial U.S. government shutdown is putting a dent in the U.S. economy and is undercutting investor confidence.