- US/Chinese trade talks so far remain on track despite Huawei flap

- PM May tours Europe desperately seeking Brexit concessions

- U.S. headline CPI expected to edge lower

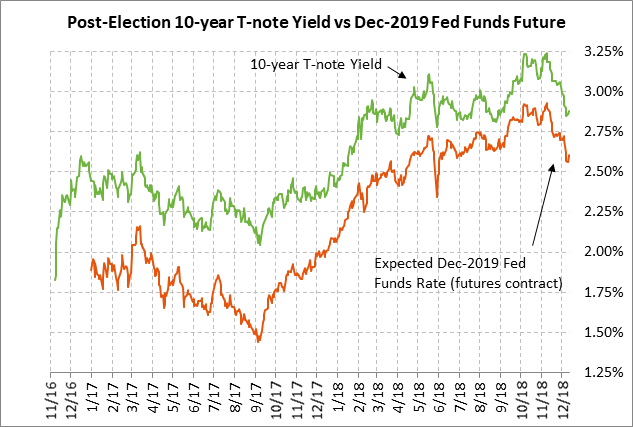

- 10-year T-note yield calms down after sharp drop

- 10-year T-note auction to yield near 2.86%

US/Chinese trade talks so far remain on track despite Huawei flap — U.S. and Chinese officials on Tuesday made a point of showing that the US/Chinese trade talks remain on track and have not been canceled over the US/Canadian arrest of Huawei CFO Meng. Chinese Vice Premier Liu He, U.S. Treasury Secretary Mnuchin and USTR Lighthizer spoke by phone late Monday and discussed the timetable and road map for the US/Chinese trade talks.

In other good US/Chinese trade news, China’s cabinet over the next few days will consider cutting the tariff on U.S. cars to 15% from 40%, thus removing the 25% retaliatory tariff. That unilateral tariff cut should please Mr. Trump, who has a particular interest in promoting U.S. autos. The markets are also waiting to see if China will eliminate its retaliatory 25% tariff on U.S. soybeans since China promised at the Dec 1 meeting to immediately start buying U.S. soybeans.

China on Tuesday detained a former Canadian diplomat, Michael Kovrig, who is now an employee of the International Crisis Group. There was speculation that his detention might be retaliation for Canada’s arrest of Huawei CFO Meng. If so, that could mean that China plans to respond in kind to the arrest of business executives and not let the Huawei flap derail the US/Chinese trade talks. Ms. Meng was at least granted bail late Tuesday, although she must remain in Canada for extradition hearings to the U.S. for alleged fraud charges relating to violating Iran sanctions.

PM May tours Europe desperately seeking Brexit concessions — Prime Minister May is on a tour of Europe trying to get some relief on the Irish backstop that has attracted so much opposition in Parliament. Ms. May hopes to attend the EU Summit that begins on Thursday and that will have a session covering Brexit.

The EU insists that there will no relief from the current Irish backstop except for non-binding assurances that the EU does not want the UK to end up in the backstop forever. Ms. May still plans on holding a vote in Parliament on her Brexit withdrawal plan by January 24 with whatever small improvements she can extract from the EU. Meanwhile, businesses in the UK are starting to prepare for the increased likelihood of a no-deal Brexit, which will increase migration out of the UK and reduce investment in the UK.

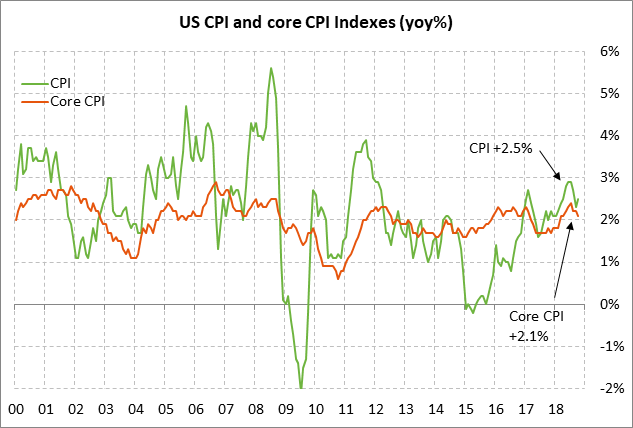

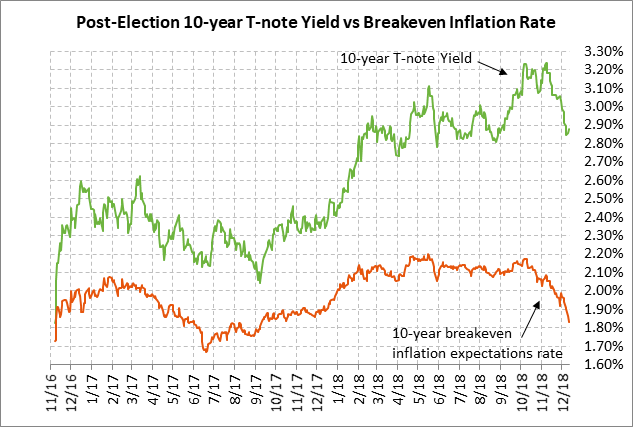

U.S. headline CPI expected to edge lower — The market consensus is for today’s Nov CPI to ease to +2.2% y/y from Oct’s +2.5% but for the Nov core CPI to rise slightly to +2.2% from Oct’s +2.1%. The headline CPI is expected to ease largely due to the plunge in oil prices in October and November.

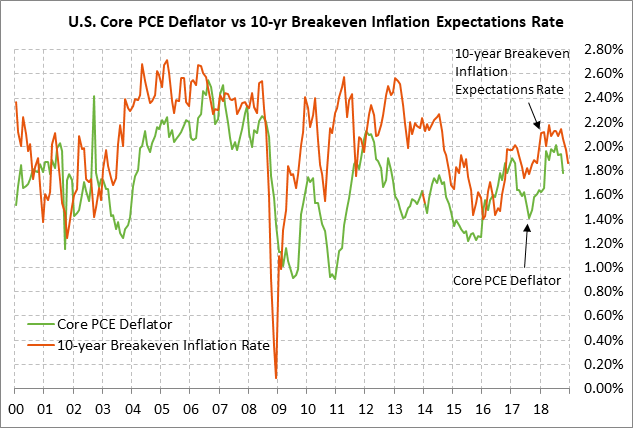

The market’s worries about inflation have eased substantially in the past two months. The 10-year breakeven inflation expectations rate on Tuesday fell to a new 14-month low of 1.83%. The rate has now plunged by -38 bp from May’s 4-1/4 year high of 2.21%. That sharp drop gives the Fed some room to pause its rate-hike regime in 2019 since inflation is currently on its way lower.

The PCE deflator, the Fed’s preferred inflation measure, has also moderated in recent months, signaling that the actual inflation figures are moving lower as well as inflation expectations. The core PCE deflator in October fell to an 8-month low of +1.8% from the 6-year high of +2.0% posted earlier this year in May-July. The headline PCE deflator fell to an 8-month low of 2.0% in Sep-Oct from the 6-year high of +2.3% posted earlier this year in May-July. The recent weakness in the deflator is particularly seen by the fact that the core PCE deflator in October fell to a 1-1/2 year low of +1.1% on a 3-month annualized basis.

10-year T-note yield calms down after sharp drop — The 10-year T-note yield in the past 5 weeks plunged by an overall -43 bp to Monday’s 3-1/2 month low of 2.82% but then rebounded higher to 2.86% by Tuesday as stocks recovered.

The plunge in the 10-year T-note yield has been due to (1) the drop in market expectations to only one Fed rate hike in 2019 from two rate hikes, (2) the sharp drop in inflation expectations due largely to the plunge in oil prices, (3) softer global economic growth, and (4) safe-haven demand tied to the stock market correction, US/Chinese trade and tech tensions, Brexit, the EU-Italian budget standoff, and the Mueller investigation.

10-year T-note auction to yield near 2.86% — The Treasury today will sell $24 billion of 10-year T-notes in the first reopening of last month’s 3-1/8% 10-year note of Nov 2028. The $24 billion size of today’s sale is up by $1 billion from the $23 billion size seen at the last reopenings in Sep-Oct and is up by $4 billion from the $20 billion size that prevailed in 2016/17. The Treasury will then conclude this week’s coupon package by selling $16 billion of 30-year T-bonds on Thursday.

The 12-auction averages for the 10-year are as follows: 2.51 bid cover ratio, $22 million in non-competitive bids, 4.5 bp tail to the median yield, 19.4 bp tail to the low yield, and 37% taken at the high yield. The 10-year is slightly above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 63.6% of the last twelve 10-year T-note auctions, which is slightly above the median of 63.2% for all recent coupon auctions.

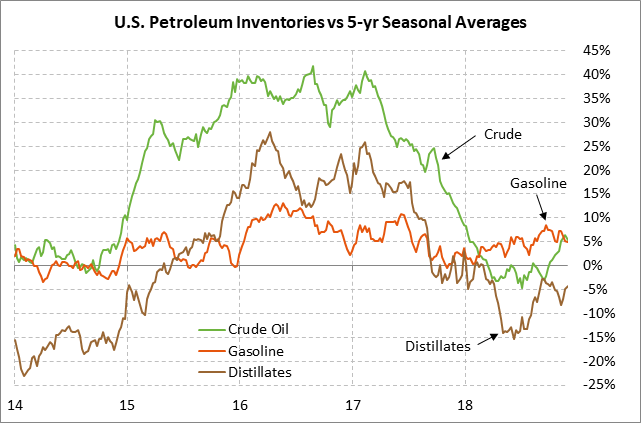

EIA report — The consensus for today’s EIA report is for a -3.5 mln bbl decline in U.S. crude oil inventories, a +2.0 mln bbl rise in gasoline inventories, and a +1.6 mln bbl rise in distillate inventories. U.S. crude oil inventories are currently +5.4% above the 5-year seasonal average, gasoline inventories are 4.9% above average and distillates are -4.3% below avg.