- US/Mexico trade agreement is a step in the right direction but Canadian fallout is possible by Friday

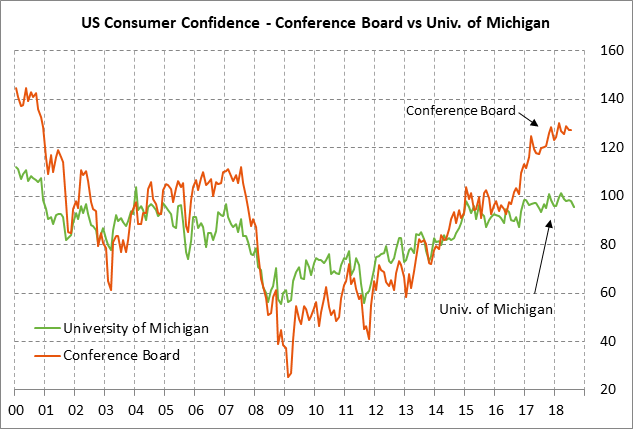

- U.S. consumer confidence expected to dip

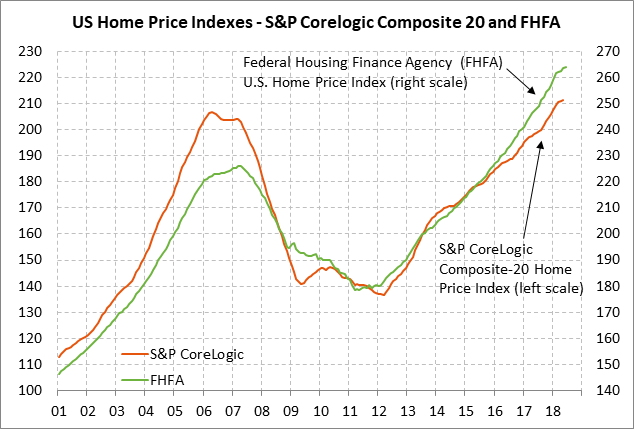

- U.S. home prices could soon start leveling off

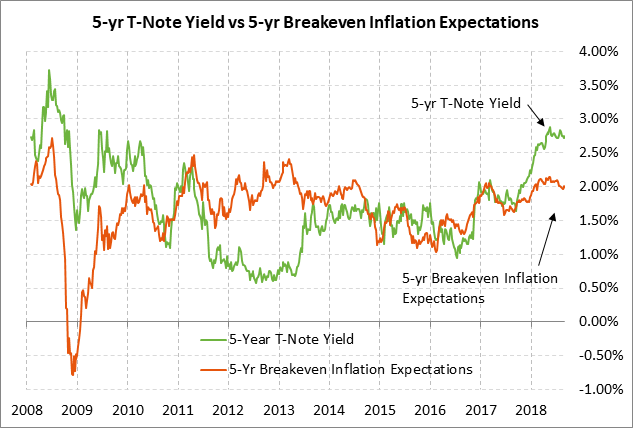

- 5-year T-note auction to yield near 2.74%

US/Mexico trade agreement is a step in the right direction but Canadian fallout is possible by Friday — The U.S. and Mexico yesterday agreed on a trade pact, which was clearly a positive development. The US/Mexico agreement is the Trump administration’s second trade agreement following the revamp of the US/South Korea free trade agreement.

However, it remains unclear whether yesterday’s new US/Mexico agreement will be approved and finalized by the Mexican and U.S. legislatures. The first problem is that the U.S. is trying to force Canada to agree to the new US/Mexico NAFTA terms by Friday. A deal by Friday is necessary so that the Mexican legislature has the sufficient 90-day notice to approve the deal before Mexico’s new president takes over in December. The new Mexican president will likely want to revise the US/Mexican trade agreement if it isn’t finalized by the time he takes power.

President Trump yesterday said that if Canada doesn’t agree to the revised US/Mexico NAFTA deal by Friday, then the agreement will simply become the US/Mexico trade agreement and the U.S. will then negotiate a separate bilateral trade agreement with Canada. However, it remains unclear whether the U.S. Congress would go along with the idea of dropping the trilateral NAFTA framework and going with separate US/Mexico and US/Canadian agreements.

The markets reacted favorably to Monday’s US/Mexico trade deal. The S&P 500 index rallied to a new record high and closed the day up +0.77%. The Mexican peso rallied by +0.77% and the S&P/BMV Mexican stock index (MEXBOL) rallied by +1.58%.

While the markets are pleased that the US and Mexico agreed to a trade deal, the markets are also well aware that there are plenty of landmines that could still sink the deal. Until both Mexico and Canada are locked into a new trade deal, the markets will remain cautious.

The markets during the remainder of this week will be carefully watching Canada’s reaction. Canadian Foreign Minister Chrystia Freeland is due to arrive in Washington on Tuesday for trade talks. The bad news is that if Canada doesn’t agree to the US/Mexico NAFTA terms by Friday, President Trump may be ready to formally announce a U.S. exit from NAFTA and perhaps also launch a new trade assault on Canada. President Trump on Monday issued an explicit threat against Canada by saying that, “I think the easiest thing is to tariff their cars.” White House economic advisor Kudlow reinforced Mr. Trump’s threat by saying that if a US/Canadian trade deal isn’t reached “we might have to resort to auto tariffs.”

U.S. consumer confidence expected to dip — The market consensus is for today’s Aug Conference Board U.S. consumer confidence index to show a -0.8 point decline to 126.6, more than reversing July’s small +0.3 point increase to 127.4. The U.S. consumer confidence index remains generally strong at only 2.6 points below February’s 17-3/4 year high of 130.0. However, the University of Michigan has already reported its consumer sentiment index for August and its index fell by -2.6 points to a an 11-month low of 95.3, which did not bode well for today’s Conference Board report.

U.S. consumer sentiment is seeing support from (1) the strong economy and labor market, (2) rising wages and income, and (3) rising household wealth due to strong housing prices and stock prices. Negative factors include (1) Washington political uncertainty, (2) tariffs, and (3) high gasoline prices.

U.S. home prices could soon start leveling off — The market consensus is for today’s June S&P CoreLogic composite-20 home price index to show an increase of +0.2% m/m and +6.4% y/y following May’s report of 0.2% m/m and +6.5% y/y. Expectations for today’s Composite-20 index are supported by last week’s news that the FHFA home price index for June rose by +0.2% m/m and +6.5% y/y.

U.S. home prices marched higher through May due to strong demand and tight supplies. Indeed, the Composite-20 index is currently up by +6.5% y/y and by a total of +54% from the housing-bust trough. However, home prices could start plateauing due to a slowdown in home sales and higher mortgage rates. Existing home sales have fallen during the last four months (April-July) by a total of -4.7% and sales were down by -1.5 y/y in July. Meanwhile, the current 30-year mortgage rate of 4.51% is only 15 bp below May’s 7-1/4 year high of 4.66% and is up by about +70 bp from the 3.80% level seen as recently as last autumn.

5-year T-note auction to yield near 2.74% — The Treasury today will sell $37 billion of 5-year T-notes. The $37 billion size of today’s 5-year T-note is up by $1 billion from the $36 billion size seen in May-July and is up by $3 billion from the $34 billion size that prevailed during 2016-17. The Treasury will conclude this week’s $121 billion T-note package by selling $31 billion of 7-year T-notes and $17 billion of 2-year floating-rate notes on Wednesday.

Today’s 5-year T-note issue was trading at 2.74% in when-issued trading late yesterday afternoon. The 5-year yield has been moving sideways in the narrow 20 bp range of 2.69%-2.89% since early June and is currently only 21 bp below May’s 9-1/4 year high of 2.95%.

The 12-auction averages for the 5-year are as follows: 2.50 bid cover ratio, $58 million in non-competitive bids to mostly retail investors, 4.3 bp tail to the median yield, 21.7 bp tail to the low yield, and 49% taken at the high yield. The 5-year is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 63.1% of the last twelve 5-year T-note auctions, which exactly matches the median for all recent Treasury coupon auctions.