- Congressional leaders meet today to avert a U.S. government shutdown in two weeks

- FOMC minutes will be gauged for hawkishness as inflation expectations move to new 9-1/2 month high

- U.S. ISM manufacturing index expected to remain strong

- U.S. vehicle sales expected to close the year on a strong note

- German coalition talks begin

Congressional leaders meet today to avert a U.S. government shutdown in two weeks — The “Big Four” congressional leaders (Ryan, Pelosi, McConnell, Schumer) are scheduled to meet today with White House officials on the topic of preventing a government shutdown and resolving immigration issues. White House officials attending the meeting will include legislative affairs director Marc Short and budget director Mick Mulvaney. Congress has only 16 days to pass new spending authority and prevent a government shutdown when the current continuing resolution expires on Jan 19.

There is the distinct threat of a government shutdown this time around since Republicans and Democrats are at loggerheads on a range of issues including top-line funding for defense and non-defense spending, a dreamer solution, border wall funding, the bipartisan Obamacare fix that was promised to Senator Collins, an extension of foreign surveillance authority, disaster relief, and other issues.

Regarding the larger 2018 Republican legislative agenda, President Trump is scheduled to meet with House Speaker Ryan and Senate Majority Leader McConnell at Camp David this coming weekend (Jan 6-7). President Trump reportedly wants to move ahead with an infrastructure bill and Speaker Ryan’s plan for cutting welfare and entitlements. House-Senate Republicans will hold their annual policy retreat starting on Jan 31 at The Greenbrier for a larger discussion on the Republican agenda.

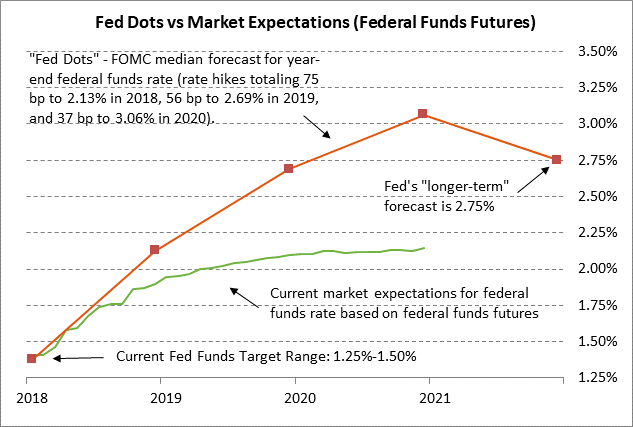

FOMC minutes will be gauged for hawkishness as inflation expectations move to new 9-1/2 month high — The FOMC today will release the minutes from its Dec 12-13 meeting. The FOMC at that meeting met unanimous market expectations by raising the funds rate target range by +25 bp to 1.25%-1.50%. The December rate hike made good on the FOMC’s forecast for three rate hikes in 2017. The FOMC is forecasting another three rate hikes in 2018, which is more hawkish than market expectations for only two rate hikes.

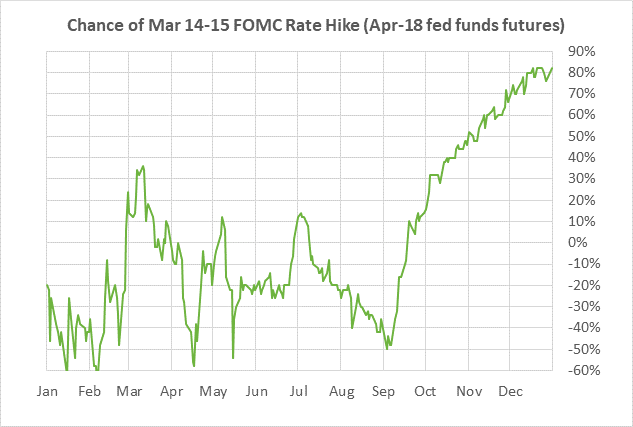

The market is forecasting a minimal 14% chance of a rate hike at the next FOMC meeting on Jan 30-31 but then a fairly strong 76% chance of a rate hike at the following meeting on March 20-21. The market is fully expecting the FOMC to implement that first rate hike of 2018 by the May 1-2 FOMC meeting.

The markets will carefully dissect today’s FOMC minutes to gauge the strength of the Fed’s intention to raise interest rate three times in 2018 to a new target range of 2.00%-2.25%. We expect the Fed to make good on its 2018 rate-hike intentions in order to at least get the funds rate above inflation expectations and do away with a negative real federal funds rate.

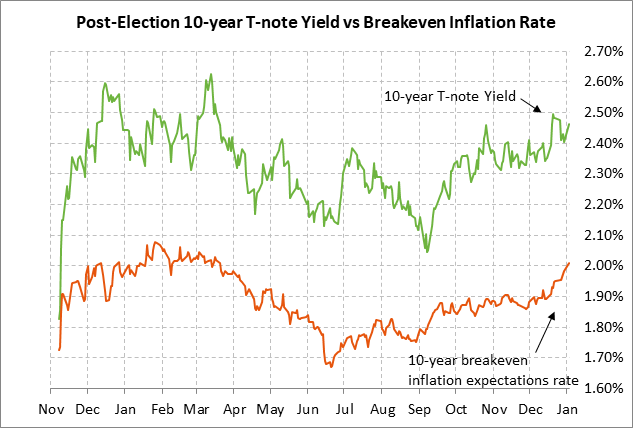

There is no justification at present for a negative real funds rate considering the strength of the U.S. economy and the tight labor market. In addition, the 10-year breakeven inflation expectations rate has risen sharply in the past two weeks by more than 10 bp to post a new 9-1/2 month high of 2.01% on Tuesday. Once the Fed pushes the funds rate above 2%, then the Fed can raise rates more slowly to avoid overtightening and a recession.

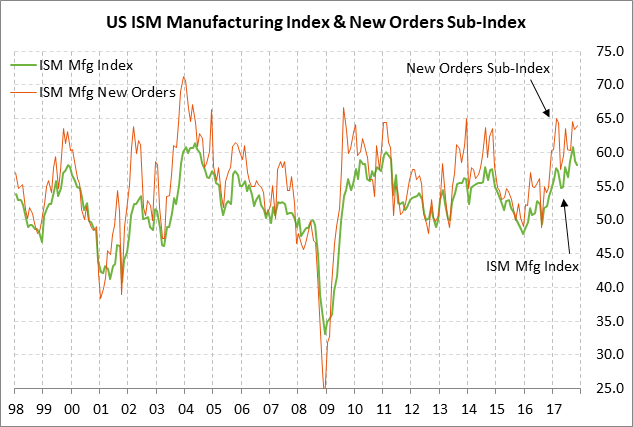

U.S. ISM manufacturing index expected to remain strong — The market consensus is for today’s Dec ISM manufacturing index to be unchanged at 58.2 following the Nov report of -0.5 to 58.2. The ISM manufacturing index fell by a total of -2.6 points in Oct-Nov but remains in strong shape at only -2.6 points below the 13-1/2 year high of 58.2 posted in September.

While manufacturing sentiment stalled in Q4, the ISM index should reach new highs in early 2018 due to optimism about (1) the strong U.S. and global economies, and (2) increased capital spending by companies taking advantage of the new tax law that allows full-expensing of equipment purchases. In addition, there is a full pipeline of orders since the ISM manufacturing new orders sub-index in November was very strong at 64.0, which was just mildly below the 8-1/4 year high of 65.1 posted in Feb 2017.

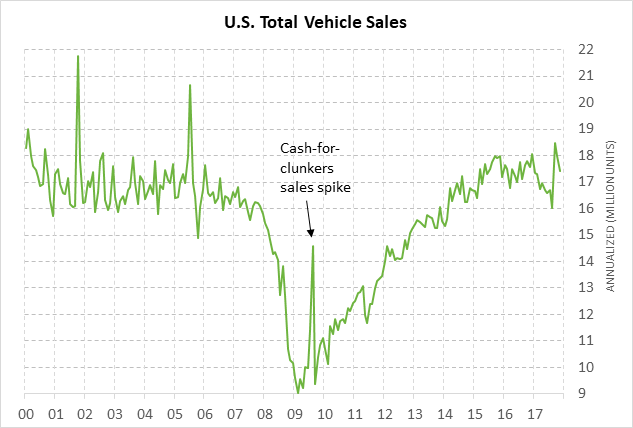

U.S. vehicle sales expected to close the year on a strong note — The market consensus is for today’s Dec total vehicle sales report to edge higher to 17.50 million from Nov’s 17.40 million. U.S. vehicle sales spiked higher to a 12-1/4 year high of 18.47 million in September, and have only backed off modestly from that high, due to replacement buying of vehicles damaged by Hurricane Harvey. However, vehicle sales are likely to trail off to more sustainable levels in 2018 as the toll slowly accumulates from higher interest rates.

German coalition talks begin — Party leaders will meet today to kick off exploratory talks scheduled for Jan 7-12 between Chancellor Merkel’s CSU bloc and the Social Democrats. Social Democrats are reluctantly entering talks on a possible coalition even though they suffered in the polls due to the last grand coalition with the CSU. If the talks fail, then Ms. Merkel will either have to call new elections or try to govern with a minority government, with specific legislation addressed by ad hoc coalitions.

The German political uncertainty is undercutting European confidence, as is the run-up to the Italian elections on March 4. The Italian elections could well produce a hung Parliament since none of the three main political groups have majority support. In addition, the anti-establishment and anti-euro Five Star Movement is leading the other political parties in the polls, thus increasing the chances that Five Star could somehow make it into power.

Congressional leaders meet today to avert a U.S. government shutdown in two weeks — The “Big Four” congressional leaders (Ryan, Pelosi, McConnell, Schumer) are scheduled to meet today with White House officials on the topic of preventing a government shutdown and resolving immigration issues. White House officials attending the meeting will include legislative affairs director Marc Short and budget director Mick Mulvaney. Congress has only 16 days to pass new spending authority and prevent a government shutdown when the current continuing resolution expires on Jan 19.

There is the distinct threat of a government shutdown this time around since Republicans and Democrats are at loggerheads on a range of issues including top-line funding for defense and non-defense spending, a dreamer solution, border wall funding, the bipartisan Obamacare fix that was promised to Senator Collins, an extension of foreign surveillance authority, disaster relief, and other issues.

Regarding the larger 2018 Republican legislative agenda, President Trump is scheduled to meet with House Speaker Ryan and Senate Majority Leader McConnell at Camp David this coming weekend (Jan 6-7). President Trump reportedly wants to move ahead with an infrastructure bill and Speaker Ryan’s plan for cutting welfare and entitlements. House-Senate Republicans will hold their annual policy retreat starting on Jan 31 at The Greenbrier for a larger discussion on the Republican agenda.

FOMC minutes will be gauged for hawkishness as inflation expectations move to new 9-1/2 month high — The FOMC today will release the minutes from its Dec 12-13 meeting. The FOMC at that meeting met unanimous market expectations by raising the funds rate target range by +25 bp to 1.25%-1.50%. The December rate hike made good on the FOMC’s forecast for three rate hikes in 2017. The FOMC is forecasting another three rate hikes in 2018, which is more hawkish than market expectations for only two rate hikes.

The market is forecasting a minimal 14% chance of a rate hike at the next FOMC meeting on Jan 30-31 but then a fairly strong 76% chance of a rate hike at the following meeting on March 20-21. The market is fully expecting the FOMC to implement that first rate hike of 2018 by the May 1-2 FOMC meeting.

The markets will carefully dissect today’s FOMC minutes to gauge the strength of the Fed’s intention to raise interest rate three times in 2018 to a new target range of 2.00%-2.25%. We expect the Fed to make good on its 2018 rate-hike intentions in order to at least get the funds rate above inflation expectations and do away with a negative real federal funds rate.

There is no justification at present for a negative real funds rate considering the strength of the U.S. economy and the tight labor market. In addition, the 10-year breakeven inflation expectations rate has risen sharply in the past two weeks by more than 10 bp to post a new 9-1/2 month high of 2.01% on Tuesday. Once the Fed pushes the funds rate above 2%, then the Fed can raise rates more slowly to avoid overtightening and a recession.

U.S. ISM manufacturing index expected to remain strong — The market consensus is for today’s Dec ISM manufacturing index to be unchanged at 58.2 following the Nov report of -0.5 to 58.2. The ISM manufacturing index fell by a total of -2.6 points in Oct-Nov but remains in strong shape at only -2.6 points below the 13-1/2 year high of 58.2 posted in September.

While manufacturing sentiment stalled in Q4, the ISM index should reach new highs in early 2018 due to optimism about (1) the strong U.S. and global economies, and (2) increased capital spending by companies taking advantage of the new tax law that allows full-expensing of equipment purchases. In addition, there is a full pipeline of orders since the ISM manufacturing new orders sub-index in November was very strong at 64.0, which was just mildly below the 8-1/4 year high of 65.1 posted in Feb 2017.

U.S. vehicle sales expected to close the year on a strong note — The market consensus is for today’s Dec total vehicle sales report to edge higher to 17.50 million from Nov’s 17.40 million. U.S. vehicle sales spiked higher to a 12-1/4 year high of 18.47 million in September, and have only backed off modestly from that high, due to replacement buying of vehicles damaged by Hurricane Harvey. However, vehicle sales are likely to trail off to more sustainable levels in 2018 as the toll slowly accumulates from higher interest rates.

German coalition talks begin — Party leaders will meet today to kick off exploratory talks scheduled for Jan 7-12 between Chancellor Merkel’s CSU bloc and the Social Democrats. Social Democrats are reluctantly entering talks on a possible coalition even though they suffered in the polls due to the last grand coalition with the CSU. If the talks fail, then Ms. Merkel will either have to call new elections or try to govern with a minority government, with specific legislation addressed by ad hoc coalitions.

The German political uncertainty is undercutting European confidence, as is the run-up to the Italian elections on March 4. The Italian elections could well produce a hung Parliament since none of the three main political groups have majority support. In addition, the anti-establishment and anti-euro Five Star Movement is leading the other political parties in the polls, thus increasing the chances that Five Star could somehow make it into power.