- US/Japanese trade tensions in focus with 2-day auto tariff meeting beginning today

- U.S. tariff on $16 billion of Chinese goods goes into effect Aug 23

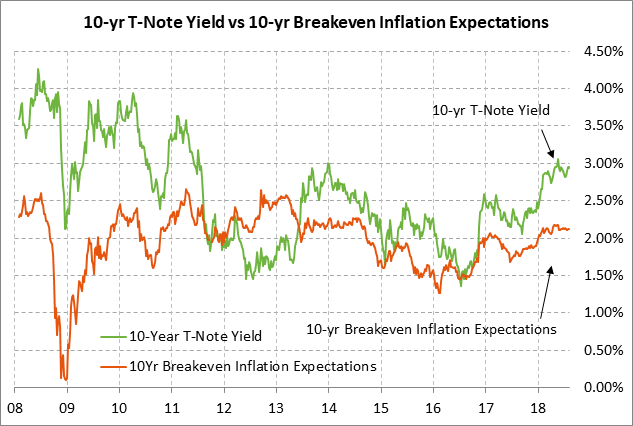

- 10-year T-note yield sees upward pressure from inflation and the strong economy

- 10-year T-note auction expected to yield near 2.97%

US/Japanese trade tensions in focus with 2-day auto tariff meeting beginning today — U.S. Trade Representative Lighthizer and Japanese economic minister Motegi will meet today and Thursday to discuss the Trump administration’s intent to slap a 25% tariff on imported vehicles. Japan has so far taken a low-key approach with President Trump and did not retaliate for U.S. steel and aluminum tariffs. However, a 25% tariff on Japanese imported autos would have a much larger effect and might well draw retaliation if negotiations are unsuccessful.

U.S. tariff on $16 billion of Chinese goods goes into effect Aug 23 — The Trump administration late yesterday afternoon announced that its 25% tariff on $16 billion of Chinese goods will go into effect on August 23. China has already announced an equal tariff on $16 billion of U.S. goods in retaliation. Yesterday’s announcement means that the U.S. and China by Aug 23 will have penalty tariffs on a total of $50 billion worth of each other’s goods. As punishment for China’s retaliation, the Trump administration has announced a 25% tariff on another $200 billion worth of Chinese goods, which could take effect shortly after the public comment period ends on Sep 5. China has already announced retaliation on that move with tariffs of 5-25% on $60 billion worth of U.S. goods.

Yesterday’s tariff announcement suggests that China remains unwilling to make the major trade concessions demanded by President Trump. The odds now appear to be high that the next round of tariffs will go into effect in early September.

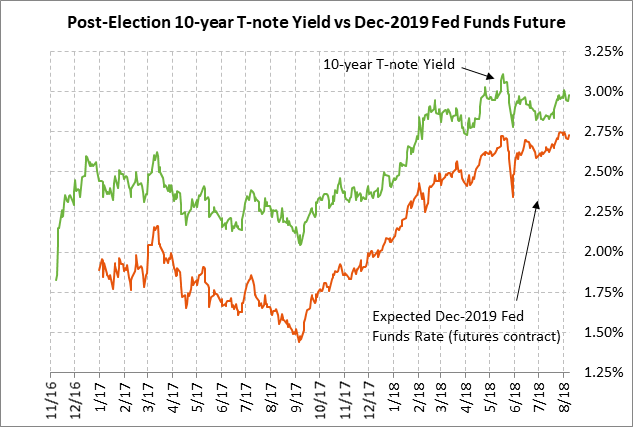

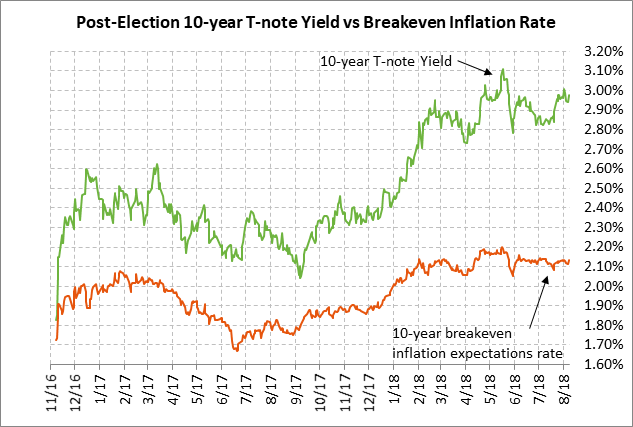

10-year T-note yield sees upward pressure from inflation and the strong economy — The 10-year T-note yield posted a 7-year high of 3.13% in May but has since consolidated below that level due to trade tensions. The 10-year T-note yield on Tuesday closed +4 bp at 2.97%.

Bearish factors for T-note prices include (1) the Fed’s steady rate-hike regime and the Fed’s balance sheet reduction program, (2) the rise in inflation, (3) the strong U.S. economy, and (4) the prospects for tighter monetary policies in Europe and Japan in 2019. Bullish factors include (1) global trade tensions, (2) political uncertainty in Washington with the Russia investigation, and (3) European uncertainty caused by Brexit and the challenges to EU governance by the populist Italian government.

The 10-year T-note yield since late 2017 has risen sharply by about 100 bp mainly because of the Jan 1 tax cuts, which prompted a more aggressive Fed rate-hike regime, a stronger economy, and fears about rising inflation. U.S. real GDP growth in Q2 was very strong at +4.1% and continued strong growth near 3% is likely for the second half of the year. The consensus is for strong U.S. GDP growth near 3% for all of 2018, which would be well above the Fed’s estimated U.S. GDP potential of +1.8%.

The 10-year T-note yield is also seeing upward pressure from increased inflation concerns. The core PCE deflator has risen from +1.5% y/y last summer to the current level of +1.9% y/y, thus essentially matching the Fed’s +2.0% inflation target. The headline PCE deflator in June hit a 6-year high of +2.2% y/y due to higher energy prices. Inflation expectations are also running above-target with the 10-year breakeven inflation expectations rate at +2.12%.

Inflation is seeing upward pressure from the usual suspects of a strong economy and higher energy prices. However, inflation is also seeing upward pressure from tariffs. If the tariffs expand to include autos and another $200 billion of Chinese products, then U.S. inflation will see a further decisive boost, perhaps forcing the Fed into an extra rate hike.

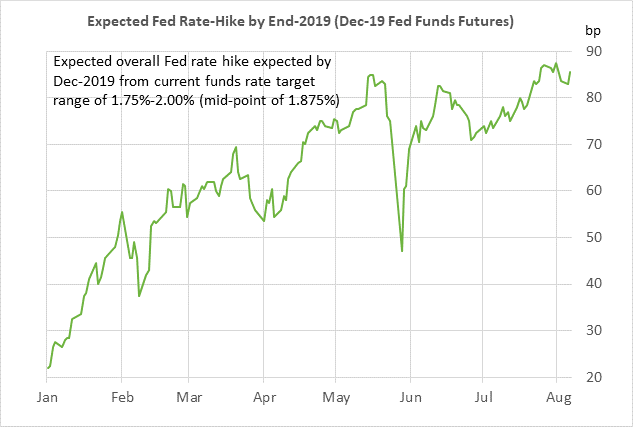

The Fed in any case is proceeding with its monetary normalization program. The market is fully expecting another rate hike at the next FOMC meeting on Sep 25-26. The market is then discounting an 82% chance of the fourth rate hike of the year at the Dec 18-19 meeting, which would put the funds rate at 2.25-2.50% by year-end. The market is then expecting the Fed to finish off its rate hike regime next year with up to two rate hikes, leaving the funds rate near 2.75% by the end of 2019.

The prospect for another 100 bp of Fed rate hikes over the next year will keep upward pressure on the 10-year T-note yield. However, the 10-year yield is not likely to move up by as much as the funds rate, which would suggest that an inverted yield curve will occur by later this year or early next year, which would be a negative indicator for the U.S. economy.

10-year T-note auction expected to yield near 2.97% — The Treasury today will sell $26 billion of new 10-year T-notes. Today’s 10-year T-note issue was trading at 2.97% in when-issued trading late yesterday afternoon. The 12-auction averages for the 10-year are: 2.47 bid cover ratio, $19 million in non-competitive bids to mostly retail investors, 4.8 bp tail to the median yield, 19.6 bp tail to the low yield, and 50% taken at the high yield. The 10-year is slightly below average in popularity among foreign investors and central banks. Indirect bidders took an average of 62.5% of the last twelve 10-year T-notes, which is mildly below the median of 63.3% for all recent Treasury coupon auctions.

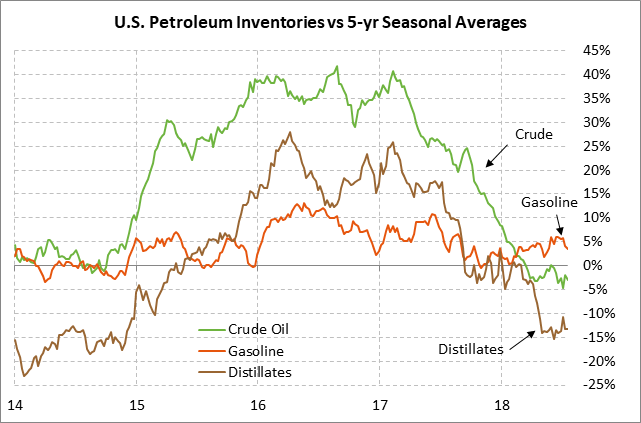

Weekly EIA report — The market consensus for today’s weekly EIA report is for a -3.0 mln bbl drop in U.S. crude oil inventories, a -1.3 mln bbl drop in gasoline inventories, and a +1.0 mln bbl increase in distillate inventories. U.S. oil inventories are -3.0% below the 5-year seasonal average while gasoline inventories are +3.4% above average and distillate inventories are -13.2% below average. U.S. oil production reached a record high of 11.000 million bpd in the past two reporting weeks.