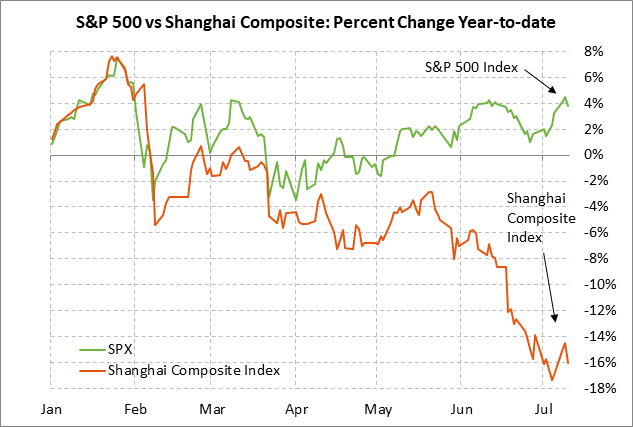

- Chinese stocks and yuan show sharp declines on stepped-up trade war

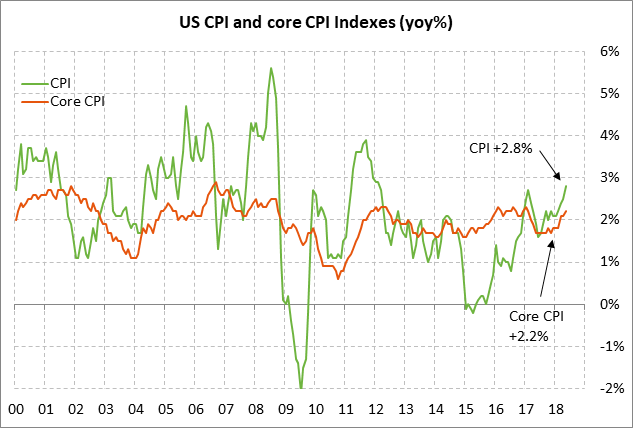

- U.S. core CPI expected to match 10-year high

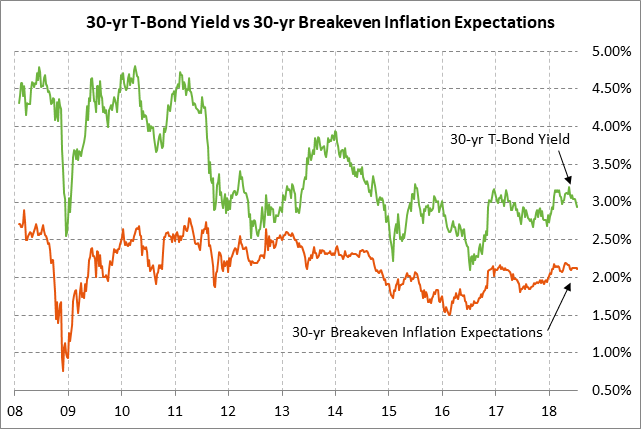

- 30-year T-note auction to yield near 2.86%

Chinese stocks and yuan show sharp declines on stepped-up trade war — The Shanghai Composite index on Tuesday fell sharply by -1.76% back towards last Friday’s 2-1/4 year low. Meanwhile, the Chinese yuan on Tuesday fell by -0.73%, nearing last week’s 1-year low. The S&P 500 index on Tuesday fell by -0.71% and the Eurostoxx 50 index fell by -1.47%. A wide variety of commodities on Tuesday also took a hit due to expectations for trade flow disruptions and slower global economic growth due to the U.S. trade war.

The markets fell on Tuesday after the Trump administration late Monday announced the list of $200 billion of Chinese products that will be subject to a 10% tariff, likely in September when the public comment period and public hearings are concluded. China on Tuesday vowed to retaliate but did not specify exactly what retaliation methods it might employ.

The markets are pessimistic about a U.S./Chinese trade compromise to avert the new tariffs since there are currently no serious negotiations between U.S. and Chinese officials. Instead, both sides seem to be battening down the hatches for a dragged-out dispute. China has fewer products to retaliate against than the U.S., but China has plenty of other ways to inflict damage on the U.S. such as curbing the sales of U.S. companies within China or by forcing a depreciation of the yuan.

In addition, China has the nuclear option of unloading some or all of the $1.2 trillion of Treasury securities that it holds as part of its foreign exchange reserves. Selling a significant chunk of those Treasury securities would not be in China’s immediate interests since the resulting plunge in T-note prices would hurt the value of the rest of its portfolio. Nevertheless, China’s sale of Treasury securities is a possibility if the trade war reaches the point of scorched-earth tactics where neither side cares if they hurt themselves as long as they are inflicting pain on their opponent.

Market gloom is building due to the expanding U.S. trade war. The U.S. has already gone ahead with steel and aluminum tariffs on most countries, which has drawn tariff retaliation on more than $25 billion of U.S. exports. The U.S. and China on July 6 implemented a 25% reciprocal tariff on $34 billion worth of each other’s goods. The U.S. and China by August are likely to implement a 25% tariff on another $16 billion worth of each other’s goods. Finally, President Trump’s threat is still outstanding for a 25% tariff on all U.S. auto imports, or a more targeted 20% tariff on U.S. auto imports from Europe.

U.S. core CPI expected to match 10-year high — Today’s CPI report is expected to move higher and display a worsening inflation picture. The consensus is for today’s June CPI to edge higher to +2.9% y/y, which would exceed May’s 6-year high of +2.8%. Meanwhile, the consensus is for today’s June core CPI to rise to +2.3% y/y from May’s +2.2%, thus matching the 10-year high posted in Jan 2017.

Both the expected CPI of +2.9% y/y and core CPI of +2.3% would be above the Fed’s +2.0% inflation target. Yesterday’s June PPI report of +3.4% y/y headline and +2.8% core were substantially stronger than expected and suggested an upside risk for today’s CPI report.

The only good inflation news is that the PCE deflator, which is the Fed’s preferred inflation measure, is weaker than the CPI and PPI indexes. However, the PCE deflator is also on the rise, having reached a 6-year high of +2.3% in May. Meanwhile, the core PCE deflator in May reached a 6-year high of +2.0%, matching the Fed’s inflation target.

There is upward pressure on inflation due to (1) strong economic growth with Q2 GDP expected above +3.4%, (2) the recent 3-1/2 year high in oil prices, (3) generally strong material input prices, and (4) upward price pressure from U.S. tariffs on a range of imported products.

The Fed has said that it will tolerate a mild overshoot of its 2.0% inflation target since its target is symmetrical. However, it is possible that the U.S. inflation rate will rise farther above the Fed’s target due to the various upward pressures, thus putting the Fed behind the inflation curve. That increases the chance of the fourth Fed rate hike of the year in December and could force the Fed into more rate hikes in 2019 than the market is currently expecting.

30-year T-note auction to yield near 2.86% — The Treasury today will sell $14 billion of 30-year T-bonds in the second and final reopening of the 3-1/8% 30-year bond of May 2048. Today’s auction will conclude this week’s $69 billion coupon package.

Today’s 30-year T-bond issue was trading at 2.95% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of 0.83% against the current 30-year breakeven inflation expectations rate of 2.12%. The 30-year T-bond yield has fallen by -31 bp to 2.95% from May’s 3-3/4 year high of 3.26% mainly because of trade tensions and reduced expectations for Fed rate hikes.

The 12-auction averages for the 30-year are as follows: 2.38 bid cover ratio, $5 million of non-competitive bids taken mostly by retail investors, 4.8 bp tail to the median yield, 42.2 bp tail to the low yield, and 32% taken at the high yield. The 30-year is a little below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.7% of the last twelve 30-year T-bond auctions, which is mildly below the median of 63.3% for all recent coupon auctions.