- FOMC minutes could shed some light on the odds for a fourth rate hike this year

- U.S. ADP employment expected to be solid

- U.S. unemployment claims expected to remain favorable

- U.S. ISM non-manufacturing index expected to show continued strength in service-sector confidence

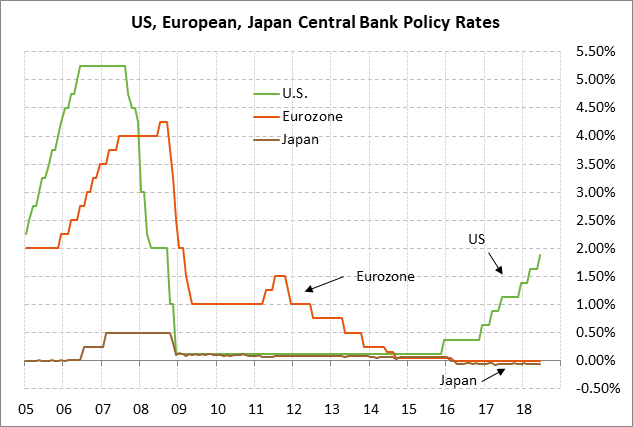

FOMC minutes could shed some light on the odds for a fourth rate hike this year — Today’s release of the minutes from the June 12-13 FOMC meeting may provide additional information for reassessing whether the Fed will end up raising interest rates four times this year. The FOMC at its June 12-13 meeting implemented its second +25 bp rate hike of the year by raising its funds rate target to the current range of 1.75-2.00%.

The market is fully discounting the third rate hike of the year at the FOMC meeting after next on Sep 25-26. The market is then discounting about a 50% chance that the FOMC will implement its fourth rate hike of the year at its Dec 18-19 meeting.

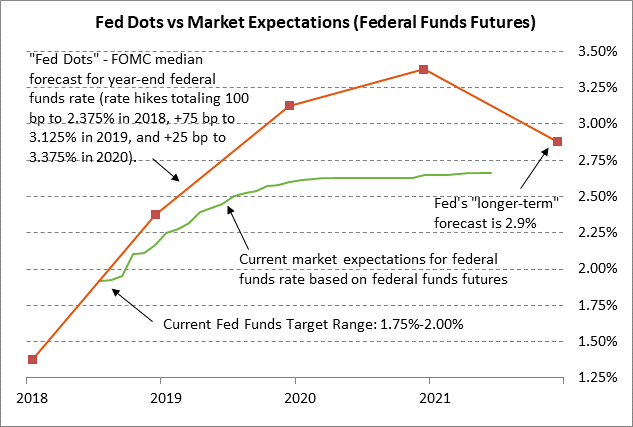

We believe the odds are strong for the FOMC to proceed with its fourth rate hike in December to a target range of 2.25-2.50%, assuming that the U.S. economy is not derailed by trade tensions. With a new funds rate target mid-point of 2.38%, the FOMC would have finally raised the funds rate above its 2.0% inflation target and the current breakeven inflation expectations rate of 2.15%, thus leaving the funds in real territory for the first time in more than a decade. The FOMC could then take its time in deciding how quickly to raise its funds rate the rest of the way to its long-term neutral rate of 2.9%.

The market continues to believe that the Fed will raise the funds rate by only another 100 bp from the current level in order to match its 2.9% neutral rate. The Fed dots, by contrast, remain significantly more hawkish and are looking for an overall 150 bp rate hike from the current level to over 3.25% to address what the Fed expects to be an overshoot on both its inflation and labor market targets.

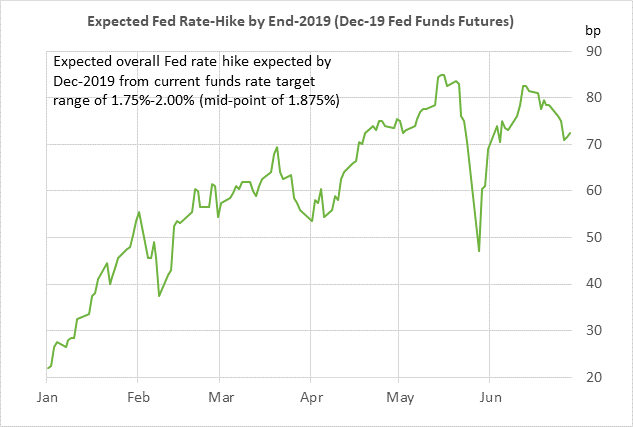

The market is currently expecting another 72.5 bp of rate hike by the end of 2019, according to the Dec 2019 federal funds rate. That is down by 12.5 bp from the peak expectation of 85 bp seen in May and down by 10 bp from the 82.5 bp seen just a few weeks ago. Market expectations for Fed rate hikes have faded a bit in the past several weeks due to the pile-up of trade tensions and due to the turmoil in China where the stock market and the yuan have fallen sharply.

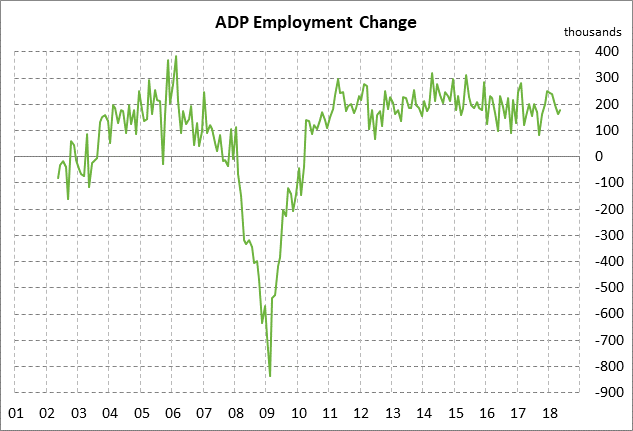

U.S. ADP employment expected to be solid — The market consensus is for today’s June ADP employment report to show an increase of +190,000, which would be mildly better than May’s report of +178,000. Today’s expected report of +190,00 would be close to the 12-month trend average of 186,000.

On the labor front, the markets are mainly looking ahead to Friday’s June unemployment report, which is expected to show continued strength in the U.S. labor market. The market consensus is for Friday’s June payroll report to show a solid increase of +195,000. That would be down from May’s increase of +223,000 but would be very close to the 12-month trend average of +197,000.

The consensus is for Friday’s June unemployment rate to remain unchanged from May 48-year low of 3.8%. The unemployment rate is now at the lowest level since 1969. The Fed is forecasting that the unemployment rate will fall even farther, i.e., to 3.6% by late this year and then to 3.5% in 2019-2020.

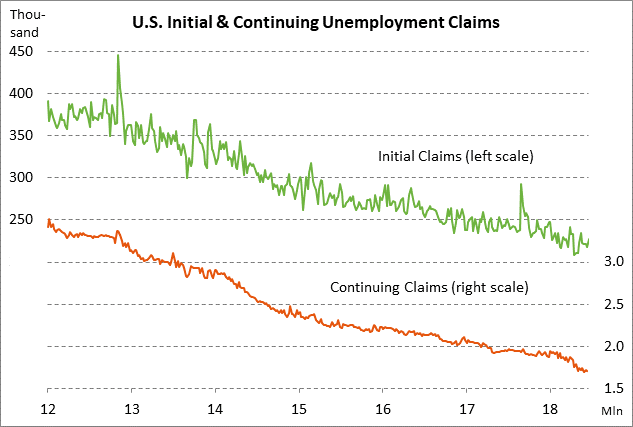

U.S. unemployment claims expected to remain favorable — Today’s unemployment claims report is expected to indicate continued labor market strength with layoffs near 4-decade lows. The initial claims series is currently only 18,000 above April’s 48-year low of 209,000 and the continuing claims series is only 4,000 above June’s 44-year low of 1.701 million.

The market consensus is for today’s initial unemployment claims report to show a -2,000 decline to 225,000, reversing part of last week’s +9,000 rise to 227,000. The consensus is for today’s continuing claims report to show an increase of +13,000 to 1.718 million, reversing part of last week’s -21,000 decline to 1.705 million.

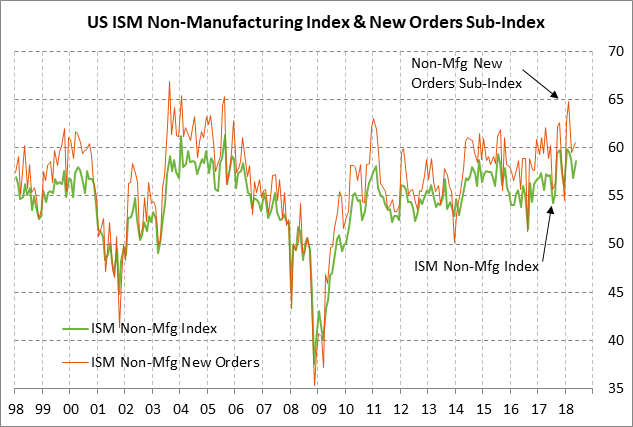

U.S. ISM non-manufacturing index expected to show continued strength in service-sector confidence — The market consensus is for today’s June ISM non-manufacturing PMI to show a -0.3 point decline to 58.3, giving back a little of May’s solid +1.8 point increase to 58.6. The index is in strong shape at only 1.3 points below January’s 13-year high of 59.9.

U.S. business confidence remains high due to (1) the strong economy where Q2 GDP could hit 4%, (2) the strong recovery of consumer spending in Q2, and (3) flush business and consumer cash positions after the sharp Jan 1 tax cuts. The trade war is less of a concern for U.S. service-sector businesses due to their lower exposure to tariffs. However, some service-sector businesses are nevertheless being hit by trade worries and by higher fuel prices.