- EU Summit begins with a potential Brexit deal still in flux

- U.S. manufacturing production expected to decline and highlight manufacturing recession

- U.S. housing starts expected to remain strong

- 5-year TIPS auction

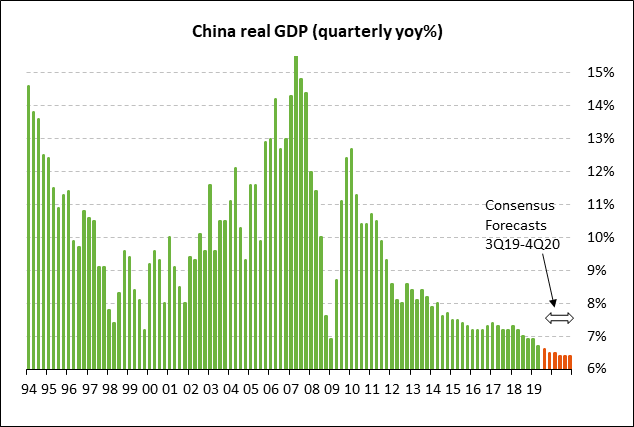

- China Q2 GDP expected to slide to new 26-year low

EU Summit begins with a potential Brexit deal still in flux — UK and EU negotiators were in talks late Wednesday attempting to forge an agreement before the 2-day EU Summit that begins today.

If there is an agreement in time for approval by EU leaders at their Thursday/Friday summit, then the UK Parliament can meet on Saturday for an up or down vote on an agreement. In the event that an agreement doesn’t come in time for approval by EU leaders at the Thursday/Friday summit, then the UK Parliament could still vote on the deal on Saturday. If approved, then the EU could hold an emergency summit within the next two weeks to approve the deal before the Oct 31 Brexit deadline.

If there is no agreement by Saturday, or if the UK Parliament votes down an agreement on Saturday, then UK Prime Minister Johnson is required by the Benn Act to request an extension of the Oct 31 Brexit deadline. The question in that case would be whether Mr. Johnson complies with the spirit of the law and gets a deadline extension from the EU, or whether he would find a loophole or simply refuse to request an extension, in which case there is a risk of a no-deal Brexit on Oct 31.

The best outcome for the markets, of course, would be if the EU and the UK Parliament approve a Brexit withdrawal deal and the UK exits the EU on the October 31 deadline. The UK would then enjoy a smooth transition period during which border conditions would be unchanged with the UK operating as if it were still in the EU. The two sides would then have plenty of time to work out a long-term UK/EU trade deal.

If there is no near-term Brexit agreement, then the next best outcome would be an extension of the October 31 Brexit deadline to avert the possibility of a no-deal Brexit on October 31. The betting odds are still very low for that possibility at only 15% for a no-deal Brexit this year.

The worst outcome would be if Prime Minister Johnson forces a no-deal Brexit on October 31 by refusing to accept a deadline extension. That action would cause an uproar in the UK and a series of court challenges. Nevertheless, Mr. Johnson could probably find a way to force an exit if he is willing to take the legal and political heat.

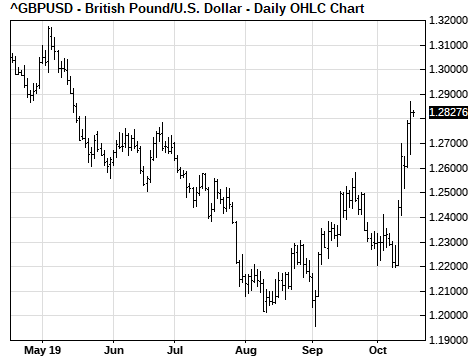

The markets remain optimistic about the Brexit situation. GBP/USD on Wednesday extended the 5-session rally to a total of +5.1% and posted a new 5-month high. GBP/USD on Wednesday closed up +0.35% even though EU officials on Wednesday turned less optimistic about a deal than they were on Tuesday.

The main question is whether the Northern Irish Democratic Unionist Party (DUP) party will approve a Johnson deal. Without the DUP’s approval, a Brexit deal has virtually no chance of getting through the UK Parliament.

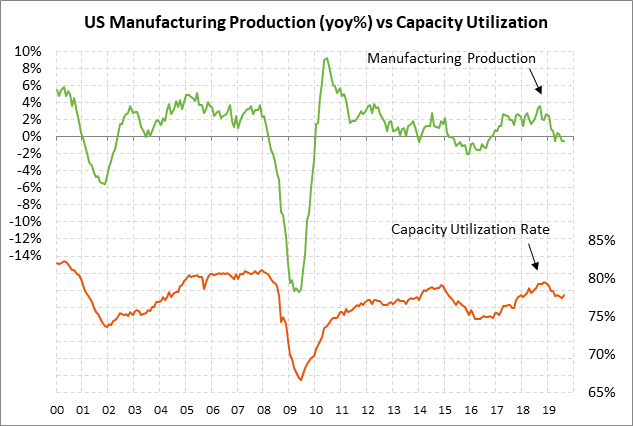

U.S. manufacturing production expected to decline and highlight manufacturing recession — The consensus is for today’s Sep U.S. manufacturing production report to show a decline of -0.3%, giving back part of Aug’s gain of +0.5%. The overall Sep industrial production report is expected to show a decline of -0.2% after Aug’s +0.6% rise.

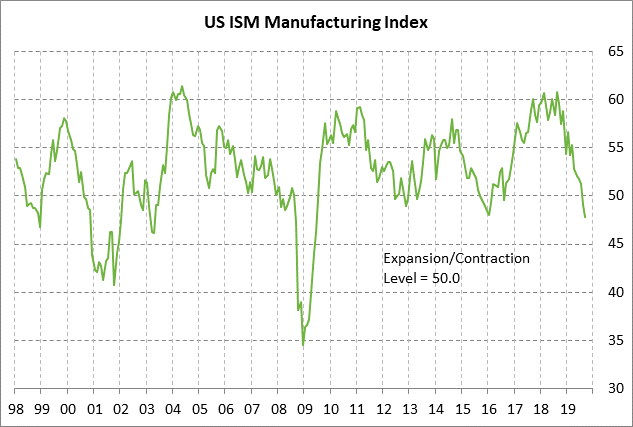

The U.S. manufacturing sector is currently in a recession as seen by the fact that manufacturing production has been in negative territory on a year-on-year basis in the last two reporting months. In August, manufacturing production fell by -0.4% y/y. Also, the ISM manufacturing sector is in contractionary territory with the index in September falling -1.3 points to a 10-year low of 47.8. The Sep ISM manufacturing new orders index was in even weaker shape at 47.3, illustrating a paltry pipeline of orders.

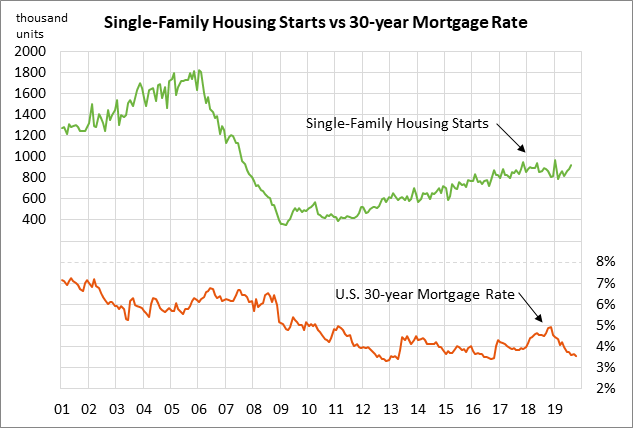

U.S. housing starts expected to remain strong — The market consensus is for today’s Sep housing starts report to fall by -3.2% to 1.320 million, giving back a little of Aug’s +12.3% surge to a 12-year high of 1.364 million.

U.S. homebuilders are in a good mood as seen by the fact that the NAHB housing market index in September rose by +1 point to match the 1-1/3 year high of 68. Homebuilders are finding encouragement from continued strength in home sales and from low mortgage rates. The current 30-year mortgage rate of 3.57% is only 8 bp above September’s 3-year low of 3.49%.

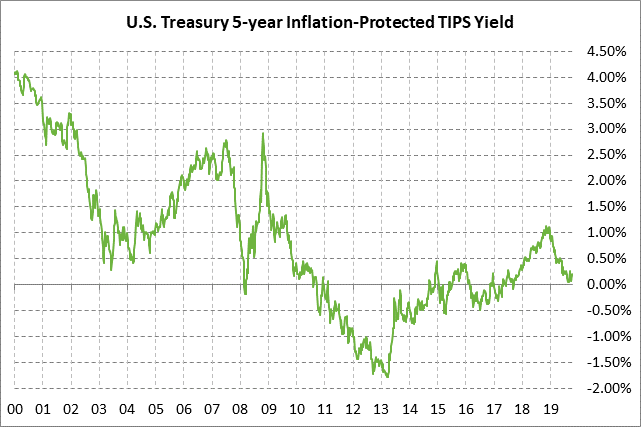

5-year TIPS auction — The Treasury today will sell $17 billion of 5-year TIPS. The benchmark 5-year TIPS yield yesterday closed at 0.21% and has been moving sideways in the past 1-1/2 months mildly above August’s 2-year low of -0.02%. The 12-auction averages are: 2.56 bid cover, $45 mln in non-competitive bids, 5.4 bp tail to the median yield, 15.1 bp tail to the low yield, 31% taken at the high yield, and 69.8% taken by indirect bidders (far above the recent average for all coupons of 59.6%).

China Q2 GDP expected to slide to new 26-year low — The consensus is for tonight’s China Q3 GDP to fall by -0.1 point to a new 26-year low of +6.1% y/y from Q2’s +6.2% y/y. A decline of only 0.1 point would actually be good news for the Chinese economy, which is taking a fairly heavy hit from President Trump’s economic war. The markets generally believe that China’s GDP figure is overstated by as much as 2-3 points, meaning the economic weakness on the ground is probably worse than what is reflected in the official data. The consensus going forward is for China’s GDP to continue to slowly slide to +6.0% in Q4 and then to 5.9% next year. Tonight’s China Sep industrial production report is expected to improve mildly to +4.9% y/y from Aug’s +4.4%. Tonight’s Sep retail sales report is expected to improve to +7.8% y/y from Aug’s +7.5%.