- FOMC predicts no further rate cuts

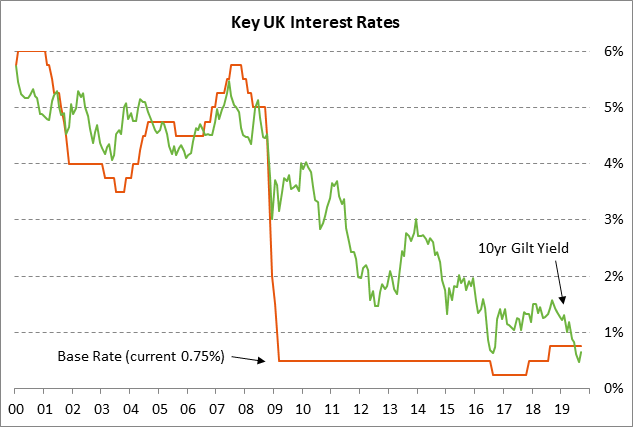

- BOE expected to leave rates unchanged

- U.S. existing home sales expected to show a small decline but remain generally strong

- U.S. LEI expected to revert to a declineÂ

- U.S. current account deficit

- 10-year TIPS auction

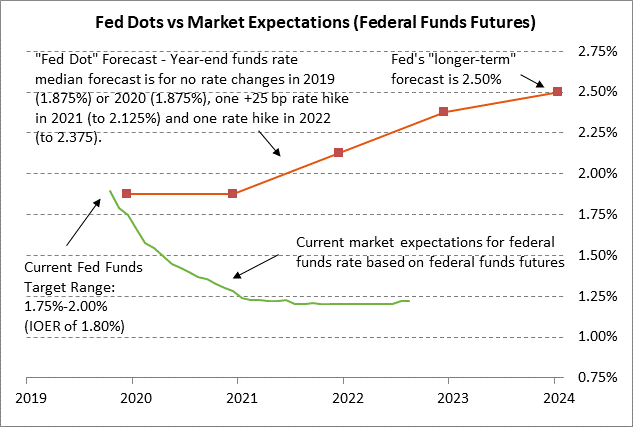

FOMC predicts no further rate cuts — The FOMC on Wednesday met unanimous market expectations by cutting the funds rate target by -25 bp to 1.75%/2.00%. However, the overall outcome of the FOMC meeting was a little more hawkish than expected as seen by the fact that the federal funds futures curve showed a slight 1-2 bp tightening in response to the meeting. Fed Chair Powell said that “the economy has continued to do well and the outlook is favorable” and that Fed rate cuts are to provide “insurance” against downside risks.

FOMC members are clearly reluctant to keep cutting rates since the median forecast from the new set of Fed dots is for no rate changes for the rest of 2019 and 2020 and then a rate hike in 2021 and a second rate hike in 2022. The Fed left its view of the “longer-term” funds rate unchanged at 2.50%.

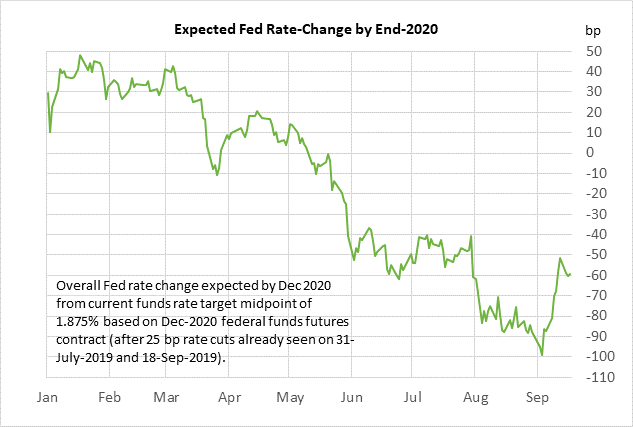

Yet the markets remain much more dovish than the Fed. The market is expecting another 60.5 bp of easing by the end of 2020 (2.4 rate cuts). The market is discounting the odds of a -25 bp rate cut at 34% for the next FOMC meeting on Oct 29-30 and at 88% for the following meeting on Dec 10-11.

The reality is that the outlook for Fed policy is highly uncertain. The Fed is hoping that it doesn’t have to keep cutting rates since the economy is still in decent shape and inflation is rising. However, there are still substantial downside risks from (1) trade tensions, (2) slowing growth in China and Europe, (3) Brexit, and (4) a potential military confrontation with Iran that could cause an even larger upward spike in oil prices.

Fed Chair Powell at his press conference said that this week’s surge in the repo rate has “no implications for the economy or the stance of monetary policy.” However, the Fed took one step to alleviate the situation by cutting the IOER rate (interest on excess reserves) by 30 bp to 1.80%, which was larger than the 25 bp cut in the funds rate. The larger IOER cut was designed to encourage banks to lend their cash to other financial institutions rather than lock it up at the Fed.

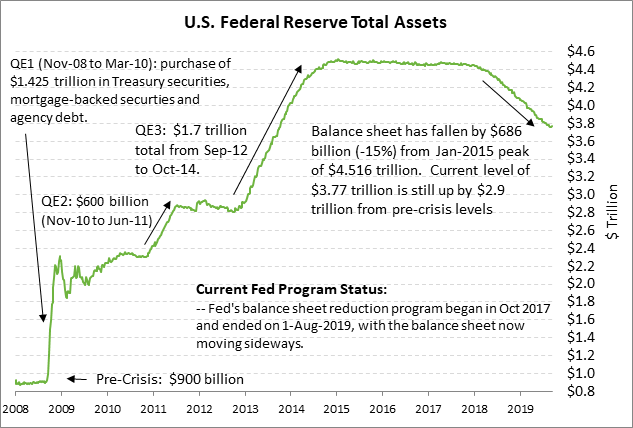

Mr. Powell also suggested that the Fed will proceed with its long-discussed plan of setting up a permanent repo facility to provide funding to banks. He also suggested that the Fed will soon start allowing its balance sheet to rise on an “organic basis” (i.e., not QE) in order to meet the market’s demand for reserves. This week’s squeeze in the money markets suggests that the Fed may have reduced its balance sheet too far, thus making liquidity scarce during times of increased need such as this week when the Treasury auctions settled and when corporations withdrew cash from the banking system to pay taxes.

BOE expected to leave rates unchanged — The Bank of England at its meeting today is expected to leave its base rate unchanged at 0.75%. The BOE is on hold as it waits to see what happens with Brexit on the October 31 deadline. If Prime Minister Johnson pushes through a no-deal Brexit, the ensuing chaos will clearly require at least one rate cut.

On the other hand, if Mr. Johnson miraculously gets Parliament to approve an EU-revised withdrawal agreement, then no rate cut is likely to be necessary since the UK would enter a smooth transition period during which the economy should improve. If there is another extension of the Brexit deadline, then the BOE will remain in purgatory, waiting to see if business and consumer confidence sags by enough that it is forced to join the Fed and ECB in cutting rates. The UK economy is already in weak shape with Q2 GDP falling by -0.2% q/q, although a recovery by +0.3% is expected in Q3.

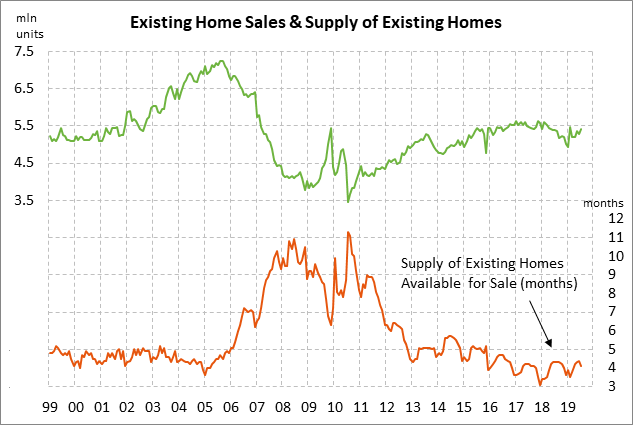

U.S. existing home sales expected to show a small decline but remain generally strong — The market consensus is for today’s Aug existing home sales report to show a -0.7% decline to 5.38 million, giving back part of July’s +2.5% increase to 5.42 million. Home sales remain in strong shape at only 4% below the 12-year high of 5.64 million units posted in Nov 2017. Home sales continue to receive a boost from low mortgage rates. The current 30-year mortgage rate of 3.56% is only 7 bp above mid-Sep 3-year low of 3.49%.

U.S. LEI expected to revert to a decline — The consensus is for today’s Aug leading indicators report to show a small decline of -0.1%. The LEI in July showed a strong increase of +0.5%, but that followed two months in which the LEI declined by -0.1%. Indeed, the LEI in July fell to a 2-1/2 year low of +1.6% on a year-on-year basis, which suggests a weak near-term economy.

U.S. current account deficit — Today’s Q2 current account deficit is expected to narrow slightly to -$127.8 billion from Q1’s -$130.4 billion, but remain wider than the 8-quarter trend average of -$120.4 billion.

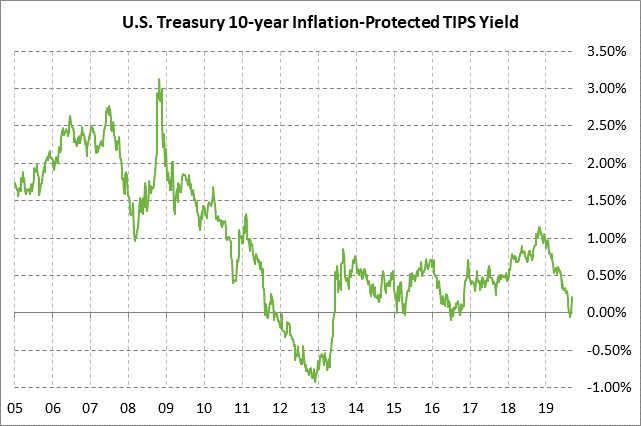

10-year TIPS auction — The Treasury today will sell $12 billion of 10-year TIPS. The benchmark 10-year TIPS on Wednesday closed the day at 0.19%, which is an improvement for auction buyers compared with the 6-1/4 year low of -0.12% seen in late-Aug.

The 12-auction averages for the 10-year TIPS are as follows: 2.50 bid cover ratio, $21 million in non-competitive bids, 5.5 bp tail to the median yield, 14.0 bp tail to the low yield, and 52% taken at the high yield. The 10-year TIPS is the third most popular security among foreign investors and central banks behind the 30-year TIPS and the 5-year TIPS. Indirect bidders, a proxy for foreign buyers, have taken an average of 67.6% of the last twelve 10-year TIPS auctions, which is well above the median of 60.2% for all recent Treasury coupon auctions.