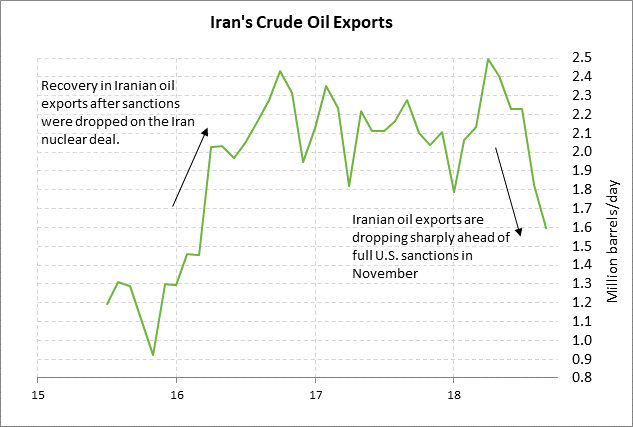

- Oil prices hit new 4-year high as concerns mount about falling Iranian exports

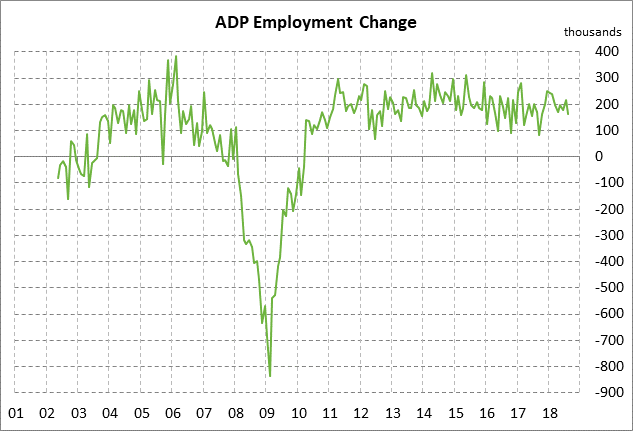

- U.S. ADP employment expected to remain solid

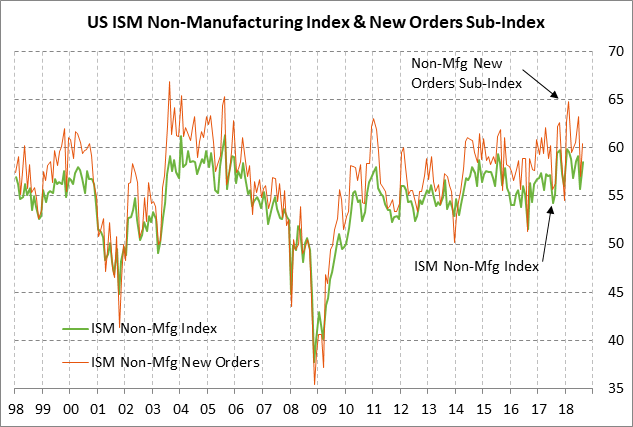

- U.S. ISM non-manufacturing index expected to indicate continued strong business confidence

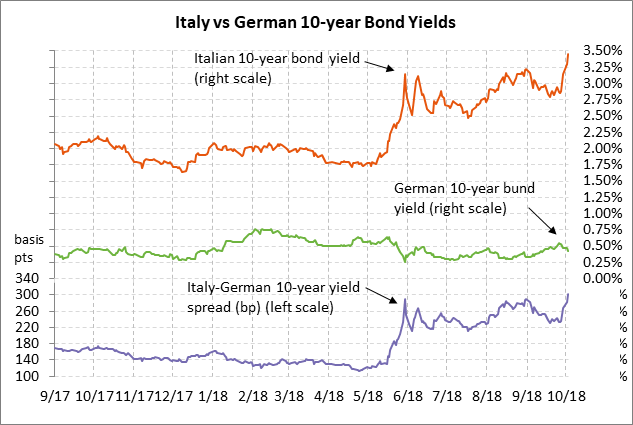

- Italian 10-year yield reaches another new 4-1/2 year high as Italian officials continue to disregard market forces

- EIA weekly Petroleum Status Report

Oil prices hit new 4-year high as concerns mount about falling Iranian exports — Nov WTI crude oil futures prices on Tuesday rose to a new 4-year high on the nearest-futures chart of $75.91 per barrel, while Nov Brent crude oil futures consolidated below Monday’s 4-year high of $85.45. The premium of Brent over West Texas Intermediate is very high at nearly $10 per barrel because international-benchmark Brent oil prices are being boosted by the decline in Iranian oil exports and tighter global oil supplies, while the record level of U.S. oil production is keeping a lid on domestic U.S. WTI oil prices.

Iranian oil exports have already plunged by -900,00 bpd (-36%) to 1.6 million bpd from April’s peak of 2.5 million bpd as foreign oil buyers shun Iranian oil ahead of full U.S. sanctions that take effect in November. After full sanctions take effect, Iranian oil exports will continue to fall sharply. The Trump administration says it will allow virtually no exceptions to the sanctions, although some buyers such as China have work-arounds and will be able to keep buying Iranian oil. Oil prices have rallied on concern that global oil supplies will continue to tighten through year-end since Saudi Arabia is the only country with any significant excess capacity to use to boost production and offset the decline in Iranian exports.

U.S. ADP employment expected to remain solid — The market consensus is for today’s Sep ADP employment report to show an increase of +184,000. The expected report would represent an improvement from Aug’s soft report of +163,000 but would remain mildly below the 12-month trend-average of +190,000. Today’s ADP report is likely to be depressed to some extent by Hurricane Florence, which caused major business disruptions in mid-September in the North Carolina region.

On the labor front, the market is mainly looking ahead to Friday’s Sep unemployment report where payrolls are expected to show a respectable increase of +184,000, though down from Aug’s +201,000. Job growth continues to hold up very well despite the difficulty that some businesses are having in finding qualified workers in the tight job market. Job growth also remains strong even though U.S. businesses have hired a net 19.5 million new employees since the Great Recession ended.

The Sep unemployment rate on Friday is expected to fall by -0.1 point to 3.8%, thus matching the 48-year low posted in May. The consensus is for Sep average hourly earnings to ease slightly to +2.8% y/y from August’s 9-year high of +2.9%. If the earnings report does not ease a bit as expected, then the markets will become more concerned about wage-push inflation.

U.S. ISM non-manufacturing index expected to indicate continued strong business confidence — The market consensus is for today’s Sep ISM non-manufacturing index to show a -0.5 point decline to 58.0, giving back some of August’s +2.8 point surge to 58.5. The index was in strong shape in August at only 1.4 points below January’s 13-year high of 59.9. The ISM manufacturing index for September, which was released this past Monday, fell by -1.5 points so 59.8, which supported expectations for a decline in today’s non-manufacturing report.

U.S. business confidence remains very strong due to (1) the strong Q2 GDP rate of +4.2%, (2) the generally solid global economy, and (3) flush cash positions from the Jan 1 tax cuts. Negative factors include (1) tariffs, (2) high gasoline prices, and (3) political worries. Sunday’s NAFTA 2.0 agreement will be a big positive for U.S. business confidence in the October statistics, although there is still considerable worry that the US/Chinese trade war is likely to get significantly worse in coming months.

Italian 10-year yield reaches another new 4-1/2 year high as Italian officials continue to disregard market forces — The Italian stock and bond markets on Tuesday extended the sharp sell-offs seen since last Friday when news emerged of a 2019 budget deficit of 2.4% of GDP. The deficit is expected to remain near 2.4% in 2020 and 2021 as well, which would further swell Italy’s massive debt that is already above 130% of GDP.

The government’s budget plan will be presented to the Italian parliament today and must be forwarded to the European Commission by October 15 for their review. The European Commission can demand changes in the budget to meet Eurozone fiscal commitments.

The markets became more concerned about the Italian situation on Tuesday after Claudio Borghi, head of the lower house budget committee, said in a radio interview that the euro was “not sufficient” to solve Italy’s problems, implying that Italy should dump the euro. Mr. Borghi later walked back that comment by telling Bloomberg TV that “There is no plan to leave the euro within this government regardless of my personal conviction.” He added that “we are not mad” and “we are not Venezuela.”

The iShares Italy ETF (EWI) on Tuesday fell by another -0.47%, bringing the 4-session plunge to -6.5%. Italy’s 10-year bond yield on Tuesday rose by another +15 bp to a new 4-1/2 year high of 3.45%, bringing the 3-day surge to an extraordinary +56 bp. The 10-year bond yield has spiked higher by +170 bp since last May when the populist government took power. The spread of the Italian 10-year bond yield over Germany rose by another +20 bp on Tuesday to a new 5-1/4 year high of 303 bp, taking out the previous high of 291 bp posted in August.

EIA weekly Petroleum Status Report –– The consensus for today’s weekly EIA report is for a +1.0 mln bbl rise in U.S. crude oil inventories, a +1.0 mln bbl rise in gasoline inventories, a -1.5 mln bbl decline in distillate inventories, and a -1.0 point drop in the refinery utilization rate to 89.4%. U.S. crude oil inventories are currently mildly tight at -2.2% below the 5-year seasonal average. Product inventories are mixed with gasoline inventories 8.4% above average and distillate inventories -3.6% below average. U.S. oil production in last week’s report rose to a new record high of 11.1 million bpd. U.S. oil production has doubled over the last six years.