- FOMC expected to move ahead with a rate cut in two weeks due to downside risks as US/China trade tensions continue

- UK/EU Brexit deal is reportedly close but the question would then be UK Parliamentary approval

- U.S. retail sales expected to show a solid increase

FOMC expected to move ahead with a rate cut in two weeks due to downside risks as US/China trade tensions continue — The global downside risks continue to be significant in the run-up to the FOMC meeting in two weeks (Oct 29-30). In fact, the IMF yesterday downgraded its global GDP forecast to a 10-year low of +3.0% from July’s estimate of +3.2%. Today’s Beige Book from the Fed will provide some additional data on the state of the U.S. economy.

The US/Chinese economic war shows no real sign of abating, which keeps the global risks skewed to the downside. In some good news, President Trump last Friday scrapped the tariff hike to 30% from 25% on $250 billion of Chinese goods that would have taken effect yesterday. However, Mr. Trump did not mention any willingness to scrap the upcoming 15% tariff on the last $160 billion of Chinese goods that is scheduled for Dec 15. There was no apparent consideration of rolling back existing U.S. penalty tariffs on $360 billion of Chinese goods and the Chinese retaliatory tariffs on $110 billion of U.S. goods.

Mr. Trump seems to be expecting China to boost its spending on U.S. ag products to $40-50 billion within two years from pre-tariff levels of $20 billion without any assurance of tariff relief. Indeed, Bloomberg reported yesterday that China is not likely to agree to $50 billion of U.S. ag purchases without a rollback of current U.S. tariffs. The markets are therefore in for a long few weeks as they wait to see if the two sides can iron out a written “first phase” deal to be signed by Presidents Trump and Xi at the Nov 16-17 APEC Summit in Santiago, Chile.

The trade uncertainty means that the global economy will still be facing major downside risks when the FOMC meets in two weeks. Fed officials are clearly reluctant to ease another notch given that they have already cut rates twice and that the U.S. economy is still growing at or above the potential U.S. growth rate of +1.9%. The latest set of Fed dots from the September meeting showed a median forecast for no more rate cuts in 2019 or 2020 and then a 25 bp rate hike in 2021 and a second rate hike in 2022.

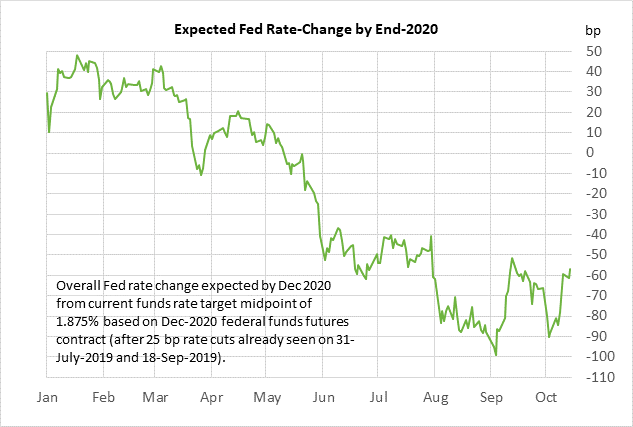

Yet the markets still strongly believe that the FOMC will go ahead with another rate cut at its meeting in two weeks. The market is discounting an 85% chance that the FOMC will cut the funds rate by another 25 bp to 1.50%/1.75% at the upcoming Oct 29-30 meeting (based on the federal funds futures market relative to the current mid-point target rate of 1.875%). The market is discounting an overall 57 bp rate cut (2.3 rate cuts) through the end of 2020.

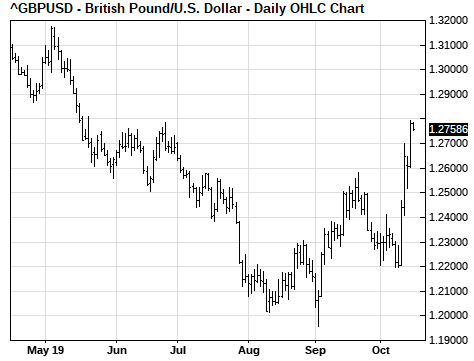

UK/EU Brexit deal is reportedly close but the question would then be UK Parliamentary approval — Reports of progress on a Brexit deal caused GBP/USD on Tuesday to rally by another +1.4%, bringing the rally since last Wednesday to a total of +4.8%.

Details were scant but a deal reportedly involves a return to a previous solution of a Northern Ireland-only backstop whereby Northern Ireland would be required to remain within EU’s single-market rules, with a customs border on the Irish Sea, until a full UK/EU trade deal could be reached. There was no word on whether there would be a time limit on the backstop, as many Brexiteers demanded when Theresa May was Prime Minister. There was also no word on whether the deal would be subject to the approval of Northern Ireland’s Assembly.

Even if there is a Brexit deal within the next day or two that is agreed upon by EU negotiators and Prime Minister Johnson, the key will be whether PM Johnson could get it approved by the UK Parliament in a planned session on Saturday. The UK Parliament has so far voted down every Brexit deal it has considered. Prime Minister Johnson currently presides over a minority government and he will struggle to get enough votes to approve a Brexit deal since the opposition parties are likely to vote against the deal.

The most critical factor for any Brexit deal is whether it is approved by the Northern Irish Democratic Unionist Party (DUP). The DUP only has 10 seats in Parliament but the DUP is a coalition partner with the Conservative Party. Moreover, there are a significant number of Conservative Party MPs who will not vote for a Brexit deal unless it is acceptable to Northern Ireland and the DUP. PM Johnson on Tuesday met with DUP leaders for 90 minutes but those DUP leaders refused to give up thumbs up or down on the deal and would only say that more work was needed.

The markets, in any case, are not particularly worried about a no-deal Brexit. If there isn’t a Brexit deal this week, then UK/EU negotiations will continue right up until the Oct 31 deadline. In addition, the UK Parliament’s Benn Act requires PM Johnson to request an extension if there is no Brexit deal by Saturday. The betting markets are discounting only a small 15% chance of a no-deal Brexit this year, according to oddschecker.com.

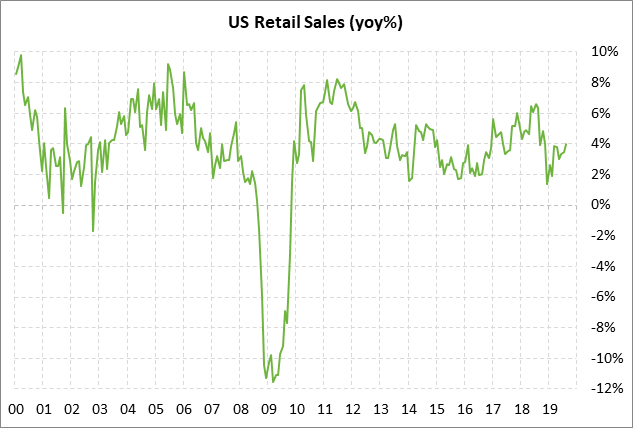

U.S. retail sales expected to show a solid increase — The consensus is for today’s Sep retail sales report to show an increase of +0.3% and +0.2% ex-autos following Aug’s report of +0.4% and unchanged ex-autos. Retail sales have been very strong for the last six consecutive months and were up by a solid +4.0% y/y in August.

Yet there are questions about consumer spending going forward as the economy slows and as political uncertainty rises. The Conference Board’s consumer confidence index fell by -1.6 points in Aug and by -9.1 points in Sep to a 3-month low. However, that slide in confidence was not confirmed by the University of Michigan’s consumer sentiment index, which fell by -8.6 points in August but then rose by +3.4 points in September and +2.8 points in October.