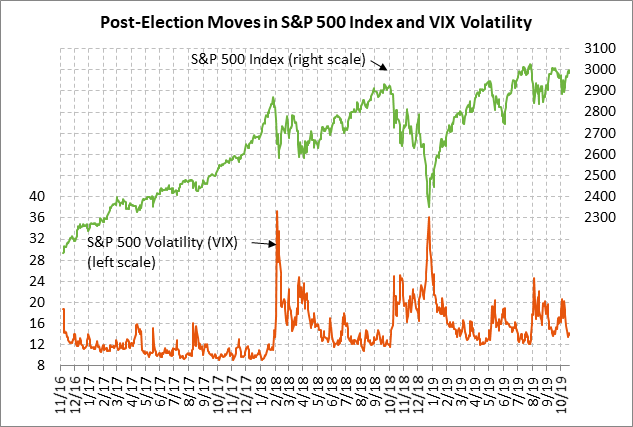

- Weekly global market focus

- Key Brexit vote delayed to this week

- US/Chinese phase-one trade talks continue with less than four weeks until APEC summit

- Q3 earnings deluge this week

Weekly global market focus — The U.S. markets this week will focus on (1) the status of the ongoing US/Chinese talks to finalize the phase-one trade agreement, (2) this week’s heavy Q3 earnings schedule with 131 of the S&P 500 companies scheduled to report, (3) the Treasury’s sale of $133 billion of T-notes this week, (4) Fed policy ahead of next week’s FOMC meeting where the market is now discounting a 100% chance of a rate cut, and (5) this week’s U.S. economic calendar with key reports including home sales and home price reports, durable goods orders, and consumer sentiment.

The European markets this week will focus mainly on Brexit. The market is expecting the ECB to leave its policy unchanged at its meeting on Thursday, which will be the last for ECB President Draghi. Key European economic reports include the PMI reports on Thursday and German confidence reports on Friday.

The Asian markets this week will focus mainly on the ongoing US/Chinese trade talks. The Japanese markets are closed on Tuesday for a national holiday.

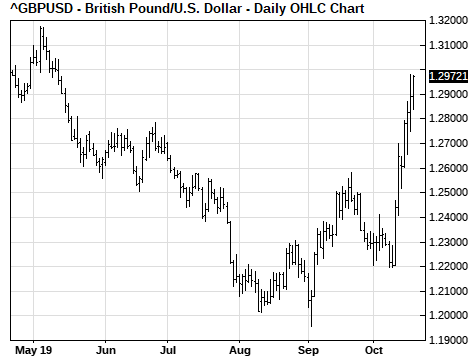

Key Brexit vote delayed to this week — The UK Parliament as soon as today may be asked to vote on Prime Minister Johnson’s Brexit deal in principle, with a follow-up vote on Tuesday on the Brexit implementation legislation. Sterling on Sunday night traded -0.8% lower after the weekend events.

The UK Parliament on Saturday voted to delay consideration of PM Johnson’s Brexit deal in order to force Mr. Johnson to request an extension of the Oct 31 Brexit deadline. Mr. Johnson on Sunday in fact sent a letter to the EU requesting that delay, although he did not sign the letter and sent a second letter arguing that a delay in Brexit would be a mistake.

It remains to be seen whether the EU will consider Mr. Johnson’s request as sufficient to respond with an extension, but the EU in any case seems willing to provide an extension of at least 3 months. The EU this week may delay granting the extension until it sees the outcome of any Parliament votes today and Tuesday, since an extension will not be necessary if Parliament approves both the principle of the deal as well as the implementation legislation before the October 31 deadline.

Mr. Johnson this week appears to have a respectable chance of getting Parliament to approve his Brexit deal. Mr. Johnson on Saturday lost the vote on a Brexit delay by only 322/306. Some MPs voted for the delay, not because they opposed the Brexit deal on the merits, but because they wanted a delay to force an extension request. Thus, a vote on the Brexit deal itself will do better than the 322/306 vote on the delay.

If Parliament approves both the deal in principle and the implementation legislation, then the UK will withdraw from the EU on October 31. The UK would then enter a smooth transition period through the end of 2020 during which the UK will continue to operate until the EU’s single-market rules.

However, if Parliament rejects Mr. Johnson’s Brexit deal and the EU provides the extension, then a no-deal Brexit on Oct 31 will be avoided but the Brexit saga will continue. In that case, the UK may hold a general election by the end of the year to try to break the impasse in Parliament. The betting odds of a no-deal Brexit on October 31 remain very low at 11% (8/1), according to oddschecker.com.

US/Chinese phase-one trade talks continue with less than four weeks until APEC summit — Treasury Secretary Mnuchin last week said that US/Chinese talks will continue this week on the phone as they try to finalize the “phase one” trade agreement that was announced on Oct 11. Chinese Vice Premier Liu on Saturday said that, “China and the U.S. have made substantial progress in many aspects, and laid an important foundation for a phase one agreement.”

The goal continues to be to have a written agreement that can be signed by Presidents Trump and Xi at the upcoming APEC Summit in Chile on Nov 16-17.

President Trump on Oct 11 said that the phase one agreement could result in annual Chinese purchases of U.S. ag products of as much as $40-50 billion, but China responded through leaks to the press by saying that ag purchases that high would require roll-backs of U.S. tariffs. So far, President Trump has scrapped only the tariff hike to 30% from 25% on $250 billion of Chinese goods that was due to go into effect on Oct 15. Mr. Trump still has in effect his plan to slap a 15% tariff on the last $160 billion of Chinese goods on Dec 15.

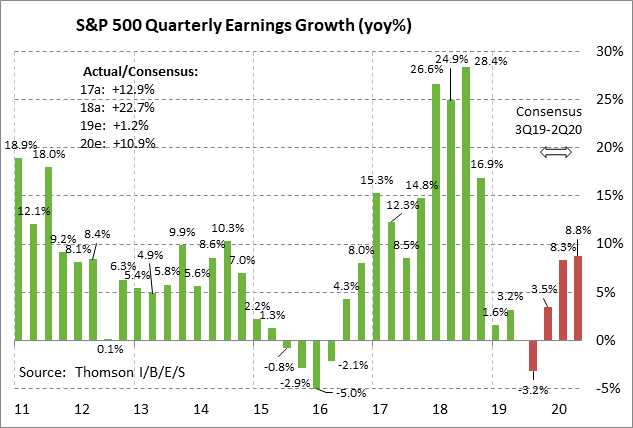

Q3 earnings deluge this week — There is a deluge of Q3 earnings reports this week with 131 of the SPX companies reporting. Notable reports this week include UPS and PulteGroup on Tuesday; Microsoft, Boeing, and Caterpillar on Wednesday; Amazon.com, Twitter, Visa, and CapitalOne on Thursday; and Verizon on Friday.

The consensus is for Q3 SPX earnings growth of -3.1% y/y, according to Refinitiv. Looking ahead the consensus is for SPX earnings growth of +2.7% in Q4, +7.7% in Q1, and 7.9% in Q2. On a calendar basis, earnings growth in 2019 is expected to slump to +1.2% from 2018’s stellar pace of +22.7%.

Earnings reports have thus far been better than expected. Of the 73 reporting SPX companies, 83.6% have reported above-consensus earnings, which is better than the long-term average of 64.8% and the 4-quarter average of 74.1%, according to Refinitiv.