- Trump administration sources claim trade deal will be done by next week

- OPEC+ continues to struggle with massive excess global oil production capacity

- U.S. factory orders expected to edge higher

- U.S. trade deficit expected to narrow sharply

Trump administration sources claim trade deal will be done by next week — Bloomberg on Wednesday reported that “people familiar with the talks” said that the US/Chinese trade talks remain on track and that they expect a phase-one trade deal to be completed before the Dec 15 tariff deadline, which is now only 10 days away. The sources told Bloomberg that the only outstanding issues are how to guarantee China’s purchase of U.S. ag products and exactly what tariffs will be rolled back.

The article appeared to be an attempt by at least one Trump administration official to counteract the market damage done on Tuesday when President Trump told reporters that, “I don’t have a deadline” for a trade deal and, “I like the idea of waiting until after the election for a China deal.”

The S&P 500 index on Wednesday rebounded higher by +0.63% on the Bloomberg report, largely reversing Tuesday’s -0.66% sell-off. The markets remain generally optimistic that a deal will get done, though perhaps not by Dec 15. The markets will not be overly worried if a deal slips into early 2020 as long as President Trump seems satisfied with the progress of the talks and agrees to delay the Dec 15 tariffs.

However, if the US/Chinese talks should suddenly fall apart, U.S. stocks would fall sharply since the markets would then expect a series of new Trump tariff rounds on Chinese goods, along with Chinese retaliation.

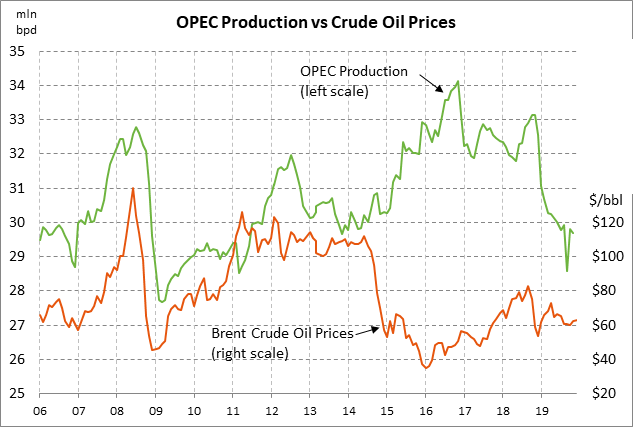

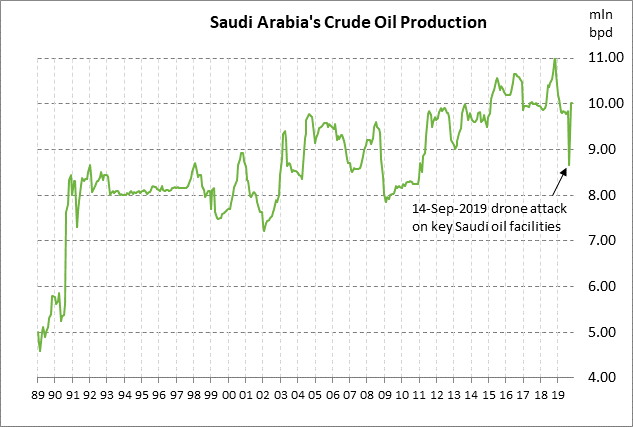

OPEC+ continues to struggle with massive excess global oil production capacity — OPEC+ meets today and Friday with a variety of possible outcomes. However, the long-term picture for the oil market will remain overwhelmingly bearish since there is an ever-present threat of a plunge in oil prices if OPEC+ wavers in its production cut stance.

There is a huge amount of excess oil production capacity across the world, which grows by the year as oil extraction technology improves and becomes cheaper. Production capacity is simply outstripping demand, leading to the need for the OPEC+ production cut to balance supply and demand. Without the OPEC+ production cut agreement, oil prices would already be at sharply lower levels.

The market consensus is that OPEC+ this week will extend its 1.2 million bpd production cut by 3-6 months beyond the current expiration date of March 2020. However, there is a chance that OPEC+ will defer any decision until Q1 in line with Russia’s preferences. Alternatively, Saudi Arabia may push for the agreement to be extended to the end of 2020 to support oil prices and provide more confidence to the markets that there won’t be a surge in production when the agreement ends in 2020. The markets are already worried about an expected global oil surplus in the first half of 2020.

Jan WTI crude oil prices on Wednesday surged by $2.33 per barrel (+4.15%) to $58.43 on reports that Saudi Arabia is talking up a new production cut of 400,000 bpd beyond the current 1.2 million bpd cut, for a total cut of 1.6 million bpd. However, that was viewed by some as a ploy to boost oil prices ahead of the pricing of Saudi Arabia’s Aramco IPO deal.

Moreover, Saudi Arabia, in any new production cut, would not cut production itself, but would instead rely on the current quota-cheaters in OPEC+ such as Iraq and Russia to shoulder the burden. Moreover, a new 400,000 bpd cut agreement would not result in any real cut in production since current production levels are already about 300,000 bpd less than the official OPEC production target. Saudi Arabia’s talk of a further 400,000 bpd production cut seems to be more of a PR move for its Aramco IPO and a threat to OPEC+ cheaters that they better start complying with their existing production cut quotas.

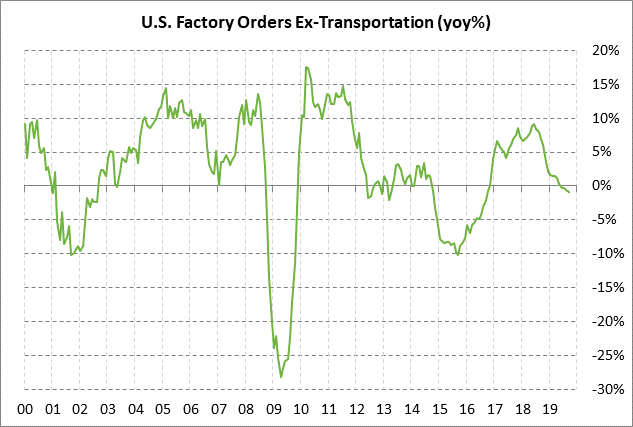

U.S. factory orders expected to edge higher — The market consensus is for today’s Oct factory orders report to show a small +0.3% increase following Sep’s weak report of -0.6% and -0.1% ex-transportation. Even a small increase in factory orders today would be a welcome development since factory orders on a year-on-year basis in September were down -3.5% y/y headline and -0.9% y/y core.

The U.S. manufacturing sector is mired in a recession. The Nov ISM manufacturing index fell by -0.2 to 48.1, where the index was only 0.3 points above Sep’s 10-year low of 47.8 and remained below the expansion-contraction level of 50.0 for the fourth straight month. Meanwhile, U.S. manufacturing production in October fell by -1.5% y/y and remained in negative year-on-year territory for the fourth consecutive month (July-Oct).

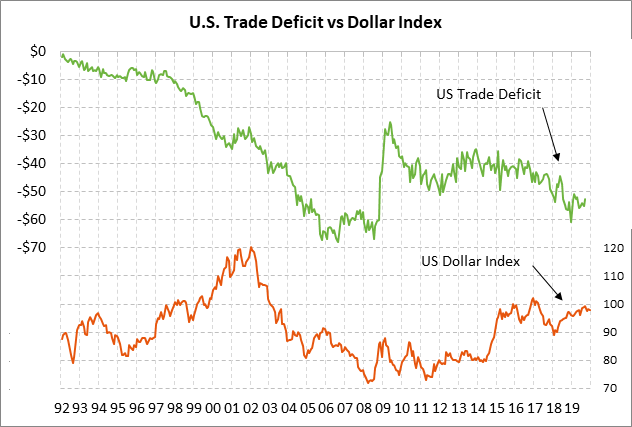

U.S. trade deficit expected to narrow sharply — The market consensus is for today’s Oct U.S. trade deficit to narrow substantially to -$48.6 billion from Sep’s -$52.5 billion. Today’s expected report of -$48.6 would leave the deficit at a 15-month low and substantially below the 12-month trend average of -$54.4 billion.

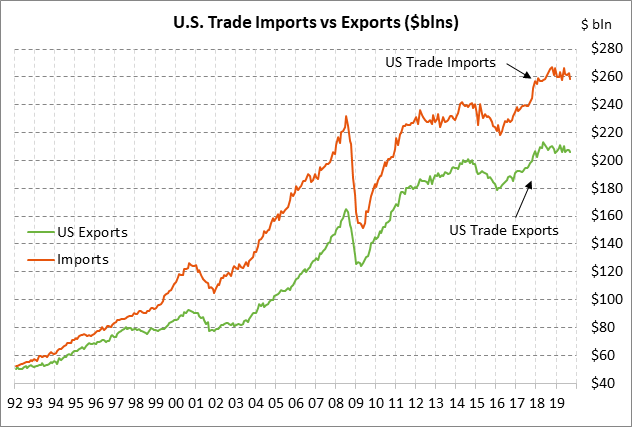

U.S. imports and exports have both been moving mostly sideways since the tariff war began in early 2018. U.S. imports have been undercut by U.S. tariffs on imports from China and elsewhere. Meanwhile, U.S. exports have been hurt by (1) retaliatory tariffs on U.S. goods, (2) the generally strong dollar, and (3) weak overseas economic growth. The U.S. trade deficit has widened since the tariff war began.

The U.S. trade deficit with China (on a 12-month cumulative basis) widened when the U.S. tariff war began but has since narrowed to -$381 billion and is now close to where it was before the tariff war began in spring 2018.