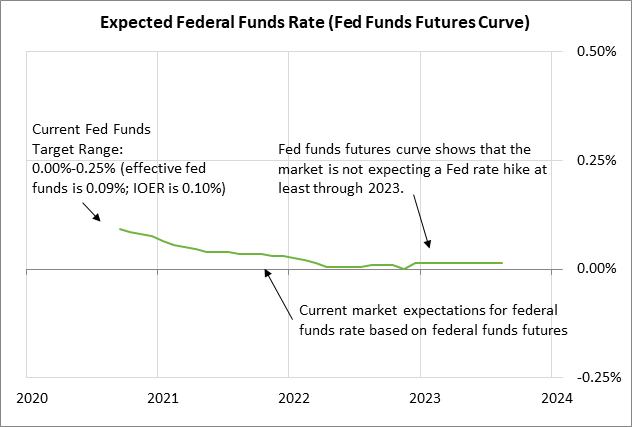

- Markets take in stride FOMC plan to keep rates near zero through 2023

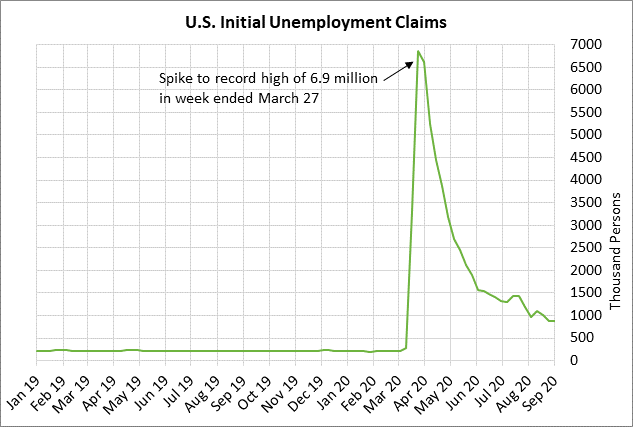

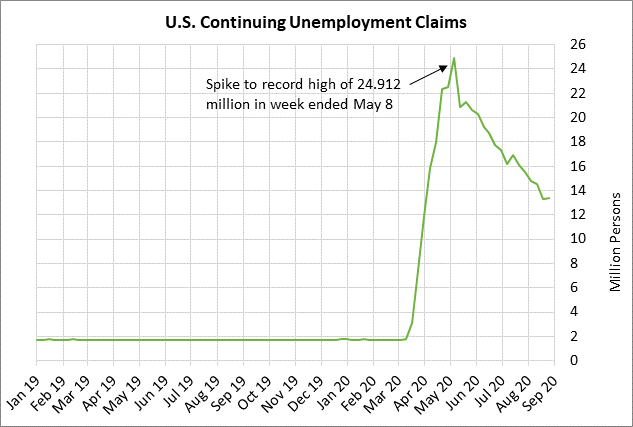

- Unemployment claims expected to show continued improvement but remain high

- U.S. housing starts expected to remain strong

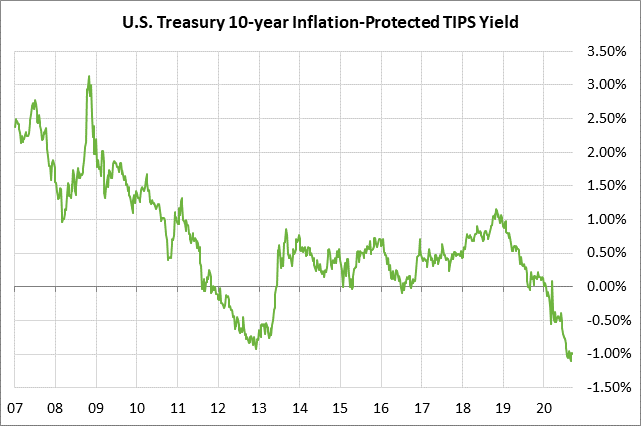

- 10-year TIPS auction to yield near -1.00%

Markets take in stride FOMC plan to keep rates near zero through 2023 — The FOMC, at its 2-day meeting that ended yesterday, made clear that it does not plan to raise interest rates for at least the next 3 years. The new Fed-dot forecast contained a median forecast for the funds rate to remain unchanged near zero through the end of 2023.

In addition, the Fed issued new interest guidance saying that it will not raise interest rates until both its inflation and employment targets are met, and inflation is on its way to overshooting its 2% target. The Fed’s latest macroeconomic forecasts indicate that it doesn’t expect that combination of events to happen until at least 2023.

The dovish outcome of the meeting was largely in line with market expectations, although the new interest rate guidance came sooner than expected. The federal funds futures curve showed no change out to the mid-2021 contracts and only a 1 bp tightening for the contracts from mid-2021 through mid-2023. The Eurodollar futures curve showed a similar movement, except that the longer-dated contracts from 2025 through 2029 showed a 2 bp tightening.

Meanwhile, the 10-year T-note yield moved higher by about +2 bp to 0.697% and closed the day up +1.8 bp after Fed Chair Powell in his press conference dashed hopes that the Fed might shift its QE buying toward longer-dated Treasury securities. Mr. Powell indicated that the Fed is satisfied with its current QE program and has no near-term plan for changes.

There is talk in the markets that the Fed might eventually move some of its Treasury buying towards the longer-end of the Treasury curve to keep longer-dated Treasury yields from rising. Mr. Powell did say yesterday that the Fed is prepared to adjust its asset-buying as appropriate. The Fed may eventually increase the size of its purchases of longer-term Treasury securities if longer-term Treasury yields start rising and the Fed wants to intervene to cap those yields. That idea is currently premature with longer-term Treasury yields trading sideways at extraordinarily low levels.

The new Fed-dot forecast showed a median forecast for an unchanged funds rate near zero through the end of 2023. However, one of the 17 FOMC members expect a rate hike by 2022, and four members expect a rate hike by 2023.

Regarding the new interest rate guidance, the FOMC said it will not raise rates from the current level until its inflation and labor market goals are met. The FOMC’s post-meeting statement said, “The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”

Since the Fed is forecasting the longer-run unemployment rate at 4.1%, the implication is that the Fed will not start raising interest rates until the unemployment falls by more than half to 4.1% from the current level of 8.4% level seen in August.

Unemployment claims expected to show continued improvement but remain high — Today’s unemployment claims report is expected to show a continued slow improvement in the labor market. The consensus is for today’s initial unemployment claims report to show a -34,000 decline to 850,000 after last week’s report of unchanged at 884,000. Meanwhile, today’s continuing claims report is expected to show a -385,000 decline to 13.000 million after last week’s +93,000 rise to 13.385 million.

Initial claims in the past two weeks fell to a 6-month low, and continuing claims fell to a 5-month low. However, initial claims are still 687,000 above the pre-pandemic level seen in February and continuing claims are 11.593 million higher than the pre-pandemic level. That shows that there are still 11.6 million people that are on the unemployment rolls because of the pandemic. Moreover, there are many more people who are unemployed but who aren’t getting unemployment benefits because they don’t qualify for one reason or another or worked off-the-books.

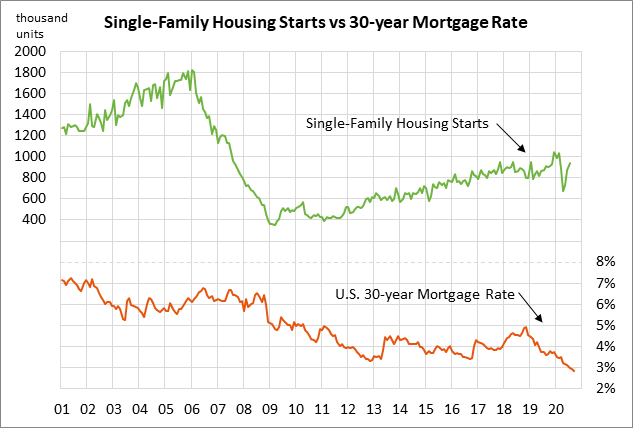

U.S. housing starts expected to remain strong — The consensus is for today’s Aug housing starts report to show a -0.9% decline to 1.483 million, falling back slightly after July’s surge of +22.6% to 1.496 million. Housing starts in the past three months have surged from pandemic lows and would need to rise by only another 8% to reach January’s 13-1/2 year high of 1.617 million.

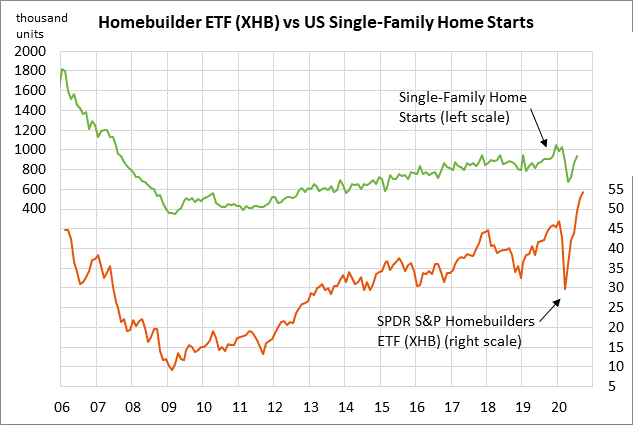

U.S. housing starts have surged as U.S. homebuilders respond to the spike in demand for new homes from people looking to take advantage of low mortgage rates, to move into larger homes, or to move away from urban areas. The NAHB housing index yesterday unexpectedly rose by 5 points to a record high of 83 (data since 1985), illustrating the extremely strong optimism among U.S. homebuilders. The SPDR S&P Homebuilders ETF (XHB) edged to a new record high yesterday (data since 2006) and is up +19.0% on a year-to-date basis, which is much better than the +4.8% year-to-date gain in the S&P 500 index.

10-year TIPS auction to yield near -1.00% — The Treasury today will sell $12 billion of 10-year TIPS in the first reopening of July’s 1/8% 10-year TIPS of July 2030. The benchmark 10-year TIPS yield yesterday closed at -0.997%. The 12-auction averages for the 10-year TIPS are: 2.45 bid cover ratio, $23 million in non-competitive bids, 6.6 bp tail to the median yield, 25.6 bp tail to the low yield, 58% taken at the high yield, and 66.8% taken by indirect bidders (higher than the median of 63.6% for all recent Treasury coupon auctions).