- President Trump tries some oil diplomacy but oil fundamentals are too dismal

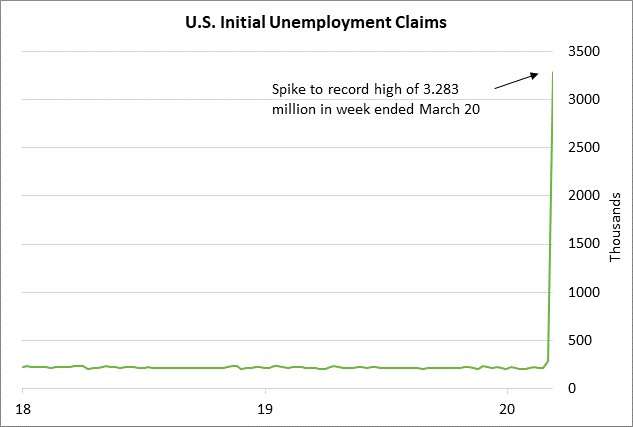

- U.S. unemployment claims expected to surge by another 3.5 million

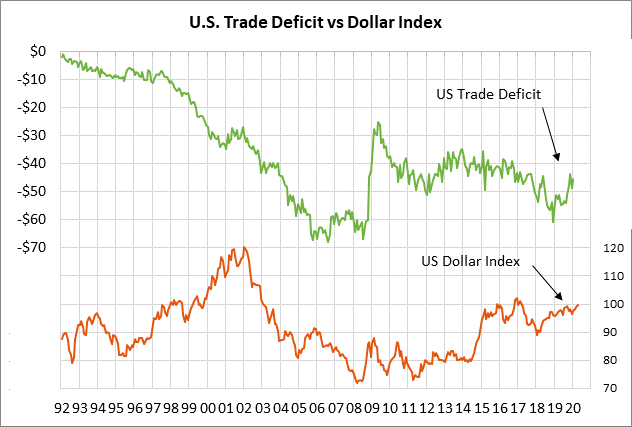

- U.S. trade deficit expected to narrow

President Trump tries some oil diplomacy but oil fundamentals are too dismal — President Trump on Friday is scheduled to meet with top oil company officials to discuss the dire situation facing the global oil markets. In addition, President Trump has called both Russian President Putin and Saudi Prince MBS to try to get them to start cooperating again. Mr. Trump is worried about what could be the complete collapse of the U.S. oil production industry if the current slump in oil prices persists or worsens. Indeed, Whiting Petroleum on Tuesday filed for bankruptcy since it couldn’t pay its debt of more than $250 million. There will be more bankruptcies to come in the U.S. shale patch.

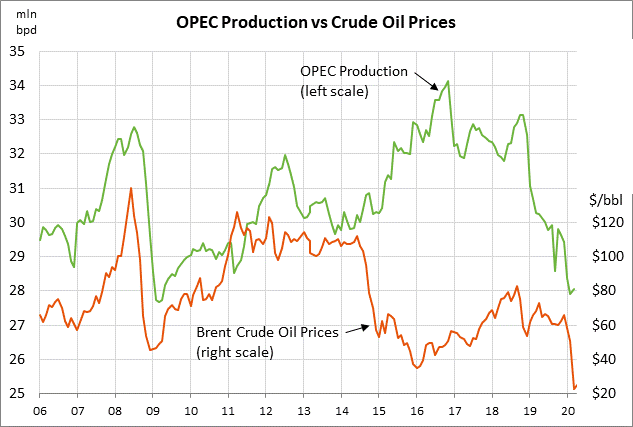

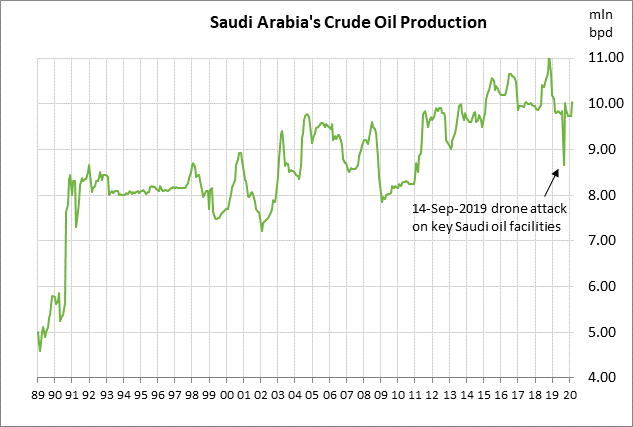

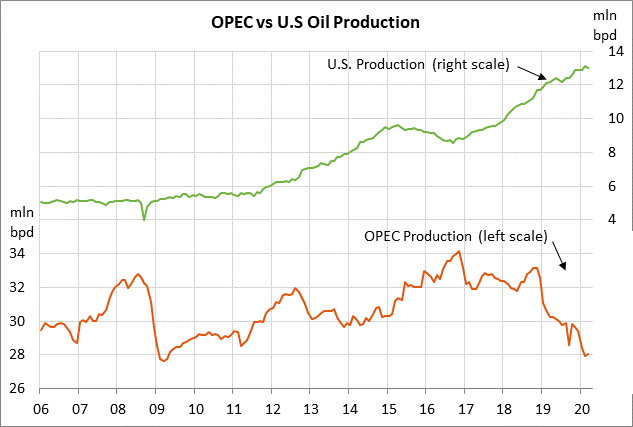

However, there isn’t much anyone can do right now to put a dent in the size of the problem that the oil market faces. The oil market’s biggest problem is the plunge in global oil demand on the order of 20-30%, totaling some 25 million bpd. Global transportation has dropped off sharply, thus reducing fuel demand. The massive drop in demand couldn’t even be fully offset if Saudi Arabia (with 10 million bpd of production) and Russia (with 11.3 million bpd of production) both agreed to cut their production to zero, which obviously isn’t even a consideration.

The reinstatement of the Q1-2020 OPEC+ production cut agreement of 1.7 million bpd would be a drop in the bucket at this point for near-term oil prices, although it could at least spark a rally in the back-month crude oil futures contracts that are more willing to price in the end of the pandemic. Saudi Arabia has suggested that it might be interested in talking if all the oil producers in the world would cooperate in a production cut, including the United States. Russia has indicated that it will not be raising production, but it has not indicated any willingness for a new production cut.

Meanwhile, the oil fundamentals grow worse by the day as the global oil surplus grows. Saudi Arabia in March already boosted its production by 290,000 bpd (+3.0%) to 10.0 million bpd and is in the process of boosting its output by another 20% in April to 12.0 million bpd. It will not be long before the world’s oil storage facilities will be completely full, at which point some companies will have to stop producing oil since there won’t be anywhere to put that oil.

Oil prices received a boost on Wednesday on reports that the Energy Department is considering renting out space in the Strategic Petroleum Reserve for private parties to store their oil. That would take at least some oil out of the market. President Trump was turned down in the recent $2 trillion rescue bill on his request for $3 billion to buy oil to fill up the Strategic Petroleum Reserve (SPR). However, he could get that money in the next deal if Republicans agree to give Democrats increased support for renewable energy.

In the meantime, the Energy Department has about 78.5 million barrels of room to spare in the SPR. The SPR’s current level of 635 million barrels is at 89% of the storage capacity of 713.5 million. However, that isn’t very much space since it would only take six days to fill up the SPR if all of America’s 13.0 million bpd of production were to be diverted to the SPR.

The emerging oil surplus was highlighted by yesterday’s news that EIA U.S. crude inventories soared by +13.83 million bbl to a 9-month high of 469.19 million bbl, well above expectations of +4.0 million bbl. In addition, crude supplies at Cushing, the delivery point for WTI crude oil futures, rose +3.52 million bbl.

May WTI crude oil prices on Wednesday closed -$0.17 (-0.83%) at $20.31, which was just mildly above last Friday’s 18-year low of $19.27. The plunge in oil prices has been a contributing factor, along with the plunge in the global economy, in pushing inflation expectations sharply lower. The current U.S. 10-year breakeven inflation expectations rate of 0.91% is down sharply by 74 bp from the mid-February pre-pandemic levels near 1.65%, which in turn has been a major bullish factor for T-note prices.

U.S. unemployment claims expected to surge by another 3.5 million — The consensus is for today’s weekly initial unemployment claims report for the week ended last Friday (March 27) to show another surge of 3.500 million, which would be 217,000 higher than last week’s report of 3.283 million. Last week’s surge in claims was quadruple the previous weekly record.

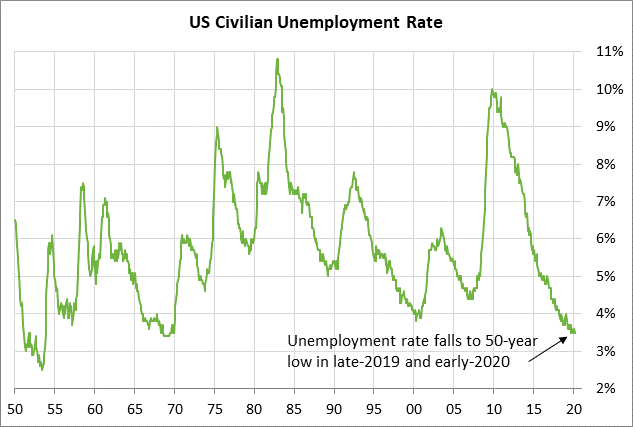

Goldman Sachs is projecting that the U.S. unemployment rate will surge from the current 50-year low of 3.5% to 15% by mid-year, which would be higher than the peak of 10.1% seen during the Great Recession in 2007/09 and the post-war record high of 10.8% posted in 1982.

The markets are closely watching the claims data because it provides a much timelier indication of what is happening on the ground, as compared with the monthly economic reports that are of little use at this point. Yesterday’s March ADP report, for example, showed a decline of only -27,000 jobs, which was a much smaller decline than expectations of -150,000. The consensus is for Friday’s March payroll report to show a decline of -100,000 jobs and for the March unemployment rate to rise by +0.3 points to 3.8% from Feb’s 50-year low of 3.5%.

U.S. trade deficit expected to narrow — The consensus is for today’s Feb trade deficit to narrow to -$40.0 billion from -$45.3 billion in January. Today’s report will only show a minor impact from the pandemic since the big economic impact in the U.S. didn’t hit until March. Starting in March, the pandemic will cause a sharp drop in both U.S. imports and exports as world trade dries up. On the trade front, President Trump has not made any mention of getting the phase-two trade talks started with China since dealing with the pandemic is currently much more important.