- S&P 500 extends its drop as virus concerns continue to grip the markets

- Commodity indexes fall to new lows and help push inflation expectations lower

- Q4 GDP expected unrevised at +2.1%

- 7-year T-note auction

S&P 500 extends its drop as virus concerns continue to grip the markets — The U.S. stock market rallied early Wednesday on some short-covering, but then starting sinking again after news that health officials in New York are monitoring 83 people who have visited mainland China or have come into contact with the coronavirus. In addition, the first case emerged in the U.S. on Wednesday of a person in Northern Californian who caught the virus from an unknown origin with no known connection to foreign travel, suggesting the possible first case of the community spread of the virus.

The markets continue to worry about the CDC’s warning on Tuesday that it is inevitable that the U.S. will start seeing the community spread of the coronavirus, which could lead to travel restrictions and business and school closures in affected areas. Also, Germany’s Health Minister on Wednesday said, “Germany is at the beginning of a coronavirus epidemic.” Confirmed cases of the virus are now reported globally at 81,412 in more than 30 countries, with 2,773 deaths.

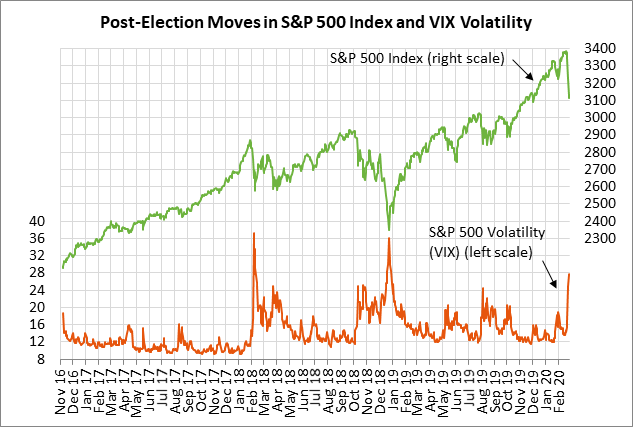

The S&P 500 index on Wednesday edged to a new 2-1/4 month low and closed the day down -0.38%. On Wednesday’s low, the S&P 500 index corrected lower by a total of -8.4% from last Wednesday’s record high and retraced 27% of the extraordinary 44.6% rally seen over the past 14 months from the 3-year low posted in Dec 2018.

Tech and momentum stocks held up better than the S&P 500 index on Wednesday and managed to avoid falling below Tuesday’s lows. From last week’s respective record highs, the Nasdaq-100 index on Tuesday corrected lower by a total of -9.5%, and the NYSE Fang+ index corrected lower by a larger -11.2%.

The VIX S&P 500 volatility index on Wednesday fell back from Tuesday’s 14-month high of 30.25 and closed the day -0.29 at 27.56%. The VIX on this week’s upward trajectory has so far remained below the 2-year high of 36.20 posted in December 2018 when the S&P fell on a heavy downside correction, and also below the 4-1/2 year high of 50.30 posted in Feb 2018 when Volmageddon caused some VIX products to blow up.

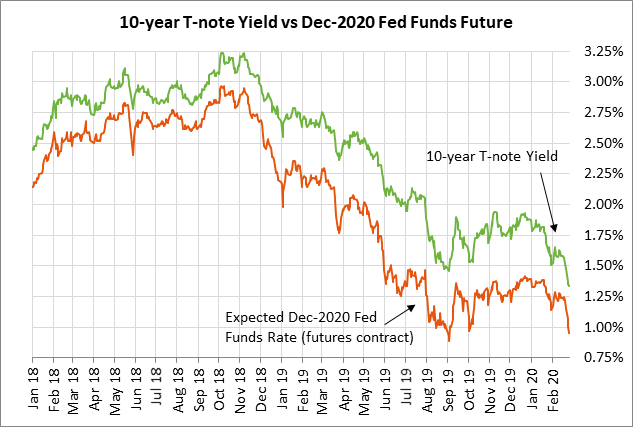

The 10-year T-note yield on Wednesday edged below Tuesday’s low to post a new record low of 1.299%, finally closing the day down -1.5 bp at 1.337%. Market expectations for Fed easing through year-end increased by another 5.5 bp to 67.5 bp (2.7 rate cuts) on Wednesday, with the Dec 2020 federal funds futures contract breaking below the 1.00% level to close at a yield of 0.95%.

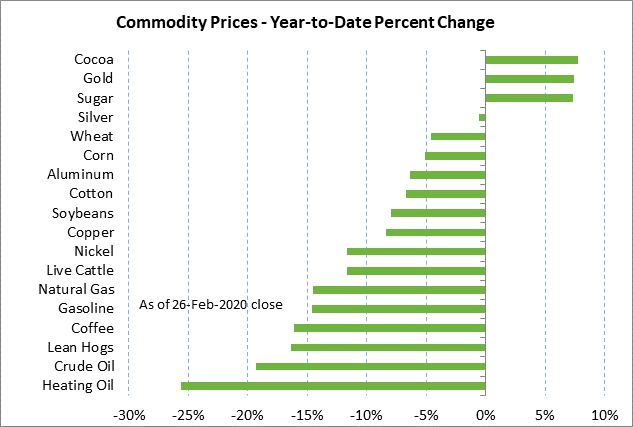

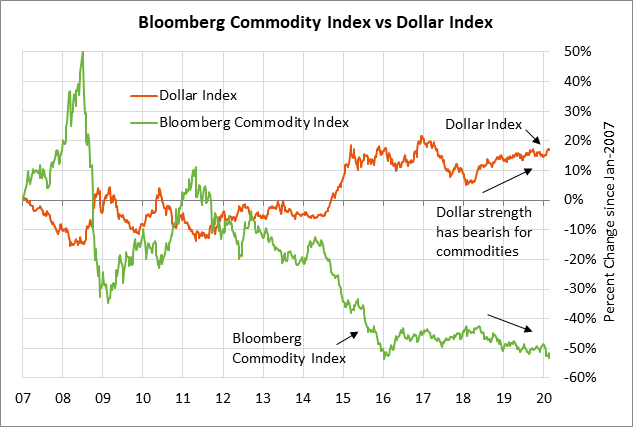

Commodity indexes fall to new lows and help push inflation expectations lower — Commodity prices, in general, continue to be pummeled by the stronger dollar and by concern about reduced commodity demand caused by the coronavirus crisis. The Thomson Reuters Equal Weight Commodity Index (CCI) has plunged by an overall -4.4% since last week and fell to a new 4-3/4 month low on Wednesday. The Bloomberg Commodity index since last week has plunged by an overall -4.1% and fell to a new 4-year low on Wednesday.

As the nearby chart shows, energy and industrial metals prices have plunged this year on concern about sharply reduced demand caused by the coronavirus. U.S. ag products have also been hurt by the strong dollar and by concern that China will not be able to make good on its phase-one trade deal promise to buy more U.S. ag products since its economy has been decimated by the coronavirus.

The plunge in commodity prices in the past week has helped push inflation expectations to new lows. The 10-year breakeven inflation expectations rate on Wednesday closed at 1.55%, which was just 2 bp above Tuesday’s 4-1/2 month low of 1.53% and far below the Fed’s +2.0% inflation target.

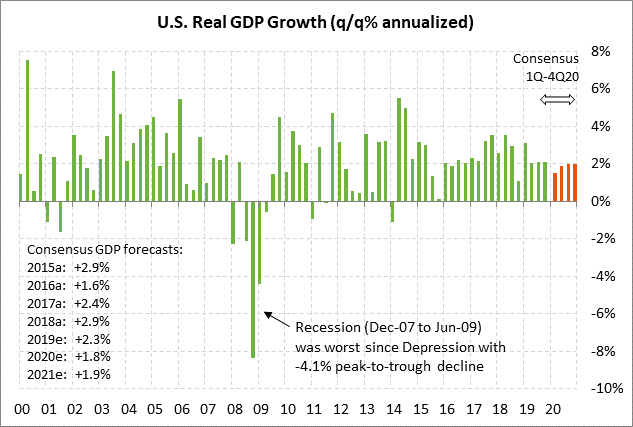

Q4 GDP expected unrevised at +2.1% — Today’s Q4 GDP report is expected to be unrevised at +2.1% (q/q annualized). Q3 personal consumption is expected to be revised slightly lower to +1.7% from +1.8%. U.S. GDP was supported in Q4 by a 1.20 point contribution from personal consumption and by a 1.48 point contribution from net exports, although net exports were artificially inflated by tariffs. Business investment in Q4 remained missing-in-action with a near-zero contribution to GDP in Q4.

Looking ahead, U.S. GDP in Q1 will be undercut by the coronavirus, which will hurt exports, business investment, and domestic consumption. The consensus is for Q1 GDP to ease to +1.5% from Q4’s +2.1%, but expectations are likely to worsen as the full extent of the damage is seen in China and as domestic fears of the virus flare-up in the U.S.

7-year T-note auction — The Treasury today will conclude this week’s $131 billion T-note package by selling $32 billion of 7-year T-notes. The benchmark 7-year T-note yield on Wednesday fell to a new 3-1/2 year low of 1.22% and closed the day -1 bp at 1.26%.

The 12-auction averages for the 7-year are as follows: 2.42 bid cover ratio, $15 million in non-competitive bids, 4.7 bp tail to the median yield, 38.8 bp tail to the low yield, and 66% taken at the high yield. The 7-year T-note is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 60.1% of the last twelve 7-year T-note auctions, which exactly matches the median of 60.1% for all recent coupon auctions.