- Weekly global market focus

- U.S. Treasury today will outline quarterly borrowing needs after Fitch puts U.S. debt rating on negative watch

- U.S. new Covid cases stabilize at a high level

- Negotiations continue on new pandemic bill with little progress thus far

- Q2 earnings season remains busy with SPX earnings growth expected at -34%

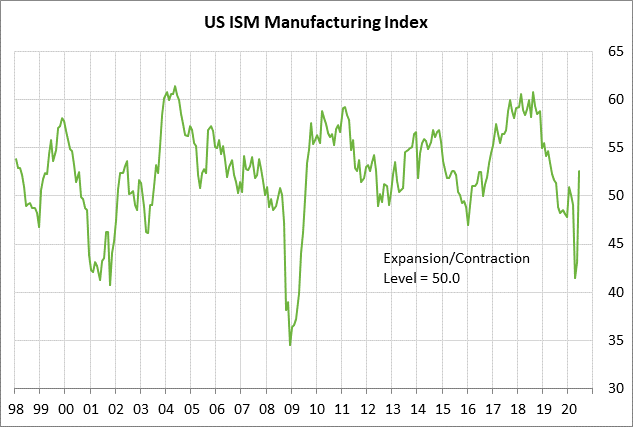

Weekly global market focus — The U.S. markets this week will focus on (1) progress in Washington on the pandemic stimulus bill, (2) U.S./China tensions with President Trump saying he plans to ban TikTok in the U.S., (3) the Treasury’s borrowing requirements with its announcements today and Wednesday, (4) this week’s busy Q2 earnings schedule, (5) today’s July ISM U.S. manufacturing index (expected +0.9 to 53.5 after June’s +9.5 to 52.6), and (6) Friday’s July unemployment report (payrolls expected +1.6 million and unemployment rate expected -0.6 to 10.5%).

In Europe, the focus will be on the Bank of England’s meeting on Thursday, which is expected to produce an unchanged policy. Friday’s German June industrial production report is expected to rise by +7.2% m/m, extending May’s +7.8% m/m upward rebound.

In Asia, the focus will remain mainly on U.S./China tensions with the U.S. expected to launch a broadside against some Chinese software apps, starting with TikTok. China’s July Caixin services PMI on Tuesday night is expected to fall by -0.5 points to 57.9 after June’s +3.4 point rise to 58.4. Chinese July exports on Thursday night are expected to fall by -0.9% y/y after June’s +0.5% y/y increase.

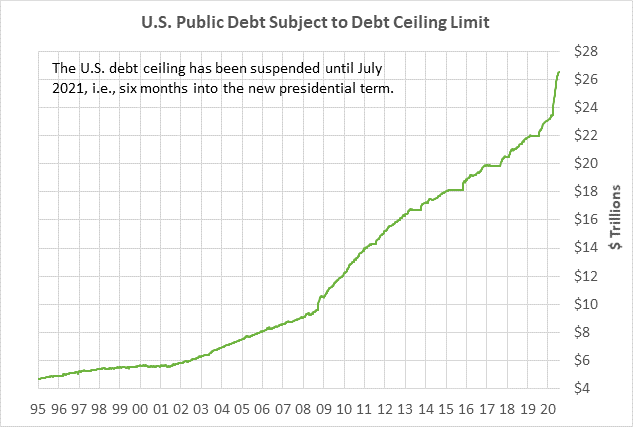

U.S. Treasury today will outline quarterly borrowing needs after Fitch puts U.S. debt rating on negative watch — The Treasury today will announce its short-term borrowing needs and on Wednesday will then announce the details of its planned auctions for Q3. The Treasury is expected to announce up to $2.5 trillion of T-bills and a record issuance of coupons.

Meanwhile, Fitch after last Friday’s market close put the U.S. debt rating on negative watch, citing a “deterioration in U.S. public finances and the absence of a credible fiscal consolidating plan.” Fitch left its U.S. country ranking at AAA for now. Fitch said that it expects general U.S. government debt to exceed 130% of GDP by 2021, which would clearly be in the red zone.

U.S. new Covid cases stabilize at a high level — The 5-day average of new U.S. Covid cases was near 65,000 this weekend, mildly below the record of 69,451 cases posted in mid-July, according to Johns Hopkins. The 5-day average of new Covid cases has been fluctuating between 60,000 and 70,000 for the past several weeks, suggesting that recent restrictions in hard-hit states have been successful in preventing infection rates from rising any higher. However, the U.S. has yet to see any dramatic fall in new Covid cases that would indicate the pandemic is being brought under control.

Globally, India’s new-infection level is steadily climbing and may soon challenge America’s first-place position. Brazil saw a recent dip but its new infection levels are back up near their recent high. Other countries in the world are seeing sporadic outbreaks that are leading to new restrictions. Still, none of those countries is seeing any major upside breakout in the total country infection levels.

Negotiations continue on new pandemic bill with little progress thus far — The federal unemployment bonus of $600 per week expired last Friday for some 30 million people, which will reduce U.S. consumer income by about $18 billion per week and put a big dent in Q3 U.S. personal income and spending. Meanwhile, the federal protection against eviction expired on July 25, which means more people will now be getting evicted from rental properties financed by federally-guaranteed loans.

Meanwhile, Republicans and Democrats remain far apart on a pandemic deal that would extend the unemployment bonus at some level and also extend the eviction shield. There was a 3-hour Mnuchin-Meadows-Pelosi-Schumer meeting on Saturday, and their staff then met on Sunday. That group is due to convene today for another round of talks.

White House chief of staff Meadows on Sunday said, “We still have a long ways to go. I’m not optimistic that there will be a solution in the very near term.” Democrats are pushing for an overall deal and are refusing to consider the Republicans’ proposal for a 1-week extension. The Senate is scheduled to leave for its August recess this Friday. The House is already on recess, but Speaker Pelosi said she will call the House back to session if there is a pandemic bill to pass.

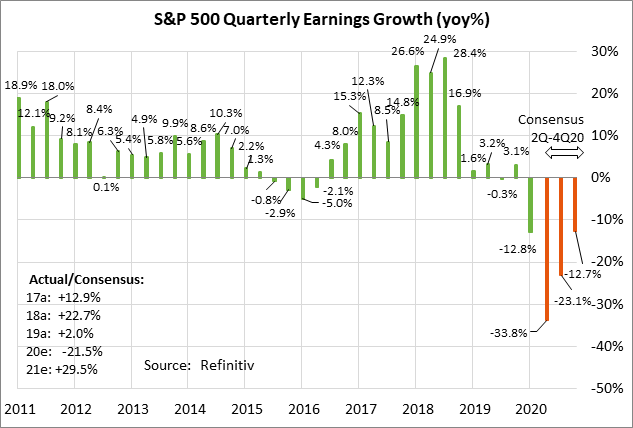

Q2 earnings season remains busy with SPX earnings growth expected at -34% — Last week was the peak week for Q2 earnings, but this week will still be very busy with 132 of the S&P 500 companies reporting. Notable reports this week include Berkshire Hathaway on Monday; Walt Disney and Allstate on Tuesday; Regeneron, Humana, and Marathon Oil on Wednesday; and Norwegian Cruise Line Holdings on Thursday.

The consensus is for a plunge of -33.8% y/y in S&P 500 Q2 earnings (according to Refinitiv) due to the widespread economic shutdowns seen across the United States and the world. Looking ahead, the consensus is for earnings to fall by -23.1% y/y in Q3 and -12.7% in Q4, then recovering sharply in early 2021. On a calendar year basis, the consensus is for SPX earnings to fall -21.5% in 2020 and then recover by +29.5% in 2021.

Sector earnings in Q2 have been highly variable depending on how hard a particular sector was hit by the pandemic. The earnings consensus by sector, according to Refinitive, is ranked as follows: Energy -170.2%, Industrials -85.6%, Consumer Discretionary -77.0%, Financials -43.6%, Materials -31.3%, Communication Services -22.6%, Real Estate -15.0%, Consumer Staples -8.9%, Health Care +1.2%, Info Technology +1.4%, and Utilities +2.7%.