- Weekly global market focus

- Stock market is shaken by global spread of coronavirus

- Chinese officials promise more stimulus as economy crawls back from shutdown

- Q4 earnings season winds down

Weekly global market focus — The U.S. markets this week will focus on (1) the extent to which the coronavirus is spreading outside China, (2) the tail end of Q4 earnings season with reports from 41 of the S&P 500 companies, (3) the Treasury’s sale of $131 billion of T-notes, (4) politics with this coming Saturday’s (Feb 29) South Carolina Democratic primary and next week’s Super Tuesday primaries in 14 states (Mar 3), and (5) a busy U.S. economic calendar.

Europe will focus on the coronavirus and a busy economic calendar. US/EU trade could be in the news this week after the digital tax was discussed at this past weekend’s G-20 meeting, and as the EU tries to get trade talks on track with the U.S.

Asia will focus on the coronavirus and the extent to which the Chinese economy is revving back up to capacity. The markets will assess the extent of the damage to Chinese business confidence with Chinese PMI reports due this Friday and Sunday. The consensus is for Friday’s Feb Chinese national manufacturing PMI to fall by -2.6 points to 47.4 and for the non-manufacturing PMI to fall by -4.1 to 50.0.

Stock market is shaken by global spread of coronavirus — The S&P 500 index last Friday fell sharply by -1.05% and the Nasdaq 100 index fell by -1.88% on concern about the spread of the coronavirus outside China. There are new concerns as pockets of the virus are popping up in a wide range of countries such as Japan, South Korea, Italy, and even Iran. Some of the infections have no known connection to China, suggesting that the virus is gaining local platforms for transmission.

The cases of the virus in the U.S. have all been traceable to overseas travel. However, the markets will get much more concerned about the impact of the virus on the U.S. if cases of community transmission start to emerge, which could lead to quarantines and business shutdowns in the U.S.

Fed officials are so far still expressing confidence about the U.S. economy and foresee a limited impact from the coronavirus. However, government officials naturally try to be optimistic and try not to foster a contagion of fear.

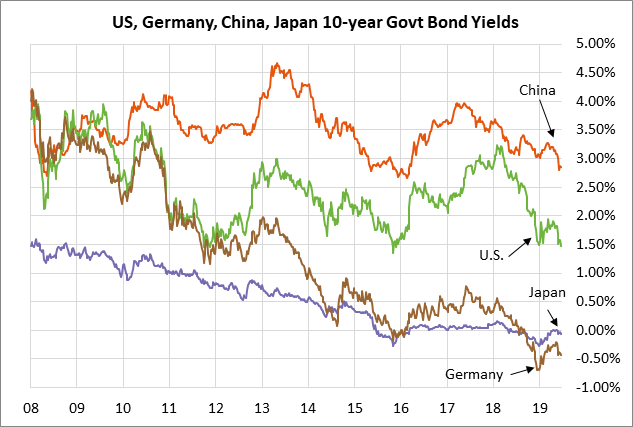

The markets last week boosted the estimate of Fed easing by year-end by 9 bp to 47.5 bp from 38.5 bp in the previous week, according to the Dec 2020 federal funds futures contract. That is equivalent to 1.9 rate cuts in 2020. The Fed, by contrast, is so far sticking with its Fed-dot forecast that no more rate cuts will be necessary and that one rate hike is likely in 2021 and a second rate hike in 2022.

Chinese officials promise more stimulus as economy crawls back from shutdown — The Chinese economy is struggling to get back on its feet after the partial shutdown seen over the past four weeks. The Chinese economy last week improved to running at 50-60% of its normal capacity, according to Bloomberg Economics, up from 40-50% a week earlier and a near shutdown in the two previous weeks during the extended Lunar New Year holiday.

Companies are expected to resume operations faster this week now that the 2-week quarantine period is over from the extended 2-week Lunar New Year holiday. That will allow more employees to travel and get back to work.

The extent of the damage was illustrated by last week’s news that Chinese domestic car sales in the first half of February plunged by 92%. The Chinese shutdown is having a substantial impact for some companies outside China from disruptions in supply chains and canceled product orders by Chinese companies.

Chinese officials last Friday promised more stimulus as the Chinese economy struggles to get back on its feet. Chinese officials, after a Politburo meeting last Friday chaired by President Xi, said that fiscal policy will be more proactive and construction projects will be accelerated. Meanwhile, the People’s Bank of China Deputy Governor Liu Guoqiang issued a separate statement last Friday saying that the central bank will free up more bank reserves to boost lending and will cut benchmark rates at the appropriate time.

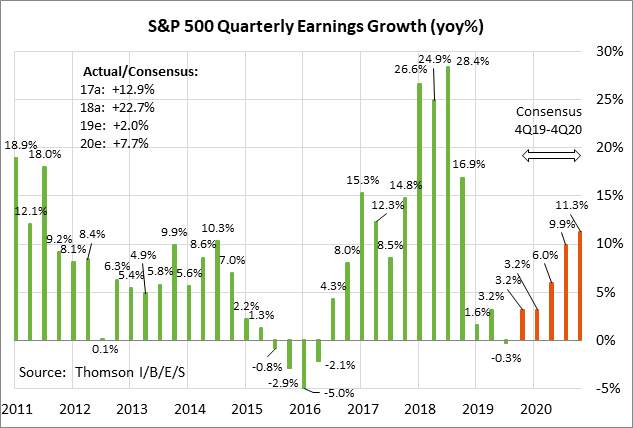

Q4 earnings season winds down — Q4 earnings season is winding down with 41 of the S&P 500 companies reporting earnings this week. Notable reports include HP and Intuit on Monday; Home Depot, Macy’s and Salesforce.com on Tuesday; Lowe’s, TJX, and L Brands on Wednesday; and Best Buy, Monster Beverage, and Occidental Petroleum on Thursday.

The consensus is for Q4 SPX earnings growth of +3.2% (6.1% ex-energy), which is substantially better than expectations of -0.3% as of January 1, according to Refinitiv. That would follow the weak 2019 quarterly SPX earnings growth rates of +1.6% in Q1, +3.2% in Q2, and -0.3% in Q3. Looking ahead, the consensus is for SPX earnings growth of +3.2% in Q1-2020, +6.0% in Q2, +9.9% in Q3, and +11.3% in Q4. The consensus is for 2019 calendar-year earnings growth of only +2.0% as earnings growth flattened out after the extraordinary growth rate of +23% in 2018 caused mainly by the massive 2018 corporate tax cut. The market consensus is for earnings growth in 2020 to improve to +7.7% y/y, although that 2020 earnings estimate has been steadily falling from 9.7% as of January 1.

Of the 437 S&P 500 companies that have reported thus far, 70.5% have reported above-consensus earnings, which is better than the long-term average of 64.9% but below the 4-quarter average of 73.5%, according to Refinitiv. Of the reporting S&P 500 companies, 64.7% have beaten their revenue consensus, which is better than the long-term average of 60.2% and the 4-quarter average of 57.8%, also according to Refinitiv.