- Time is winding down for CR and stimulus bill

- U.S. consumer sentiment expected to edge higher but remain generally weakÂ

- U.S. leading indicators expected to increase but remain well below pre-pandemic levels

- U.S. current account deficit expected to explode due to pandemic shutdowns

Time is winding down for CR and stimulus bill — Washington is quickly running out of time to get things done. Congress must pass a continuing resolution (CR) within the next 1-1/2 weeks to avoid a federal government shutdown on Oct 1.

Time is also running out for a pandemic relief bill since the Senate is trying to recess by late next week so that Senators who are up for reelection can hit the campaign trail.

The Hill reported yesterday that House might put a CR on the floor as early as today and vote on the bill next week. If the House moves quickly and votes by the middle of next week, then the Senate could perhaps vote on the CR by late next week, thus wrapping up their business and allowing them to go on recess.

However, House Democrats and Senate Republicans have not yet agreed on how long a CR will last. Senate Republicans want the bill to last until December, thus giving the current Republican Senate the chance to set spending for the remainder of the fiscal year. However, some Democrats want a longer CR that lasts into early 2021 after the inauguration to avoid a knock-down, drag-out fight in December during the lame-duck session.

In any case, the differences are likely to be ironed out fairly quickly because the general view is that no one in Washington wants to be blamed for a U.S. government shutdown so close to the November 3 election.

There was some possible movement this week on the pandemic relief bill when President Trump said that he “agreed with a lot” of the $1.5 trillion pandemic bill released this week by the bipartisan Problem Solvers group in the House. That suggested that Mr. Trump was raising his offer to as much as $1.5 trillion from the previous White House offer of $1 trillion. However, Speaker Pelosi rejected the Problem Solvers’ $1.5 trillion plan and said she was sticking to her $2.2 trillion demand.

Senate Republicans rejected the idea of going as high as $1.5 trillion. However, Senate Majority Leader McConnell, if he were to be sufficiently pressured by President Trump, could probably get a $1.5 trillion pandemic bill through the Senate with mostly Democratic votes.

Despite this week’s developments, the odds for a pandemic relief bill appear slim. If there is no deal by October 1, then most observers believe that any further consideration of a bill will not happen until after the Nov 3 election.

Yesterday’s sharp sell-off in the U.S. stock market was attributed in part to concern that the economic recovery is slowing as stimulus measures dry up. Part of that concern was sparked by Fed Chair Powell’s comment at his post-meeting press conference on Wednesday that he is unsure if the faster-than-expected economic recovery will continue.

Also, yesterday’s U.S. economic data was weaker than expected. Weekly initial unemployment claims fell by only -33,000 to 860,000, showing a weaker labor market than expectations for a decline to 850,000. Also, Aug housing starts fell -5.1% to 1.416 million, weaker than expectations of 1.488 million. In addition, Aug building permits unexpectedly fell -0.9% to 1.470 million, weaker than expectations for an increase to 1.512 million.

The stock market is also worried about the continued stalemate in Washington over a new pandemic relief bill since virtually everyone agrees that the economy needs another shot of stimulus of some size.

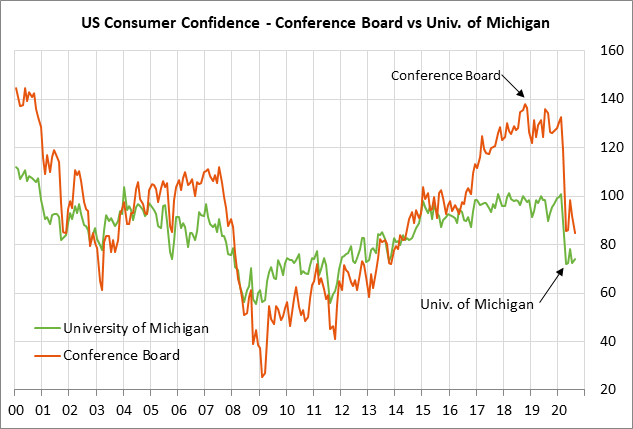

U.S. consumer sentiment expected to edge higher but remain generally weak — The consensus is for today’s preliminary-Sep University of Michigan U.S. consumer sentiment index to show a small +0.9 point increase to 75.0, adding to Aug’s +1.6 point increase to 74.1.

U.S. consumer sentiment has failed to show much of a recovery from the plunge seen during the spring pandemic shutdowns. The consumer sentiment index of 74.1 seen in August was only +2.3 points above April’s 8-3/4 year low. U.S. consumer sentiment has stabilized due to the partial rebound in the economy. However, consumers remain nervous with (1) unemployment still at very high levels, (2) previous stimulus measures wearing off and with Washington deadlocked over another pandemic relief bill, and (3) uncertainty about the upcoming election that may have a chaotic outcome.

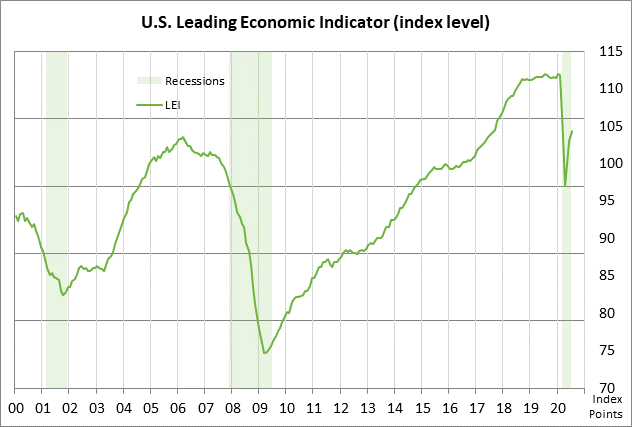

U.S. leading indicators expected to increase but remain well below pre-pandemic levels — Today’s U.S. leading indicators report is expected to show an increase of +1.3% m/m, adding to July’s increase of +1.4% m/m. The LEI has so far recovered only about half of the plunge seen this past spring when the U.S. saw its worst recession in post-war history.

The LEI is still down -6.8% on a year-on-year basis, indicating that the U.S. economy has a long way to go for a recovery. The consensus is for the U.S. economy in 2020 to show a GDP decline of -4.5%, and then recover by only +3.7% in 2021 and +2.9% in 2022.

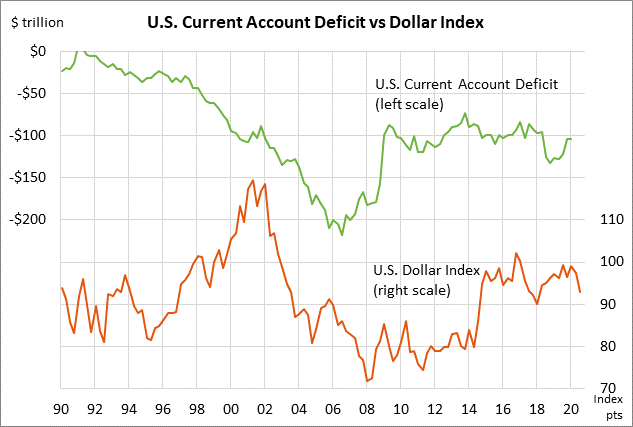

U.S. current account deficit expected to explode due to pandemic shutdowns — The consensus is for today’s Q2 current account deficit to explode to -$160.0 billion from -$104.2 billion in Q1, which would be the largest deficit since 2008 during the Great Recession. The sharp rise in the deficit is expected to be the result of exports plunging much faster than imports during the pandemic shutdowns. The sharp rise in the Q3 current account deficit is highly negative for the GDP figures.