- President Trump threatens executive action late today or Saturday if there is no pandemic deal

- July U.S. payroll report expected to show slower improvement of the U.S. labor market

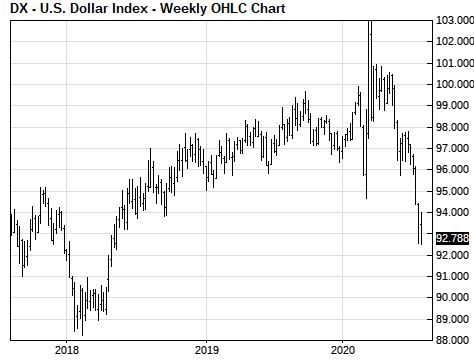

- Dollar index edges to new 2-year low as bearish factors dominate

President Trump threatens executive action late today or Saturday if there is no pandemic deal — President Trump on Thursday said he expects to sign executive orders late Friday or Saturday with pandemic relief measures if there is no agreement by Republicans and Democrats on a pandemic bill. Mr. Trump said he would sign an order to reinstate the renter eviction shield, which Speaker Pelosi said she would welcome.

Mr. Trump also said he would sign orders suspending the payroll tax, extending student loan forbearance, and reinstating the unemployment bonus. The White House says it can re-purpose unused money from one of the previous pandemic bills to send unemployment bonus money to the states. However, only Congress has the power of the purse. On the issue of President Trump unilaterally reinstating the unemployment bonus, Ms. Pelosi on Thursday said, “I don’t think they know what they’re talking about.”

Mr. Trump’s threat of executive action is clearly designed to push Democrats into a deal since the executive action could take away the Democrats’ key leverage points. Senate Republicans could then simply walk away from the rest of the deal, most of which they don’t support anyway.

Yet the more likely outcome is the well-trodden trail in Washington to a last-minute deal. Most politicians in Washington would like to get the pandemic bill over with and settle into their August vacations. After Labor Day, politicians will be in full campaign mode ahead of the November election. They will also be trying to prevent another government shutdown when the fiscal-year spending authority runs out on September 30.

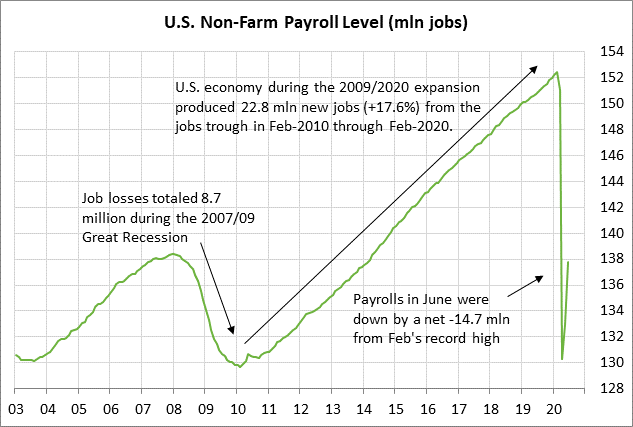

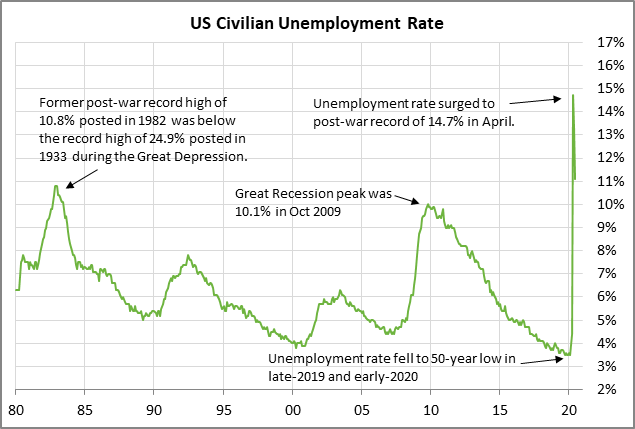

July U.S. payroll report expected to show slower improvement of the U.S. labor market — The consensus is for today’s July payroll report to show an increase of +1.5 million jobs, which would be a smaller gain than +4.8 million in June and +2.7 million in May.

The labor market is expected to show a smaller improvement in July because of the second Covid wave that began in mid-June. The second wave caused some businesses to shut back down, thus laying off their employees for a second time. The Covid resurgence also made clear that the pandemic will last much longer than earlier thought, forcing business managers to lay off more employees to batten down the hatches for a long road back to profitability. In addition, PPP money has largely run out, forcing businesses to lay off employees who were kept on the payroll only because of the temporary PPP money.

If today’s payroll report is in line with market expectations of +1.5 million, then payrolls would have risen by +9 million from April’s trough, retracing about 40% of the 22.2 million job loss seen in March-April. Today’s expected rise in payrolls would still leave jobs down by 13.2 million jobs from February’s record high.

Wednesday’s ADP report of only +167,000 was disappointing and was much weaker than market expectations of +1.2 million. The ADP report did not bode well for today’s payroll report.

The consensus is for today’s July unemployment rate to fall by -0.6 points to 10.5%. Today’s expected unemployment rate of 10.5% would be down sharply by 4.2 points from April’s record high of 14.7% but would still be above the worst level of 10.0% seen during the Great Recession.

The U.S. unemployment rate was at a 50-year low of 3.5% as recently as February. The unemployment rate is not likely to fall back to that level for a matter of years.

Dollar index edges to new 2-year low as bearish factors dominate — The dollar index on Thursday edged to a new 2-year low and closed the day slightly lower by -0.09%. The dollar fell on Thursday as stocks rallied and reduced liquidity-demand for the dollar. The S&P 500 index on Thursday rallied to a new 5-1/2 month high and closed the day up +0.64%, while the Nasdaq 100 index rallied to a new record high and closed the day up +1.27%.

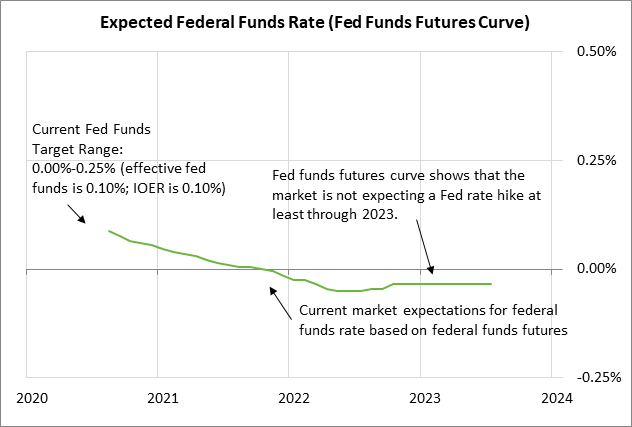

The dollar continues to see weakness due to the Fed’s extremely easy monetary policy, which has successfully tamped down systemic financial risks and reduced emergency demand for the dollar. The Fed has cut its funds-rate target rate to near zero and the markets are expecting the funds rate to remain near zero, or go even lower, for at least the next two years.

The Fed is also continuing to pump reserves into the banking system at a furious pace with its QE program of $120 billion per month. The Fed’s balance sheet has risen by $2.8 trillion (+67%) to a record $6.95 trillion from February’s pre-pandemic level. The Fed’s balance sheet has exploded to 32.2% of U.S. GDP from 19.3% before the pandemic.

The dollar is also seeing weakness from political uncertainty ahead of the November presidential and Congressional elections. Foreign investors are nervous about what could be a chaotic election amidst the pandemic.

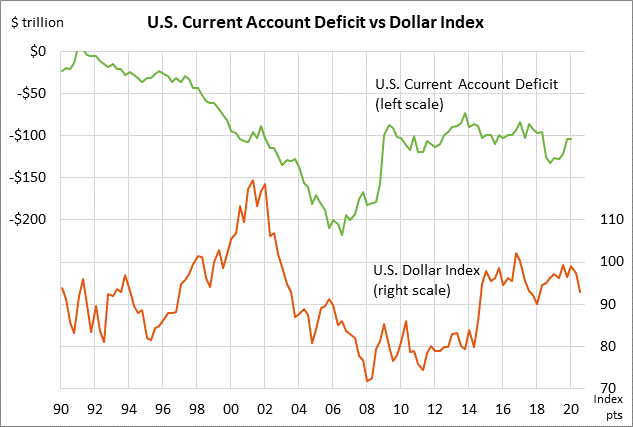

The dollar also continues to be undercut by the so-called Twin Deficits. The U.S. has had a large and persistent current account deficit totaling $458 billion over the last four quarters. That means that a net $1.3 billion worth of dollars are flowing out of the U.S. every calendar day. The explosion of the U.S. federal government’s budget deficit is also bearish for the dollar because that deficit needs to be covered in part by importing foreign capital, which creates a larger capital account surplus and by definition a larger current account deficit.