- Pelosi expects House to pass rescue bill today

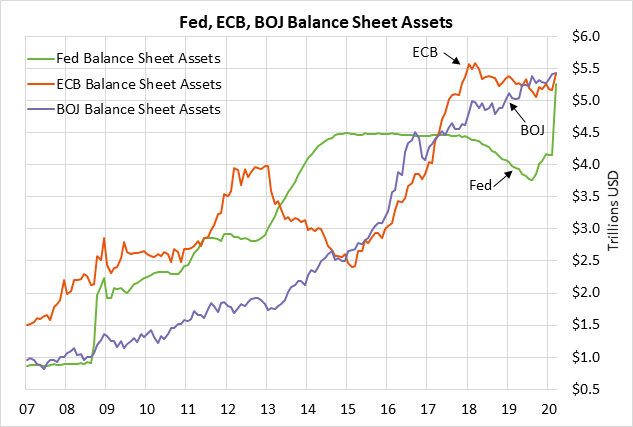

- Fed becomes an even bigger super-bank with another $4.5 trillion of direct-lending firepower

- ECB throws off the shackles to support troubled countries such as Italy and Spain

Pelosi expects House to pass rescue bill today — House Speaker Pelosi on Thursday said that she expects the House today to approve the $2 trillion rescue bill, sending it to President Trump for his signature. However, the House today must pass the bill by unanimous voice consent since the chamber is on recess. If a single House member objects to a unanimous voice consent, then Ms. Pelosi will have to call all House members back to Washington to vote, which would delay the vote by 1-2 days. The Senate on Wednesday night approved the bill by a unanimous 96-0 vote.

The breakdown of where the $2 trillion of rescue funds will go, according to Bloomberg, is as follows: (1) $532 billion for big business and local government loans, (2) $377 billion for small business loans and grants, (3) $290 billion for direct payments to families, (4) $290 billion in tax cuts, (5) $260 billion in expanded unemployment insurance, (6) $150 billion for state and local stimulus funds, and (7) $385 billion for a variety of other items including hospitals, FEMA, education, vaccines, and infrastructure.

Speaker Pelosi on Thursday said that she sees the next virus legislative package as focusing on recovery efforts, including job creation and infrastructure. Washington is currently focused on dealing with the immediate economic blow to the economy and the financial markets, but will soon turn to programs designed to help the millions of unemployed persons, helping small business, and getting the country back to work.

Considering that millions of people have already been laid off from their jobs, Washington will have to think big about how to get the nation back to work. Washington may have to dust off the history books and see what lessons can be learned from the Works Progress Administration (WPA), which was the employment and infrastructure program run by the U.S. government in the 1930s during the Depression.

Many people will not be able to return to their previous jobs because many businesses will be forced to close permanently because of the financial stress from the pandemic. In addition, the U.S. is likely to face a long slog in getting the pandemic contained since the number of U.S. coronavirus cases is steadily rising. Just yesterday, the U.S. overtook China with the most cases of coronavirus. The U.S. has 81,285 reported cases of coronavirus and 1,177 deaths. As testing increases, the number of identified coronavirus cases could skyrocket, showing that the U.S. has a much bigger problem than it thought. The longer it takes to get the pandemic under control, the longer it will take for the travel, entertainment, hotel, and restaurant industries to come back to life.

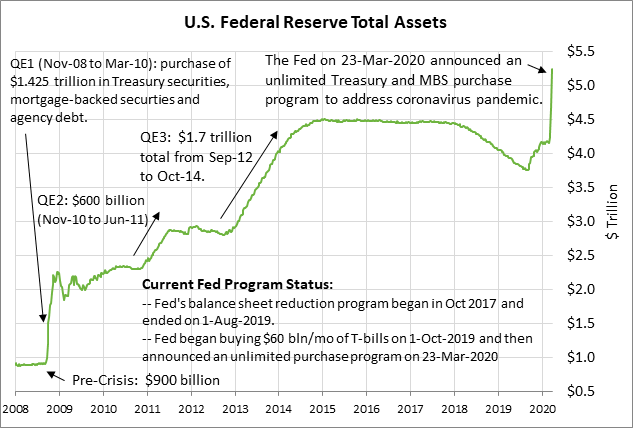

Fed becomes an even bigger super-bank with another $4.5 trillion of direct-lending firepower — The Fed has already embarked on a whole new method of conducting monetary policy, i.e., delivering loans directly to securities markets, financial firms such as government securities dealers, mortgage banks and servicing firms, and private businesses. Also, the Fed is soon expected to have in place its new “Main Street Business Lending Program,” which in conjunction with the Small Business Administration (SBA) will provide loans to small and medium sized businesses.

The Fed’s traditional method of executing monetary policy is to deal only with banks and control lending in the economy by managing bank reserves and short-term lending rates. However, the Fed has now broken out of that box and is playing the role of the banks themselves, i.e., lending money directly to a variety of entities where the banks cannot or will not lend. The Fed has essentially become an all-powerful “super-bank” with nearly unlimited lending power.

The Fed has already started acting as a super-bank under its current authority and with the backstop of the Treasury’s Exchange Stabilization Fund (ESF). The ESF provides a 10% equity backstop for the Fed’s special lending programs and takes the first 10% of any losses that might be incurred, thus insulating the Fed from risk-taking.

However, the Fed can multiply the firepower of the ESF by ten-fold since the Treasury’s ESF provides the first $1 and the Fed provides the next $9 of lending. The Fed can therefore leverage the ESF on a 10-to-1 basis to an enormous size.

The ESF at the end of February 2020 held $94 billion, which implied Fed lending power of about $940 billion (i.e., $94 billion times the Fed’s 10-1 leverage). However, the $2 trillion rescue bill that the House is expected to approve today, gives the ESF another $454 billion. That means that if the House passes the bill today, the Fed by next week will have another $4.5 trillion of lending available to provide to whatever parties are deemed in need of funds. The Fed is clearly not out of firepower — the Fed is just getting going.

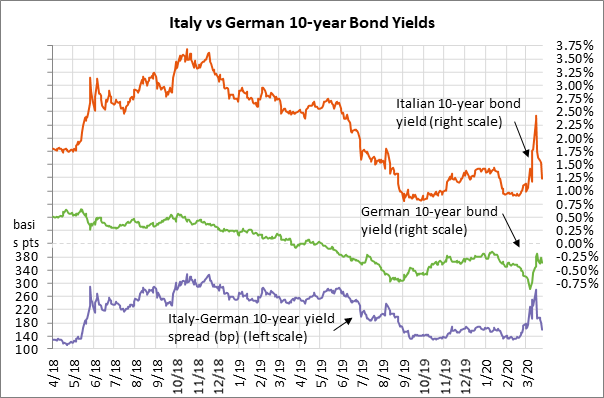

ECB throws off the shackles to support troubled countries such as Italy and Spain — The ECB on Thursday announced that it will no longer have the previous self-imposed constraints on the bonds that it buys under its new 750 billion euro bond purchase program. Previously, the ECB limited itself to buying a maximum of one-third of a country’s bonds. The ECB’s new buying program began yesterday.

The ECB clearly intends to defend the bonds of countries hard-hit by the virus such as Italy and Spain to prevent a financial crisis from developing in those countries. The spread of the 10-year Italian bond yield over the German bond yield plunged by -21 bp on Thursday to 159 bp and has now reversed most of the surge seen in early March to the mid-March 10-month high of 279 bp.