- Pelosi-Mnuchin try to reach a pandemic stimulus bill by today

- Betting spread moves against President Trump by 8 points after Tuesday’s debate

- Unemployment claims expected to continue to decline but remain high

- PCE deflator expected to edge higher

- U.S. ISM manufacturing index expected to reach new 1-3/3 year high

Pelosi-Mnuchin try to reach a pandemic stimulus bill by today — House Speaker Pelosi and Treasury Secretary Mnuchin Wednesday held a 90-minute meeting that made progress but broke up without an agreement. After leaving the meeting, Mr. Mnuchin said that he and Ms. Pelosi “made a lot of progress over the last few days.” For her part, Ms. Pelosi said, “We found areas where we are seeking further clarification. Our conversations will continue.”

Mr. Mnuchin then met with Senate Majority Leader McConnell later Wednesday afternoon, presumably to see if Mr. McConnell would be on board with whatever compromise Pelosi-Mnuchin are discussing. Senate Republicans have refused to go above about $1 trillion in spending, but they appear to be bending as the election draws closer.

Democratic Caucus leader Hakeem Jeffries (D-NY) earlier on Wednesday said that Mr. Mnuchin’s counteroffer was based on the $1.5 trillion stimulus bill that was recently released by the bipartisan House “Problem Solvers” group. The size of their bill can go up to $2 trillion if the pandemic persists. Mr. Jeffries said that the two sides were closer to a deal “than we have ever been.”

The House yesterday delayed their vote on Democrat’s $2.2 trillion stimulus bill in order to give the Pelosi-Mnuchin talks another day to produce an agreement. If there is no agreement today, then the House is expected to pass that bill before leaving Washington on Friday for a recess that will last until after the November 3 election.

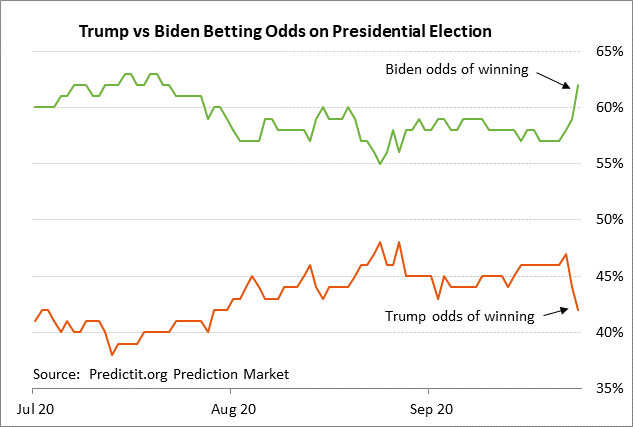

Betting spread moves against President Trump by 8 points after Tuesday’s debate — The betting odds at PredictIt.org, for whatever they are worth, moved against President Trump by a spread of 8 points after Tuesday’s Trump-Biden debate. The odds early Wednesday evening were 63% for a Biden win (up 5 points from 58% just before the debate) and 43% for a Trump win (down 3 points from 46% just before the debate).

The markets are watching the betting odds for a frame of reference, but are not relying heavily on the quality of the prediction. As everyone knows, the betting odds were very wrong for the Clinton-Trump match-up in 2016. The PredictIt.org odds just before that election were 82% in favor of a Clinton victory versus only 22% in favor of a Trump victory. However, the odds were a better predictor in the 2012 Obama-Romney matchup, with the odds just before that election at 66% for an Obama win versus 34% for a Romney win.

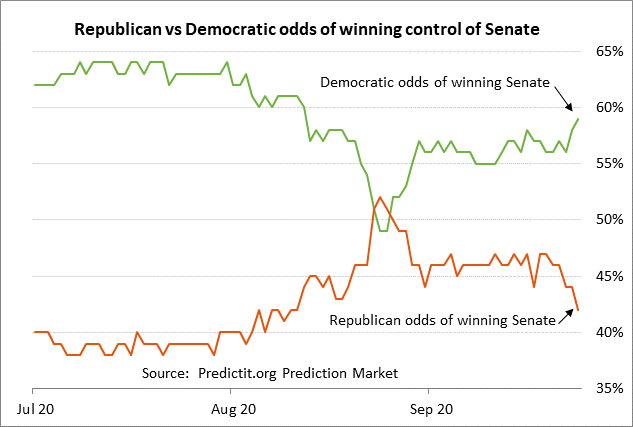

The betting odds on Wednesday for Democratic control of the Senate after November’s election improved by a spread of 3 points, with the odds late Wednesday at 59% for the Democrats (vs 58% before the debate) and at 42% for Republicans (vs 44% just before the debate). The betting odds for control of the House on Wednesday were little changed at 85% for the Democrats versus 18% for the Republicans.

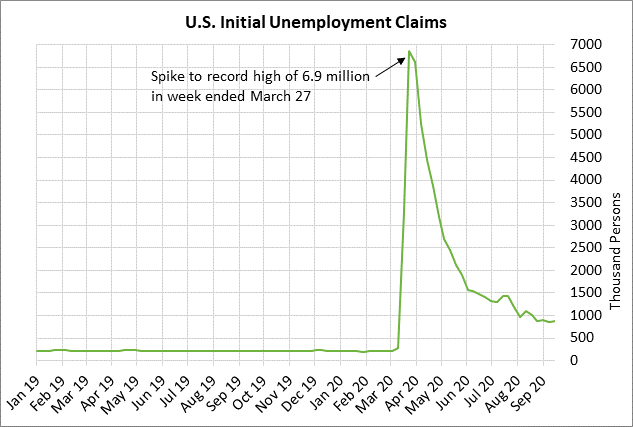

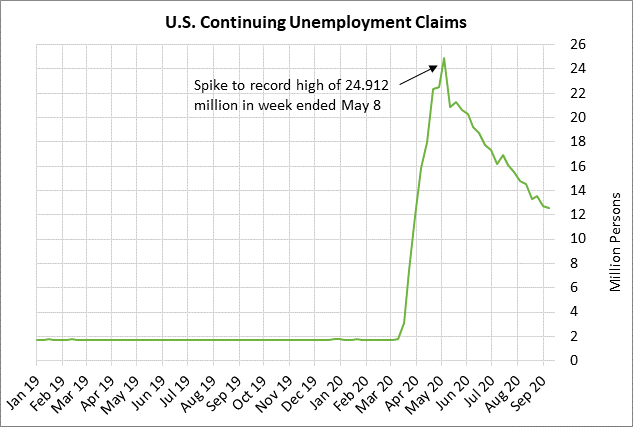

Unemployment claims expected to continue to decline but remain high — The consensus is for today’s weekly initial unemployment claims report to fall by -20,000 to 850,000 after last week’s small +4,000 increase to 870,000. Meanwhile, continuing claims are expected to fall -380,000 to 12.200 million, adding to last week’s -167,000 decline to 12.580 million.

Unemployment claims have been falling for the last five months but the level of claims remains high and indicates continued severe pain in the labor market. Initial claims are still 653,000 above the pre-pandemic level. Meanwhile, continuing claims are 10.881 million above the pre-pandemic level, indicating that nearly 11 million more people are out of work than before the pandemic.

There was some good news for the labor market on Wednesday with the Sep ADP report of +749,000, which showed a stronger labor market than expectations of +648,000. Wednesday’s ADP report lent support to the consensus for Friday’s Sep payroll report of +859,000, which would add to Aug’s increase of +1.371 million.

Meanwhile, Friday’s Sep unemployment rate is expected to fall by -0.2 points to 8.2%. However, that would still be more than double the pre-pandemic level of 3.5% and only 2 points below the worst level of +10.0% seen during the Great Recession.

PCE deflator expected to edge higher — The consensus is for today’s Aug PCE deflator to edge higher to +1.2% y/y from July’s +1.0% y/y, and for the Aug core PCE deflator to rise to +1.4% y/y from July’s +1.3% y/y.

Today’s expected rise in the PCE deflator, which is the Fed’s preferred inflation indicator, would be a step in the right direction for the Fed. However, the deflator will remain well below the Fed’s +2.0% inflation target. The Fed is not forecasting that the PCE deflator will match its 2.0% target until 2023, which means that a rate hike is not likely until at least 2023.

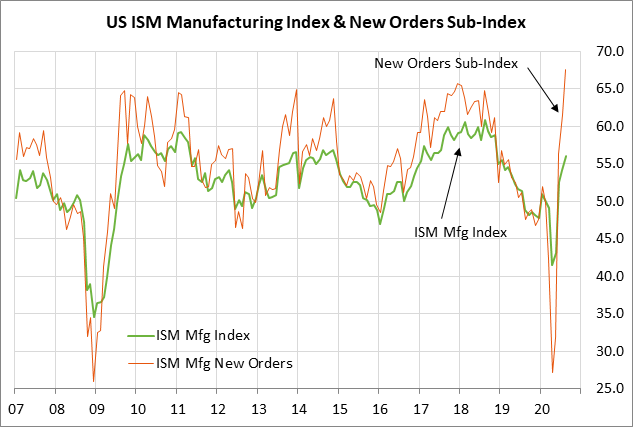

U.S. ISM manufacturing index expected to reach new 1-3/3 year high — Today’s ISM report is expected to show a continued improvement in manufacturing confidence. The consensus is for today’s Sep ISM manufacturing index to show a +0.3 point increase to 56.3, adding to Aug’s +1.8 point increase to a 1-3/4 year high of 56.0. The new orders sub-index is in even better shape, rising +6.1 points to 67.6 in August and illustrating that manufacturers are seeing their order pipelines fill back up. Expectations for an increase in today’s ISM report are based in part on recent news that the early-Sep Markit manufacturing PMI rose by +0.4 points to 53.5. The final-Sep Markit PMI index today is expected to be left unrevised.