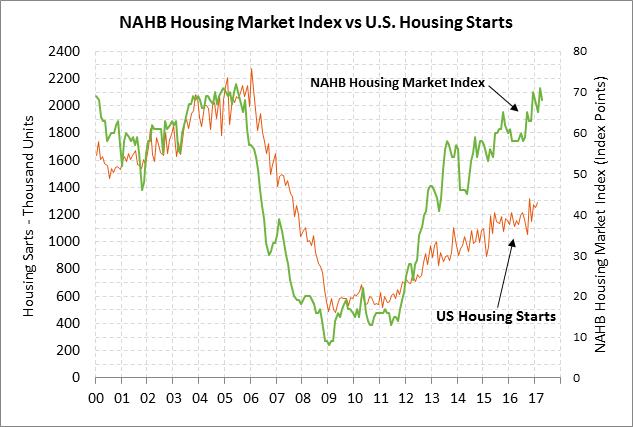

- U.S. housing starts remain in strong shape

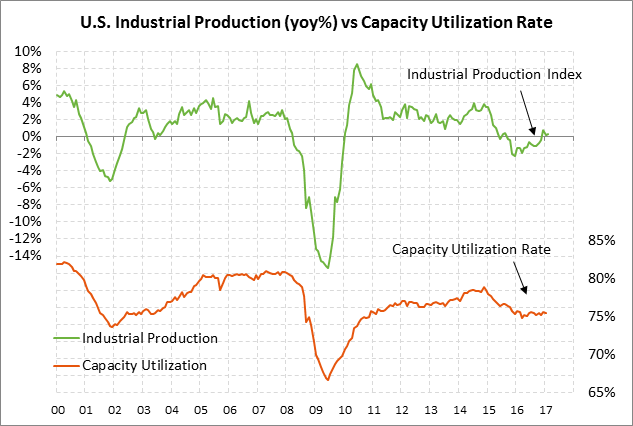

- U.S. industrial production expected to increase but could show weather-related volatility

- U.S. Q1 earnings growth expected to post 5-year high with help from energy rebound

U.S. housing starts remain in strong shape — The market consensus is for today’s March U.S. housing starts report to show a -3.0% decline to 1.250 million, thereby reversing Feb’s +3.0% increase to 1.288 million. Meanwhile, today’s Mar building permits report is expected to show a +2.8% increase to 1.250 million, recovering about half of Feb’s -6.0% decline to 1.216 million. The March housing market data may have been negatively impacted by winter storm Stella that hit the Northeastern U.S. in mid-March.

Aside from weather-related factors, U.S. housing starts in general remain in very strong shape at only -2.4% below the 9-1/2 year high of 1.320 million units posted in Oct 2016. U.S. home builder optimism continues to be very strong with the April NAHB housing market index of 68 hovering just -3 points below the 12-year high of 71 posted in March.

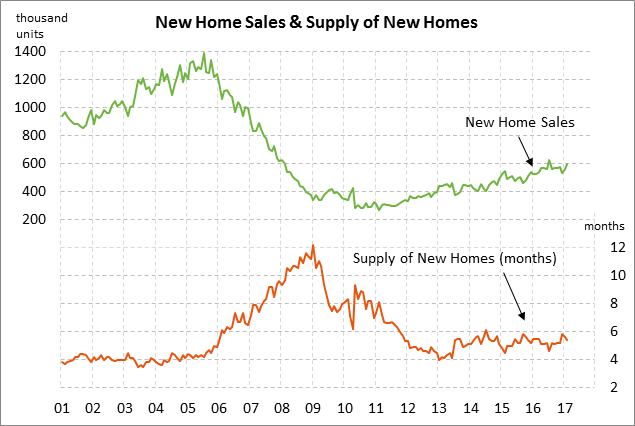

U.S. home builders are very optimistic about building homes due to (1) strong new home sales, (2) the mildly tight supply of new homes on the market, and (3) strong new home prices. New home sales started the year by rising sharply by +11.4% in Jan-Feb and are now only -4.8% below the 9-year high of 622,000 units posted in July 2016.

Home builders can also take heart from the decline in mortgage rates seen in the past month. After the election, the 30-year mortgage rate initially surged by +78 bp to a 3-year high of 4.32% in late December. However, the 30-year mortgage rate has since fallen by -24 bp to last week’s level of 4.08%, which is was +54 bp above the pre-election level.

U.S. industrial production expected to increase but could show weather-related volatility — The market consensus for today’s Mar industrial production report is for a solid increase of +0.4%. Industrial production is expected to recover in March from Feb’s weak report of unchanged since utility output likely increased in March due to the more seasonal winter weather.

For the manufacturing sector, the consensus is for March manufacturing production to show a small increase of +0.1% after Feb’s strong +0.5% gain. Manufacturing output in March likely corrected lower in part because of the bad weather in March that undercut the number of manufacturing hours worked.

The U.S. manufacturing sector is now getting a boost from stronger overseas growth and from the recovery in the petroleum sector. The dollar is still generally strong, but it has faded since January, giving exporters a little relief. U.S. manufacturing confidence remains in good shape with the March ISM manufacturing index at 57.2, which is only -0.5 points below the 2-1/2 year high of 57.7 posted in Feb.

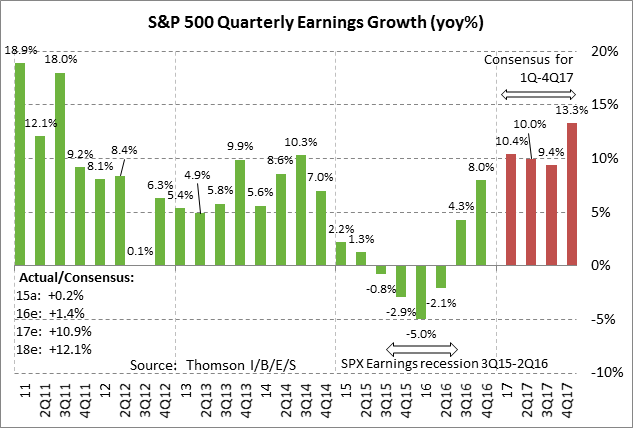

U.S. Q1 earnings growth expected to post 5-year high with help from energy rebound — The market consensus for Q1 earnings growth is +10.4% for the S&P 500 companies, according to surveys by Thomson I/B/E/S. That would be the strongest growth rate in over 5 years, i.e., since Q3-2011 when earnings were recovering sharply from the Great Recession.

U.S. companies just nine months ago emerged from the year-long earnings recession seen from 2H-2015 through 1H-2016. Earnings growth turned negative on (1) poor domestic and global growth, (2) the plunge in petroleum-sector earnings on OPEC’s oil-price war, and (3) the strong dollar.

Earnings growth finally turned positive again in the second half of 2016 and is now set to surge in 2017. The market consensus is for earnings growth of +10.9% in 2017 and +12.1% in 2018. That would follow barely positive growth of +0.2% in 2015 and +1.4% in 2016.

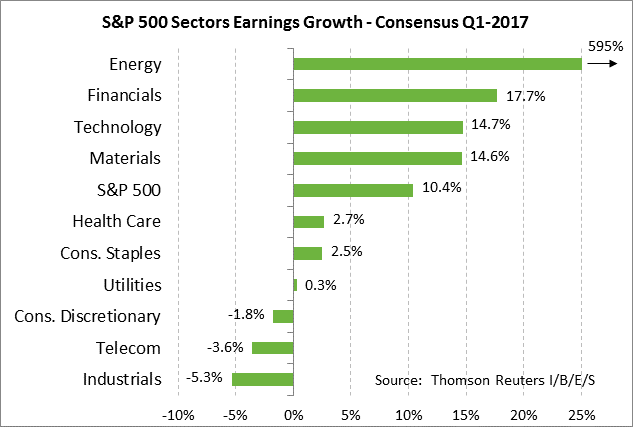

One caveat to the strong +10.4% consensus for Q1 earnings growth is that top-line growth is being artificially boosted to some extent by the sharp year-on-year recovery in petroleum earnings from last year’s recessionary levels. The energy sector is expected to show nearly 6-fold earnings growth in Q1. Excluding the energy sector, the S&P 500 index is expected to show a more modest, but still respectable, +6.5% gain.

The S&P 500 index rallied sharply by a total of +20.6% from July 2016 to the record high posted in March 2017. That rally has been driven mainly by the recovery in earnings that started in 2H-2016 and also by expectations for pro-growth policies from the Republicans’ sweep of the November’s election.

It remains an open question as to how much of the post-election rally was driven by the Republican agenda versus expectations for strong +10.9% earnings growth in 2017. The stock market has so far not lost much ground despite pessimism about the Republican agenda, suggesting that strong earnings continue to provide solid underlying support for stocks.

On a sector basis, there is a wide spread for Q1 earnings expectations. Aside from energy, earnings in Q1 are expected to be led by Financials (+17.7%), Technology (+14.7%), and Materials (+14.6%). Meanwhile, expectations are low for consumer companies with Consumer Staples expected to show earnings growth of +2.5% and Consumer Discretionary expected to show a decline of -1.8%. Health care is expected to show a modest gain of +2.7%. Declines are expected for Telecom (-3.6%), and Industrials (-5.3%).