- Near-term focus is on Thu/Fri U.S. economic data and North Korea

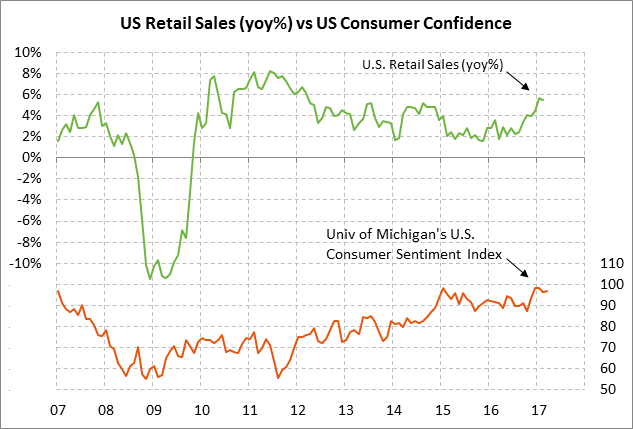

- Markets are waiting to see if U.S. consumer spending will improve

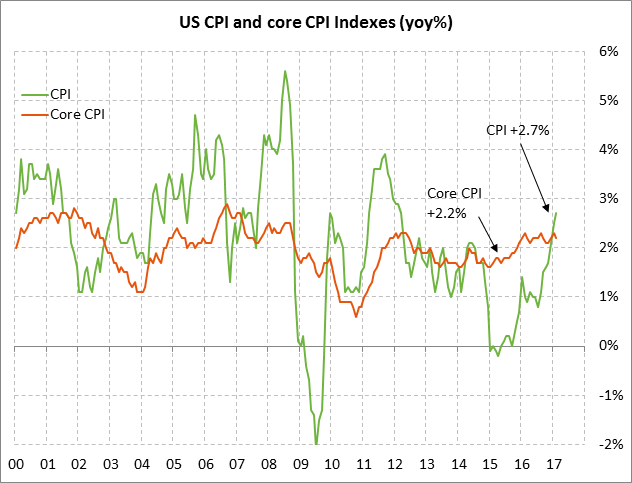

- U.S. CPI expected to remain strong

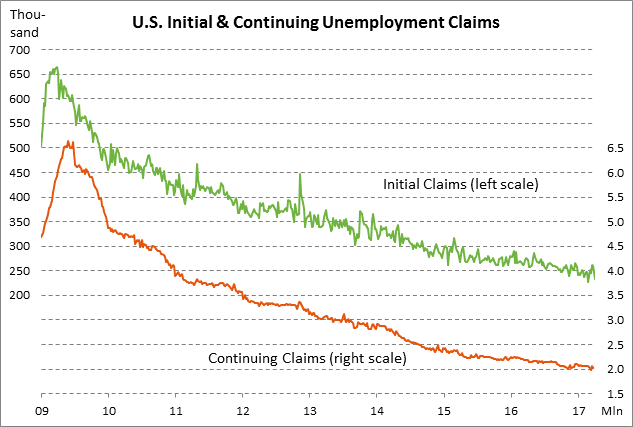

- Unemployment claims remain favorable

Near-term focus is on Thu/Fri U.S. economic data and North Korea — Today’s economic reports include (1) preliminary-April U.S. consumer sentiment index, (2) March PPI, and (3) weekly initial unemployment claims. The markets will be closed on Friday for the holiday, but the U.S. government is open. Friday’s U.S. economic reports include (1) March retail sales, (2) March CPI, and (3) Feb business inventories.

Meanwhile, foreign journalists in North Korea have been told to prepare for a “big and important” event on Thursday, according to Reuters. Saturday is North Korea’s most important national date since it the birth date of North Korea’s founder Kim Il Sung. North Korea has conducted weapons tests in the past on important national dates. A report emerged Wednesday evening that North Korea’s nuclear test site appears “primed and ready” to conduct a test, according to the US-Korea Institute at Johns Hopkins University. A nuclear bomb test or a test of a long-range intercontinental missile would be viewed as a direct challenge to President Trump, while a launch of short or medium range missiles would be a less aggressive move.

The U.S. Vinson aircraft carrier battle group, which President Trump on Wednesday called a “very powerful” armada, is due to arrive in the Korean vicinity next week. Mr. Trump also specifically noted America’s submarine capabilities, which seemed to be a reminder to North Korea that the U.S. already has submarines stationed not far off the coast of North Korea that could react if necessary. Of course, there are also some 28,500 American troops stationed in South Korea along with their weapons systems.

Markets are waiting to see if U.S. consumer spending will improve — The consumer spending data for Q1 has so far been disappointing. The Atlanta Fed’s Q1 GDP tracking estimate is currently penciling in only a +0.4 point contribution from personal spending, sharply below the more normal +2.0 point contribution seen in the second half of 2016. GDPNow last Friday cut its Q1 GDP estimate to a very weak +0.6% from +1.2%, although the report looks a little better at +1.3% after taking out the expected -0.7 point subtraction from inventories.

There are some special factors that hurt Q1 GDP that include bad weather and some late IRS refunds. There is also the ongoing debate about the extent to which the seasonal adjustment factors may have incorrectly depressed Q1 GDP growth in recent years. In the last five years, GDP growth has averaged only +1.4% in the first quarter of the year, which is -0.9 points less than the average of +2.3% seen in the other three quarters of the year.

The markets and Fed have become somewhat conditioned to expect weak GDP growth in the first quarter, so there isn’t much concern as yet about this year’s poor Q1 GDP growth. Furthermore, the NY Fed’s Nowcast Q1 GDP estimate is still much better at +2.8% since it takes into account not only the hard data tracked by GDPNow but also the stronger sentiment data seen recently. Still, the markets are nervous about the possibility that this year’s weak Q1 GDP growth could be due to something more fundamental than weather factors and residual seasonal effects.

On the consumer spending front, the market consensus is for Friday’s March retail sales to be weak at -0.2% m/m and +0.1% ex-autos, which would be even weaker than the Feb report of +0.1% and +0.2% ex-autos. The markets already know that vehicle sales were weak in March with the -5.4% m/m drop to a 2-year low of 16.53 million units from 17.47 million units in Feb. The drop in March vehicle sales was attributed in part to bad weather and consumers shunning sedans, but the weakness in auto sales may also have reflected the desire by consumers to simply spend less money.

On the consumer sentiment front, the market is expecting today’s preliminary-Apr University of Michigan U.S. consumer sentiment index to show a -0.4 point decline to 96.5, reversing part of March’s +0.6 point increase to 96.9. U.S. consumer sentiment remains very strong since the latest index level of 96.9 is only -1.6 points below the 13-year high of 98.5 posted in January.

U.S. CPI expected to remain strong — The market is expecting today’s March final-demand PPI report to converge toward the higher CPI figures. The March PPI is expected to rise to +2.4% from Feb’s +2.2% and the core PPI is expected to rise to +1.8% y/y from Feb’s +1.5%. Meanwhile, the market is expecting Friday’s March CPI report to edge lower to +2.6% y/y from Feb’s +2.7%, but the market is expecting the core CPI to edge slightly higher to +2.3% y/y from Feb’s +2.2%.

The Fed believes its job is virtually done on pushing inflation up to its +2.0% target level. The PCE deflator, the Fed’s preferred inflation measure, rose to a 5-year high of +2.1% y/y in Feb while core deflator matched the 4-3/4 year high of +1.8% y/y. Yet, market-based measures of inflation have recently been declining due to reduced optimism about the Republican agenda. The 10-year inflation expectations rate has fallen by -17 bp from January’s peak of 2.09% and is currently near a 4-month low at 1.92%.

Unemployment claims remain favorable — The consensus is for today’s weekly initial unemployment claims to show a +11,000 increase to 245,000 (after last week’s -25,000 to 234,000) and for continuing claims to show a -4,000 decline to 2.024 million (after last week’s -24,000 decline to 2.028 million). Both series remain in very strong shape. Initial claims are only +7,000 above the 44-year low of 227,000 posted in Feb and continuing claims are only +41,000 above the 17-year low of 1.987 million posted in early March.