- Market focus

- Fed expectations turn more hawkish on Dudley comments

- Geopolitics keep markets on edge

- Q1 earnings season kicks off

- 3-year T-note auction to yield near 1.53%

Market focus — The U.S. markets this week will focus on Fed policy and the extent of the current weakness being seen in the U.S. economy. The consensus for Friday’s March retail sales report is for another weak report of -0.1% and -0.1% ex-autos after Feb’s report of +0.1% and +0.2% ex-autos. The Atlanta Fed last Friday cut its tracking estimate for Q1 U.S. GDP to +0.6% from +1.2%, although the NY Fed’s Nowcasting Q1 tracking estimate is much stronger at +2.8% since the NY Fed takes into account sentiment data. Q1 earnings season begins this week. The Treasury on Mon-Wed will sell $56 billion of 3, 10 and 30-year securities.

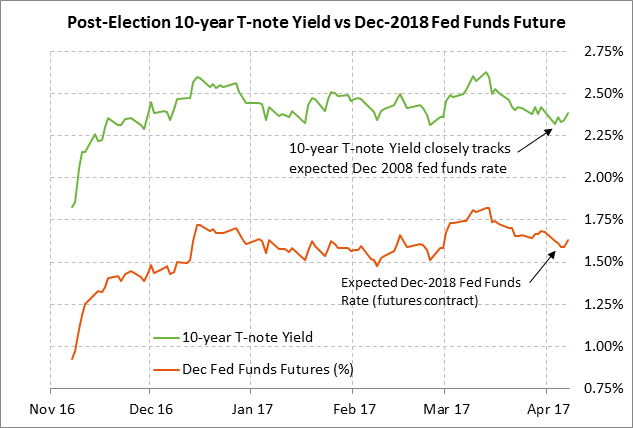

Fed expectations turn more hawkish on Dudley comments — Expectations for Fed policy last Friday turned a bit more hawkish due to comments by NY Fed President Dudley and reduced U.S. labor market slack after the -0.2 point decline in the March unemployment rate to a 10-year low of 4.5%. The federal funds futures curve on a yield basis last Friday rose by +1 bp for Dec 2017, +4 bp for Dec 2018, and +5 bp for Dec 2019. Friday’s weak March payroll report of +98,000 was largely ignored since it was caused in large part by the mid-March winter storm in the Northeastern U.S. March wage growth was in line with market expectations of +2.7% y/y.

The markets turned more hawkish on interest rates when NY Fed President William Dudley last Friday recalibrated his previous week’s comment that the Fed might pause in its rate-hike regime when it starts reducing its balance sheet. Mr. Dudley last Friday said, “Some people misconstrued what I said last week. I said a little pause. A pause is pretty short already, and I think a little pause is even shorter than that.” The markets in the past several weeks have cut expectations for Fed rate hikes mainly because of the idea that the Fed will go slower on rate hikes when it starts reducing its balance sheet.

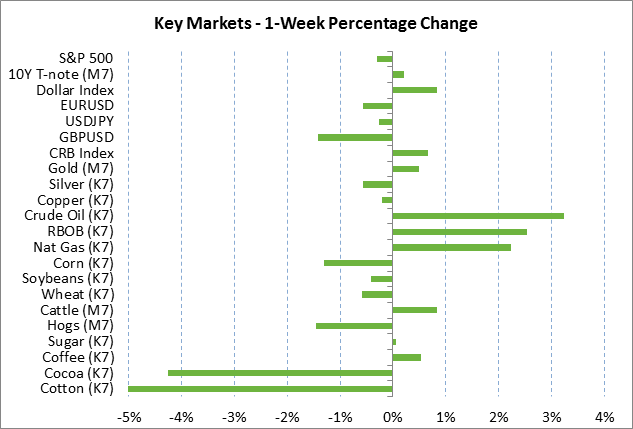

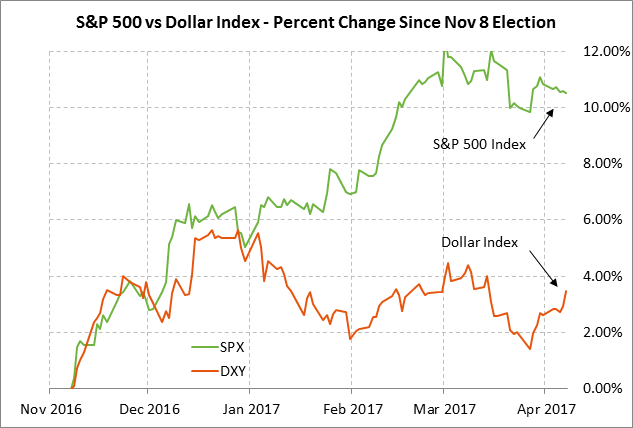

The 10-year T-note yield last Friday initially fell to a new 4-1/2 month low of 2.269% on the Syrian missile strikes and the weak payroll report, but then moved sharply higher to close the day up +4.1 bp at 2.38% due in large part to the Dudley comments. The S&P 500 index last week remained resilient despite the FOMC minutes raising the likelihood of balance sheet reduction “later this year” and the Syrian missile strike on Thursday evening. The S&P 500 index closed down -0.30% on the week. The dollar index last Friday rallied sharply on a boost from the Dudley comments and closed the week +0.83% at a 3-1/2 week high.

Geopolitics keep markets on edge — Last week’s Trump-Xi summit produced an agreement for a “100-day plan” to review U.S.-Chinese trade relations. Meanwhile, U.S.-Russian relations have deteriorated due to Russian support for Syrian President Assad. U.S. Secretary of State Rex Tillerson today will attend the Monday-Tuesday G7 foreign ministers meeting in Lucca, Italy and will then travel to Moscow for meetings with Russian Foreign Minister Sergey Lavrov.

Mr. Tillerson on Sunday said that the U.S. isn’t planning “regime change” in North Korea, but a U.S. aircraft carrier strike force has been diverted from Singapore to an area near North Korea from previous plans to sail to Australia. Treasury Secretary Mnuchin on Sunday said that the administration will be announcing new sanctions on North Korea, which could come as soon as this week. Mr. Mnuchin said the U.S. has been working with counterparts in China on those sanctions, suggesting that the Chinese government will not be surprised if the new sanctions ensnare some Chinese banks and businesses that do business with North Korea.

Congress left Washington last Friday and will be on recess through next week, meaning not much will get done on the Republican tax reform and infrastructure programs. When Congress returns from its 2-week recess, they will have only the last week of April to approve a new spending bill in order to prevent a government shutdown when the current continuing resolution expires on April 28.

Q1 earnings season kicks off — Q1 earnings season begins this week with 10 of the SPX companies reporting earnings. Large U.S. banks reporting on Thursday include Citigroup, JPMorgan Chase, and Wells Fargo. The market consensus for Q1 SPX earnings growth is +10.1% y/y (+6.2% ex-energy), according to surveys by Thomson I/B/E/S. Looking ahead, the consensus is for SPX earnings growth of +10.0% in Q2, +9.4% inQ3, and +13.4% for Q4. On a calendar year basis, the consensus is for earnings growth of +11.0% in 2017 and +12.1% in 2018 after barely positive earnings growth in 2015-16.

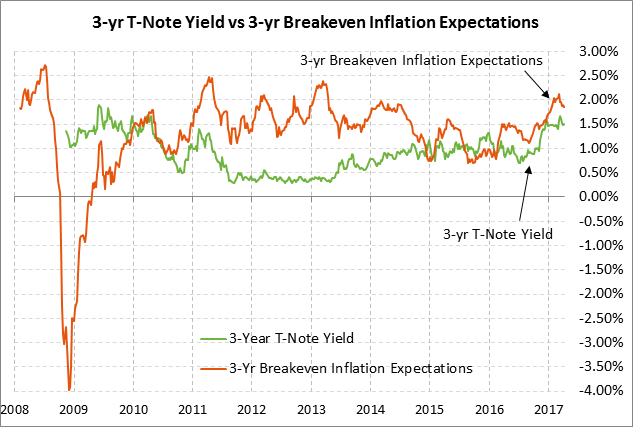

3-year T-note auction to yield near 1.53% — The Treasury today will sell $24 billion of 3-year T-notes. The Treasury will then continue this week’s $56 billion coupon package by selling $20 billion of 10-year T-notes on Tuesday and $12 billion of 30-year T-bonds on Wednesday.

Today’s 3-year T-note issue was trading at 1.53% in when-issued trading late last Friday afternoon. That translates to an inflation-adjusted yield of -0.32% against the 3-year breakeven inflation expectations rate of 1.85%. The 12-auction averages for the 3-year are as follows: 2.80 bid cover, $48 million in non-competitive bids, 4.2 bp tail to the median yield, 15.7 bp tail to the low yield, and 54% taken at the high yield. The 3-year is the second least popular security among foreign investors and central banks behind the 2-year T-note. Indirect bidders, a proxy for foreign buyers, have taken an average of only 51.7% of the last twelve 3-year T-note auctions, which is well below the average of 59.5% for all recent Treasury coupon auctions.