- U.S. dollar index sees only a mild boost so far from March rate-hike expectations

- U.S. trade deficit expected to widen

- U.S. consumer credit expected to rebound higher

- 3-year T-note auction to yield near 1.60%

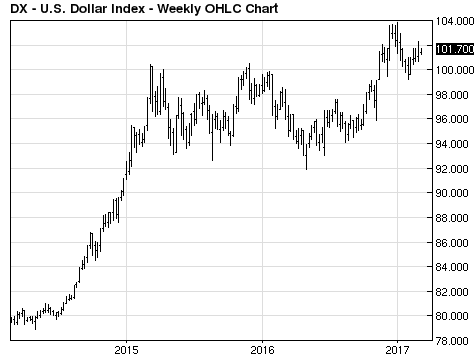

U.S. dollar index sees only a mild boost so far from March rate-hike expectations — The dollar index last week rallied by only +0.45% w/w even though the market dramatically ramped up market expectations for a Fed rate hike at next week’s FOMC meeting to just under 100% from 40% a week earlier. The dollar index on Monday closed slightly higher by +0.01% at 101.64 but below last Thursday’s 2-month high of 102.26.

The under-whelming performance of the dollar index in the past week suggests that the dollar may be in for a rather extended period of consolidation as the forex markets wait to see how quickly the Fed will actually raise interest rates. The dollar index rallied sharply by +6.2% after the November 2016 election to post a 14-year high in January 2017 on expectations for fiscal stimulus, a stronger economy, and a tighter Fed policy. However, the dollar index since January has corrected lower and is currently down by -2.1% from January’s 14-year high.

The long-term trend for the dollar undoubtedly remains bullish since the Fed is in the midst of a multi-year rate-hike regime, whereas the ECB and the BOJ are still engaged in large QE programs and have their policy rates pegged near or below zero. However, it appears that the dollar is going to take its time on moving higher in response to the Fed’s multi-year rate hike regime. The dollar index in any case has already rallied by +29% since May 2014 when the dollar index began its sharp climb in late 2014 and early 2015 in response to the end of QE3 in Oct 2014. But since then, the dollar has shown only modest gains in response to the Fed’s two 25-bp rate hikes seen so far (the first in Dec 2015 and the second in Dec 2016). That suggests that further dollar gains are going to be much more grudging than the initial surge on the end of QE3.

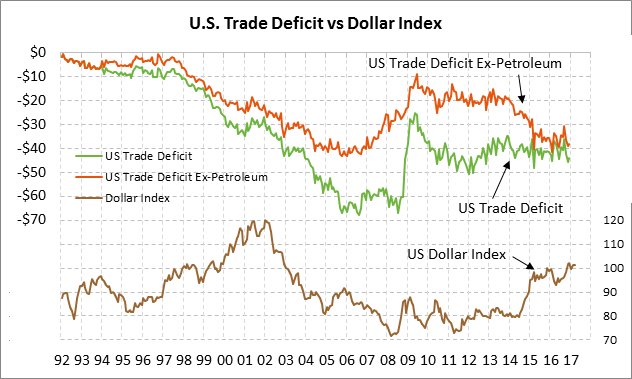

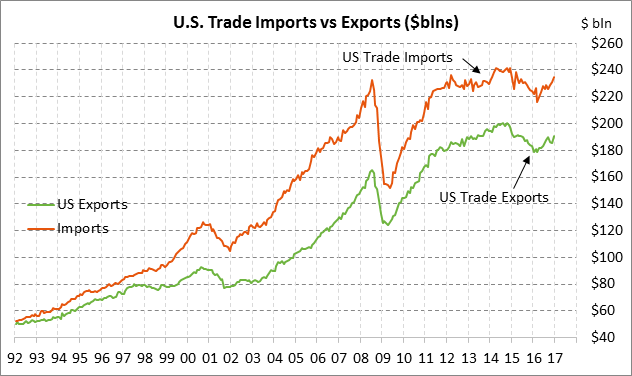

U.S. trade deficit expected to widen — The market is expecting today’s Jan trade deficit to widen to -$48.5 billion from -$44.3 billion in December, which would be substantially wider than the 12-month trend average of -$41.6 billion. The good news for the U.S. trade deficit is that exports in December showed a solid rise of +2.7% m/m and +4.2% y/y to a 1-3/4 year high of $190.688 billion. However, the bad news is that imports have risen sharply over the last three months by a total +4.0% and were up by +4.6% y/y, more than offsetting the progress on exports.

The U.S. trade deficit report has taken on much more political importance since the Trump administration is on the war path against countries that have large trade deficits with the U.S. In December, the U.S. had trade deficits of -$27.8 billion with China, -$6.5 billion with Japan, and -$5.3 billion with Germany. With its NAFTA partners, the U.S. in December had trade deficits of -$5.8 billion with Mexico and -$2.2 billion with Canada.

The bad news for the Trump administration is that the U.S. trade deficit is likely to widen this year. The U.S. trade deficit will see upward pressure in 2017 due to the general strength in the dollar, which makes U.S. exports more expensive and imports less expensive. In addition, the November OPEC production-cut agreement means that oil prices are likely to remain at least near current levels, keeping oil import values high.

The wide U.S. trade deficit continues to be a bearish underlying factor for the dollar since about $1.2 billion worth of dollars flow overseas every calendar day. However, those excess dollars are generally snapped up by overseas entities that want to hold U.S. assets or invest in the U.S., meaning that the U.S. trade deficit in the end has only a minor negative impact on the dollar.

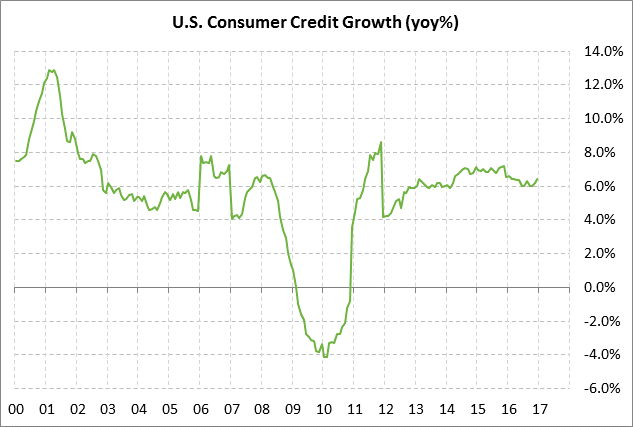

U.S. consumer credit expected to rebound higher — The market is expecting today’s Jan consumer credit report to rebound higher to +$18.0 billion from December’s weak report of +$14.16 billion. Today’s expected report of $18.0 billion would be mildly below the 12-month trend average of $18.9 billion. U.S. consumer credit continues to run strong and was up +6.4% y/y in December, matching the highest level in a year.

As for the breakdown of consumer credit, revolving credit (credit card debt) has strengthened in recent months as consumers apparently feel more comfortable about running up their credit card balances. Revolving credit was strong at +6.1% y/y in December, just below the 8-year high of +6.4% y/y posted in November. Meanwhile, installment loan growth for vehicles and school remained strong at +6.5% y/y in December.

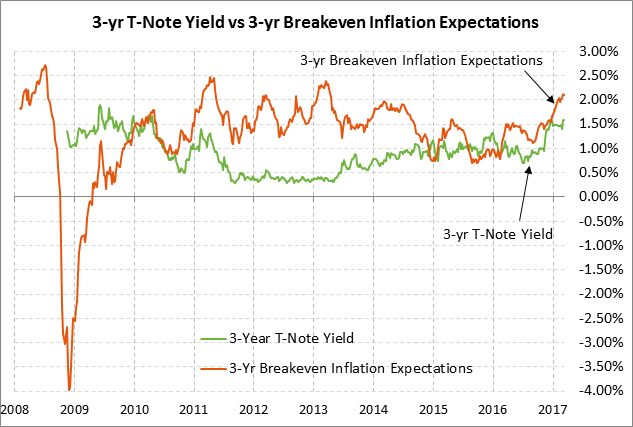

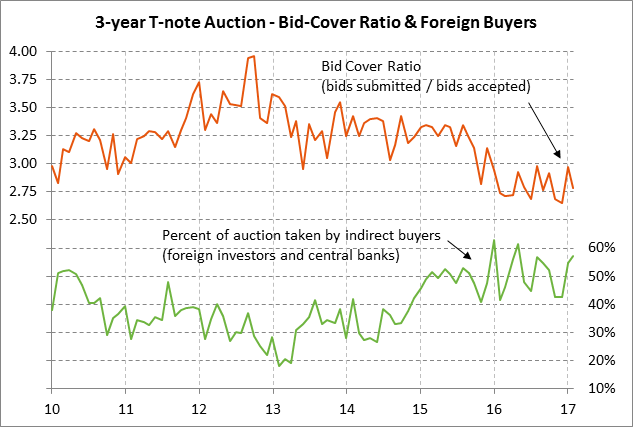

3-year T-note auction to yield near 1.60% — The Treasury today will sell $24 billion of 3-year T-notes. The Treasury will then continue this week’s $56 billion coupon package by selling $20 billion of 10-year T-notes on Wednesday and $12 billion of 30-year T-bonds on Thursday. The 10-year and 30-year auctions will be reopenings of the securities first sold last month.

Today’s 3-year T-note issue was trading at 1.60% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of -0.48% against the current 3-year breakeven inflation expectations rate of 2.08%.

The 12-auction averages for the 3-year are as follows: 2.80 bid cover ratio, $47 million in non-competitive bids, 4.1 bp tail to the median yield, 15.8 bp tail to the low yield, and 54% taken at the high yield. The 3-year is the second least popular security next to the 2-year T-note among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, haven an average of only 51.4% of the last twelve 3-year T-note auctions, well below the average of 59.2% of all recent Treasury coupon auctions.