Weekly market focus — The markets this week will focus on (1) Thursday’s Brexit vote in the UK, (2) Fed Chair Yellen’s testimony on monetary policy on Tuesday and Wednesday before Congress in which she is likely to remain cautious ahead of Thursday’s Brexit vote, (3) this week’s $107 billion deluge of Treasury coupon auctions on Monday through Wednesday, and (4) another light earnings week with only nine of the S&P 500 companies scheduled to report.

This week’s U.S. economic calendar is fairly busy starting on Wednesday with (1) the April FHFA home price index (expected +0.6% after March’s +0.7%), and (2) March existing home sales report (expected +1.8% after April’s +1.7%). Thursday brings (1) the preliminary-June Markit U.S. manufacturing PMI (expected +0.2 to 50.9 after May’s -0.1 to 50.7), (2) May new home sales (expected -9.5% after April’s +16.6%), and (3) May leading indicators (expected +0.1% after April’s +0.6%). Friday brings (1) May durable goods orders (expected -0.4% and +0.2% ex-transportation), and (2) final-June University of Michigan U.S. consumer sentiment index (expected -0.2 to 94.1 after the early-April report of -0.4 to 94.3).

Brexit week has finally arrived with implications for Fed policy as well — The markets by early Friday will finally be rid of the Brexit vote uncertainty one way or the other. The UK polls are open from 7:00 AM to 10 PM local time (2:00 AM to 5 PM ET) on Thursday. The first results are expected by about midnight local time (7 PM ET) on Thursday and final results are expected by about 7:00 AM local time on Friday (2 AM ET Friday).

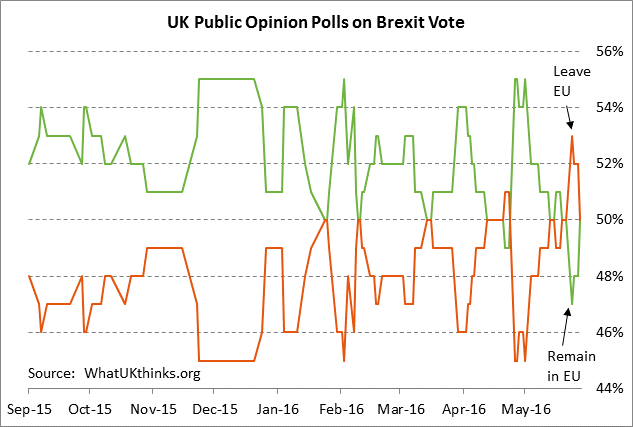

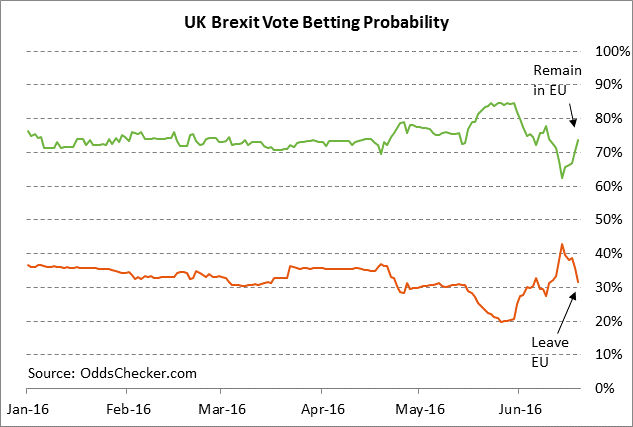

The “poll of polls” compiled by the website WhatUKThinks.org as of Sunday had the “Remain” and “Leave” vote exactly tied at 50%-50%. The Leave vote had taken the lead 52%-48% but the Remain vote then regained some ground after last Thursday’s murder of UK MP Jo Cox, which is thought to be supportive for the Remain vote on a shift towards the perceived safety of the status quo. The betting odds now have the Remain odds strengthening to 4/11 (73% probability) from a 62% probability before the tragic news of Ms. Cox’s murder. The betting odds for a Leave vote are now at 12/5 (29%).

The Remain camp is hoping for a last-minute break by the undecideds to the safety of the status quo, thus keeping the UK in the EU. However, there are a large number of undecideds that could be as high as 15% of the potential voters, meaning the vote could easily go either way depending on how the undecideds finally decide to vote.

We continue to believe that a UK vote to leave the EU would mainly be a move by the UK to shoot itself in the foot, with most of the negative effects accruing to the UK economy. However, a UK Brexit vote would also be politically damaging for Europe in its effort to keep its Eurozone members in line and would undercut European banks. Since the UK has its own currency and is not part of the Eurozone, we do not believe that a Brexit vote will turn out to be a systemic event that will fundamentally shake investor confidence.

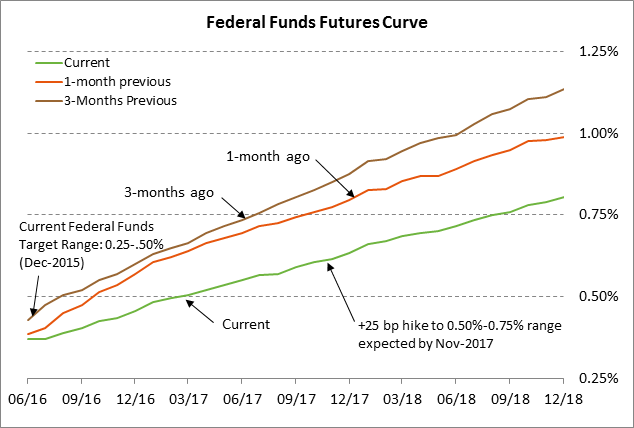

Fed policy expectations will be affected by Brexit outcome — Fed Chair Yellen testifies on monetary policy to Congress on Tuesday and Wednesday. Ms. Yellen just held a press conference last Wednesday after the June 14-15 FOMC meeting and her remarks this week are not likely to be much different than her remarks last week. The markets last week further deferred expectations for Fed rate hikes after the Fed dots became more dovish and Fed Chair Yellen admitted that the upcoming Brexit vote affected their decision.

Expectations for Fed policy this week will likely shift measurably in the hawkish direction if UK voters end up voting to stay in the EU. A UK Remain vote would remove a Brexit threat for a matter of years and would allow the Fed to shift its focus back to the U.S. economy. If the UK votes to leave the EU, on the other hand, then the impact on Fed policy will depend on whether the subsequent impact is localized to the UK and Europe or whether it spreads to the U.S.

2-year T-note auction to yield near 0.69% — The Treasury today will auction $26 billion of 2-year T-notes, kicking off this week’s $106 billion package of Treasury coupon securities. The Treasury on Tuesday will sell $34 billion of 5-year T-notes and then on Wednesday will sell three issues: $13 billion of 2-year floating rate notes, $28 billion of 7-year T-notes, and $5 billion of 30-year TIPS. The Treasury avoided any auctions on Thursday in the event of extreme market volatility on the UK Brexit vote.

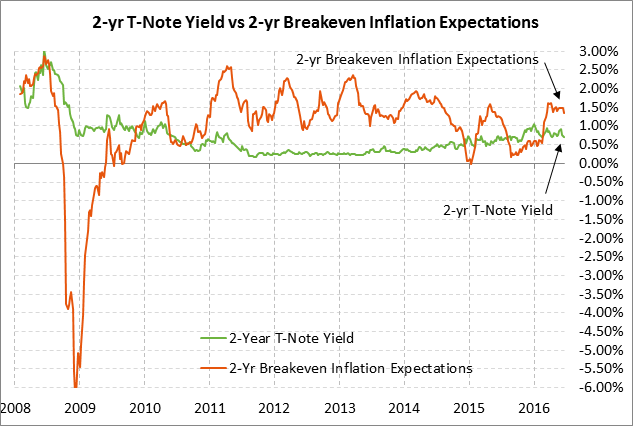

The benchmark 2-year T-note closed at 0.69% last Friday afternoon, which translates to an inflation-adjusted yield of -0.67% against the current 2-year breakeven inflation expectations rate of 1.36%. The 12-auction averages for the 2-year are as follows: 3.01 bid cover ratio, $154 million in non-competitive bids to mostly retail investors, 3.2 bp tail to the median yield, 12.0 bp tail to the low yield, and 49% taken at the low yield. The 2-year is the least popular coupon security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, took an average of only 48.2% of the last twelve 2-year T-note auctions, which is well below the average of 57.0% for all recent Treasury coupon auctions.