- Unemployment claims continue to indicate strong labor market

- U.S. import prices so far remain subdued ex-petroleum

- U.S. industrial production expected to recover from hurricane disruptions

- NAHB housing index expected to remain strong

- 10-year TIPS auction

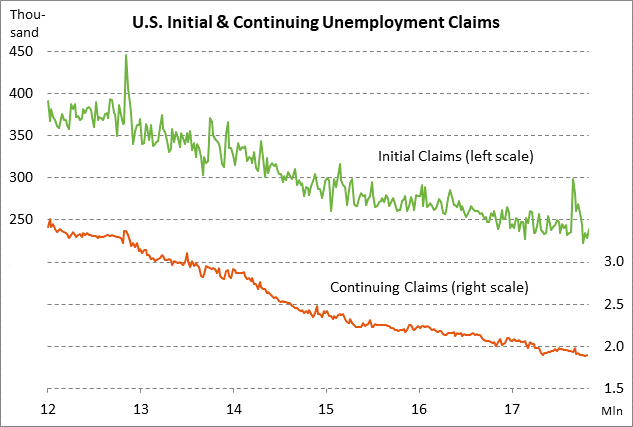

Unemployment claims continue to indicate strong labor market — The unemployment claims data is in better shape than before the Sep-Oct hurricane disruptions, illustrating the strength of the U.S. labor market. The initial claims series is currently only +16,000 above the 44-3/4 year low of 223,000 posted in the Oct 13 week and the continuing claims series is only +17,000 above the 44-year low of 1.884 million posted in the Oct 20 week. The consensus is for today’s initial claims report to show a -4,000 decline to 235,000 (after last week’s +10,000 increase to 239,000) and for continuing claims to show a -1,000 decrease to 1.900 million (after last week’s +17,000 increase to 1.901 million).

U.S. import prices so far remain subdued ex-petroleum — The headline import price index is putting upward pressure on the U.S. inflation indexes, but that is mostly due to the 5-month rally in oil prices since the import price index ex-petroleum remains subdued. In September, import prices were up by +2.7% y/y while import prices ex-petroleum showed a much smaller increase of +1.2% y/y. Still, the import price index ex-petroleum is likely to see upward pressure in coming months due to this year’s sharp decline in the dollar, which puts pressure on importers to raise prices to offset their currency losses from the weaker dollar.

The consensus is for today’s Oct import price index to show a +0.4% m/m rise, adding to Sep’s strong report of +0.7% m/m (+2.7% y/y). However, excluding petroleum, today’s Oct import price index report is expected to show a smaller +0.2% gain after Sep’s +0.3% increase.

The consensus is for today’s Oct import price index to show a +0.4% m/m rise, adding to Sep’s strong report of +0.7% m/m (+2.7% y/y). However, excluding petroleum, today’s Oct import price index report is expected to show a smaller +0.2% gain after Sep’s +0.3% increase.

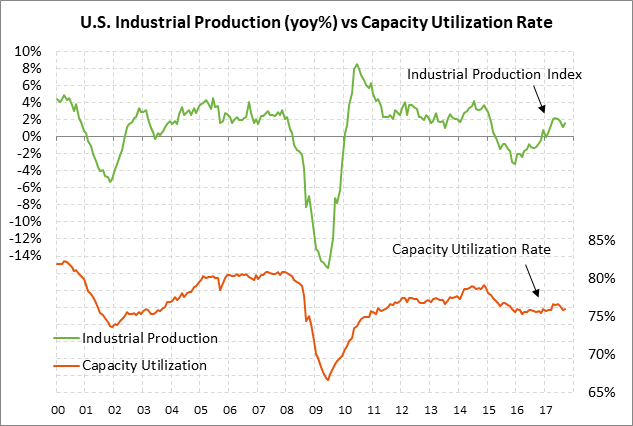

U.S. industrial production expected to recover from hurricane disruptions — Today’s Oct industrial production report is expected to strengthen as the effects of the Aug-Sep hurricanes dissipate. The consensus is for today’s Oct industrial production report to show a strong increase of +0.5%, adding to Sep’s +0.3% increase. Meanwhile, the consensus is for Oct manufacturing production to show an increase of +0.5% after Sep’s weak report of +0.1%.

The U.S. manufacturing sector is in generally good shape due to U.S. GDP growth near +3.0% in Q2-Q3 and due to exports picking up on stronger overseas economic growth and the generally weak dollar. Confidence in the manufacturing sector is strong with the ISM manufacturing index at 58.7 in October. Moreover, the manufacturing orders outlook looks very positive with the ISM manufacturing new orders sub-index at 63.4 in October.

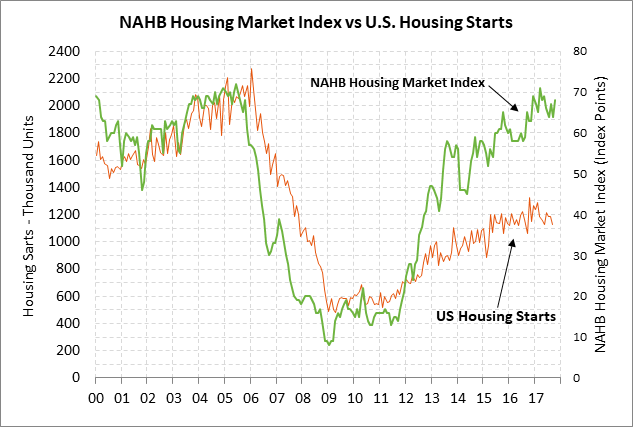

NAHB housing index expected to remain strong — U.S. home builder confidence in October was strong with the NAHB index at 68, which was just -3 points below the 12-year high of 71 posted back in March. The index dipped by -3 points to 64 in September due to hurricane disruptions but then more than recovered by +4 points to 68 in October. The consensus is for today’s report to show a small -1 point decline to 67. The Aug/Sep hurricanes disrupted home building activity, but those effects are dissipating and home builders now have the additional opportunity of replacing homes damaged by the hurricanes.

10-year TIPS auction — The Treasury today will auction $11 billion of 10-year TIPS in the second and last reopening of the 3/8% 10-year TIPS note of July 2027, which the Treasury first sold back in July. The 12-auction averages are as follows: 2.33 bid cover ratio, 6.7 bp tail to the median yield, 15.6 bp tail to the low yield, and 54% taken at the high yield. The 10-year TIPS is the third most popular security among foreign investors and central banks behind the 30-year TIPS and the 7-year T-note. Indirect bidders, a proxy for foreign buying, have taken an average of 67.3% of the last twelve 10-year TIPS auctions, which is well above the average of 61.8% for all recent Treasury coupon auctions.

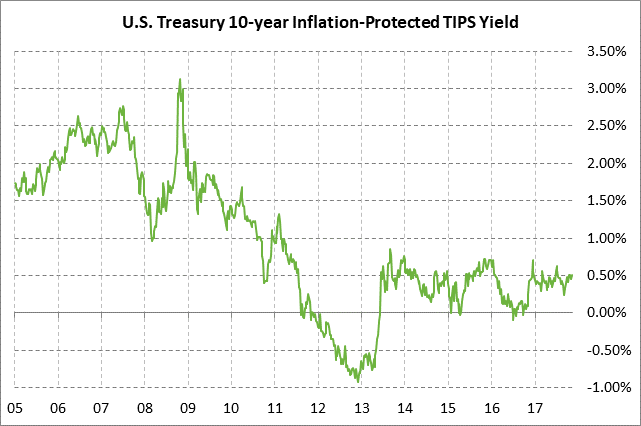

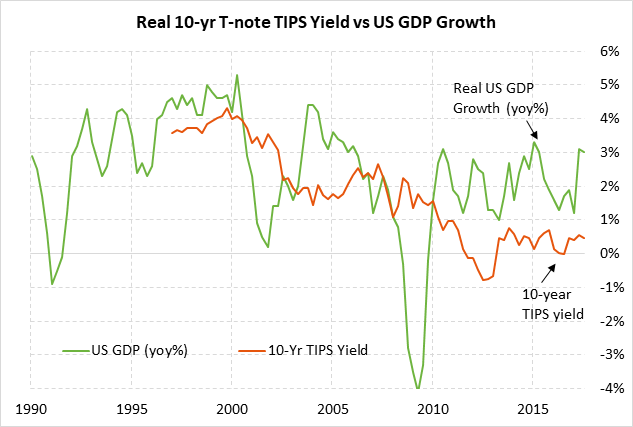

10-year TIPS yield remains subdued relative to historical levels — The current 10-year TIPS yield near 0.50% remains paltry relative to historical levels. The 10-year TIPS security compensates an investor for the cost of inflation and therefore provides an investor with essentially an inflation-adjusted, or real, yield.

The nearby chart illustrates how the 10-year TIPS yield traded near 4% back in the late 1990s when GDP was running at very strong levels near 4%. The 10-year TIPS yield in the 2003-2007 era then dropped to the 2% area when GDP was eased to an average of only about 2%. The 10-year TIPS yield then plunged during the 2008/2012 financial crisis era to negative levels. The 10-year TIPS yield in the past several years has averaged only about 0.40% even though GDP growth has returned to the 2% area.

The paltry 10-year TIPS yield can be attributed mainly to the post-crisis environment where the global financial system is awash with liquidity that is looking for a safe home like Treasury securities. The QE programs by the Fed, ECB, BOJ and BOE have contributed to this liquidity avalanche along with the long period of near-zero interest rates. The low 10-year TIPS yield can also be attributed to a continued dearth of capital spending investment activities by corporations. U.S. and European corporations continue to deal with the post-crisis economy in which they do not see particularly attractive capital investment projects and instead keep their cash in liquid securities or return it to shareholders via buybacks or dividends. The lack of demand for investment capital is a key factor that is keeping longer-term interest rates low in general.

The 10-year TIPS yield is likely to remain at paltry levels over at least the next several years. The 10-year TIPS is not likely to rise to more normal levels until global monetary policy normalizes and the global economy gets back to long-term strength with attractive investment opportunities.