- Today’s FOMC meeting will be overshadowed by Thursday’s Fed chair announcement

- House tax bill will be a pinata starting today

- ADP employment expected to rebound

- U.S. ISM manufacturing index expected to remain strong

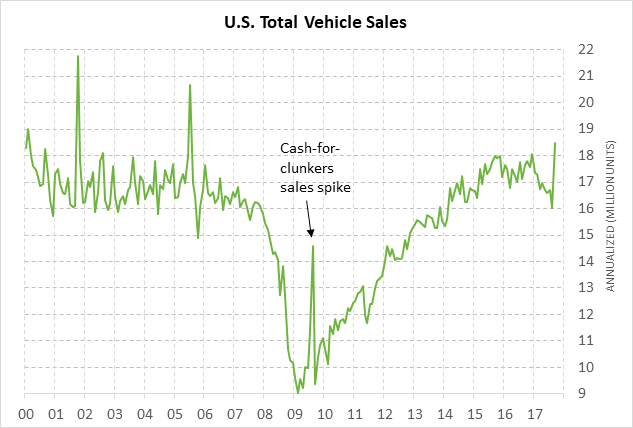

- U.S. vehicle sales expected to fall back after Sep’s hurricane surge

- Chinese government steps in to halt bond market hemorrhaging

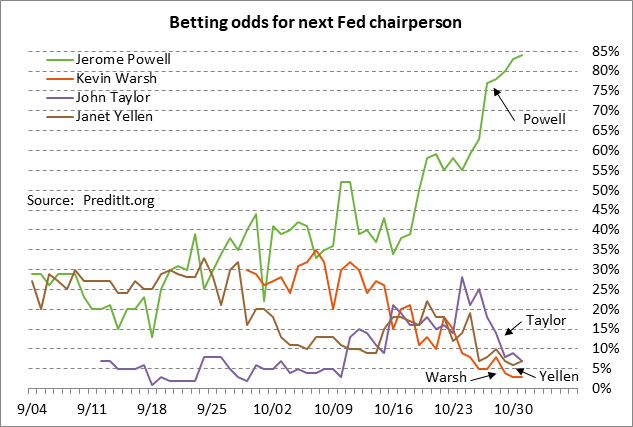

Today’s FOMC meeting will be overshadowed by Thursday’s Fed chair announcement — The 2-day FOMC meeting ending today is expected to be a nonevent, which means the main event will be the Trump administration’s announcement on Thursday of the new Fed Chair. All media reports and the betting odds continue to heavily favor Fed Governor Powell, who is broadly acceptable to the markets. The latest betting odds for the next Fed Chair are 84% for Powell, 7% for Yellen, 7% for Taylor, 3% for Warsh, and 2% for Cohn.

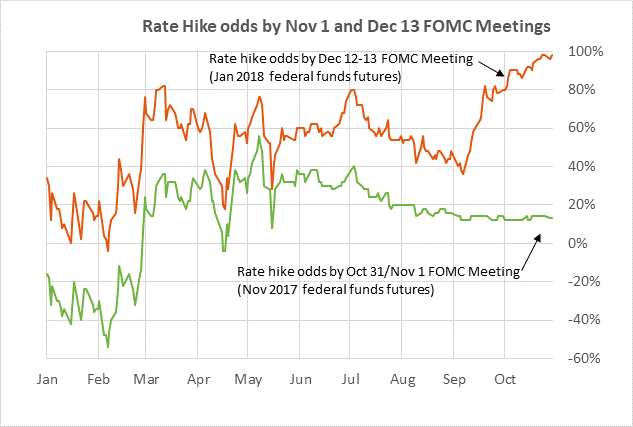

Meanwhile, the markets are discounting only a negligible 13% chance of a Fed rate hike today, based on the Nov 2017 federal funds futures contract. The market is not expecting a Fed rate hike today because (1) there is no Yellen press conference scheduled for today, and (2) the FOMC at its last meeting in September just made a tightening move by announcing the beginning of its balance sheet drawdown program on Oct 1. The FOMC this week is expected to let the balance sheet drawdown program settle in before making its third and final rate hike of the year at its next meeting on Dec 12-13. The market is discounting a 98% chance of a Fed rate hike at the December meeting.

House tax bill will be a pinata starting today — House Republicans today are scheduled to release their detailed tax reform bill. The Republican tax reform efforts will no longer be vague and aspirational but will rather be detailed enough to draw fire from many different quarters, mainly on the pay-fors to offset plans for $4-5 trillion in tax cuts over 10 years. House Speaker Ryan will try to jam the House tax bill through his caucus with as few changes as possible in order to meet his goal of passing tax reform within the next three weeks before Thanksgiving.

Speaker Ryan will likely be able to get some type of tax bill through the House, just as he was able to get a health care bill through the House after some misstarts. However, the tax bill will then land in the Senate where every Republican Senator will have a say on the contents of the bill since Majority Leader McConnell can afford to lose the support of only two Senators in order to sustain a majority vote. If and when the Senate passes a tax bill, then the House and Senate will have to iron out their different versions, unless House Republicans are willing to rubber-stamp the Senate version. Congressional Republicans are still aiming to get a bill passed and to President Trump’s desk by Christmas.

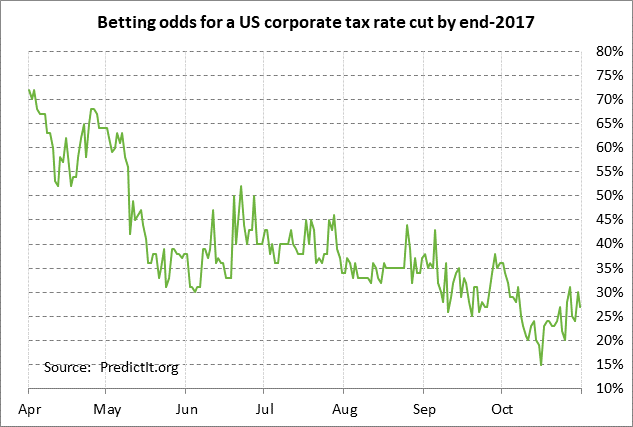

The markets have become more optimistic that Republicans will be able to get some type of tax cut bill through Congress, no matter how watered down it needs to be to get past the lowest common denominator of support. The betting odds remain slim at 27% for a signed bill by year-end, although the odds in our view are more like 70% for a deal by early 2018 since passing a tax cut bill has potentially become an existential issue for Republicans.

ADP employment expected to rebound — The market consensus is for today’s Oct ADP employment report to show an increase of +200,000, rebounding upward after hurricane disruptions caused a weak report of +135,000 in September. Meanwhile, the consensus is for Friday’s Oct payroll report to show an increase of +312,000, also rebounding higher from Sep’s hurricane-induced report of -33,000. Before the hurricane disruptions, payroll growth was respectable in June-Aug with a 3-month average of +172,000. The Sep unemployment rate fell to a 17-year low of 4.2%, illustrating underlying labor market strength.

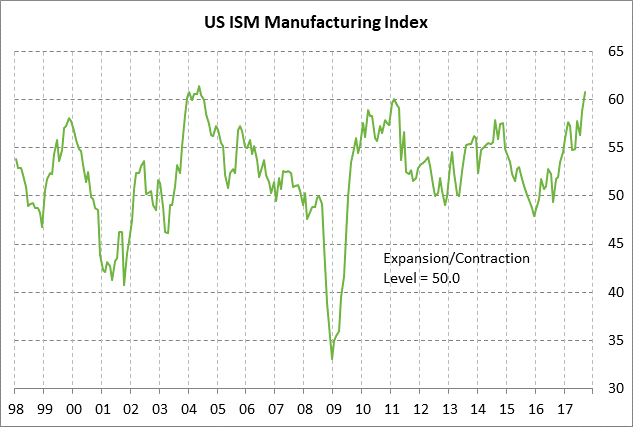

U.S. ISM manufacturing index expected to remain strong — The market consensus is for today’s Oct ISM manufacturing index to fall by -1.4 points to 59.4 after September’s +2.0 surge to a 13-1/4 year high of 60.8. The surge in manufacturing confidence in September was particularly impressive since it occurred in the face of severe hurricane disruptions. The outlook going forward looks particularly favorable with the Sep ISM new orders sub-index jumping by +4.3 points a 7-month high of 64.6, illustrating a full orders pipeline.

U.S. vehicle sales expected to fall back after Sep’s hurricane surge — The market consensus is for today’s Oct total vehicle sales report to fall back to 17.50 million units after the surge to a 12-1/4 year high of 18.47 million units in September. The surge in Sep vehicle sales was due to the replacement of vehicles damaged during Hurricanes Harvey and Irma. Vehicle replacement from hurricanes should continue to give a boost to the Oct sales figures.

Chinese government steps in to halt bond market hemorrhaging — The 10-year Chinese government bond yield on Tuesday finally fell by -4 bp to 3.89% from the previous session’s 3-year high of 3.93%. Since the Communist Party Congress concluded last week, the 10-year bond yield has surged by +16 bp just due to ideas that the government now has the go-ahead to resume its deleveraging campaign. After an overall bond-yield surge of +29 bp since the beginning of October, the PBOC on Tuesday stepped in to again inject reserves into the banking system, bringing the 4-day injection to a total of 230 billion yuan ($35 billion). The Chinese government appears determined to defend the 4% yield level in order to prevent a further surge in corporate bond costs and a downdraft in the stock market.