- Minutes from hawkish Sep 19-20 FOMC meeting will detail the unchanged “Fed dots”

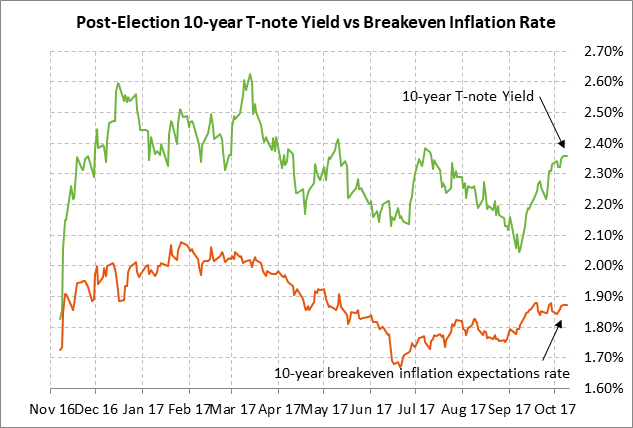

- 10-year T-note yield rises in close correlation with Fed rate-hike expectations

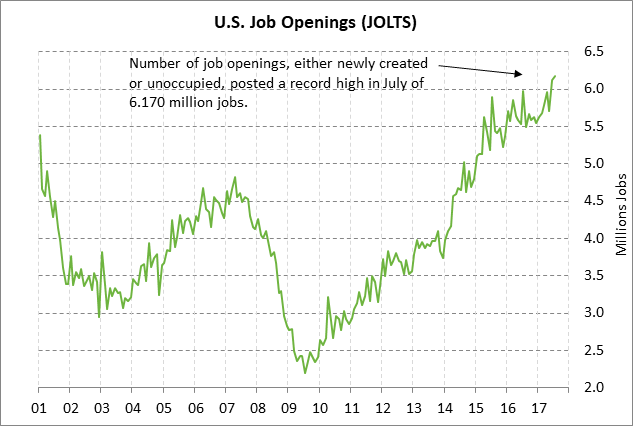

- U.S. JOLTS job openings expected to ease slightly from record high

- 3-year and 10-year T-note auctions

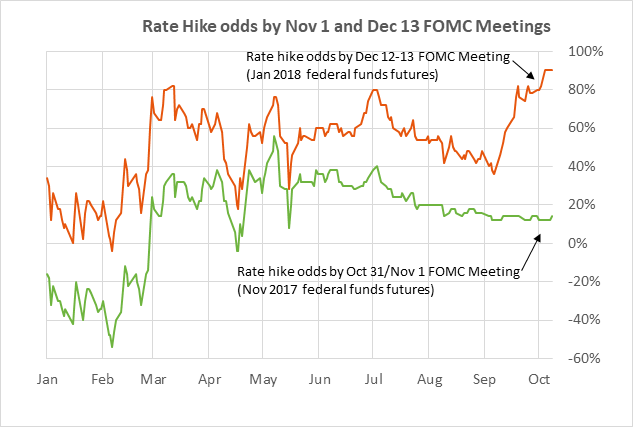

Minutes from hawkish Sep 19-20 FOMC meeting will detail the unchanged “Fed dots” — The FOMC at its Sep 19-20 meeting made its announcement that its balance sheet reduction program would begin in October, which was fully in line with market expectations and had little market impact. However, the markets greeted the Sep 19-20 meeting hawkishly because FOMC members left their “Fed dot” forecasts unchanged for another rate hike by December and three more rate hikes in 2018.

Prior to Sep 19-20 meeting, some market participants had been expecting at least some FOMC members to scale back their rate-hike expectations due to soft inflation figures and damage from hurricanes Harvey and Irma. Instead, the markets at the Sep 19-20 meeting were hit with the double-barreled news of an unchanged and hawkish rate-hike regime and the imminent beginning of the balance sheet drawdown.

When the FOMC’s post-meeting statement and forecasts were released in the early afternoon on Sep 20, Dec 10-year T-note prices fell by -14 ticks and the dollar index rallied by +0.9%. Since the Sep 19-20 FOMC meeting, the 10-year T-note yield has risen by +12 bp to 2.36% and the dollar index has risen by a net +1.6% due to even stronger expectations for Fed rate hikes. Specifically, the odds for a December rate hike have risen to 90% from 66% prior to the Sep 19-20 meeting.

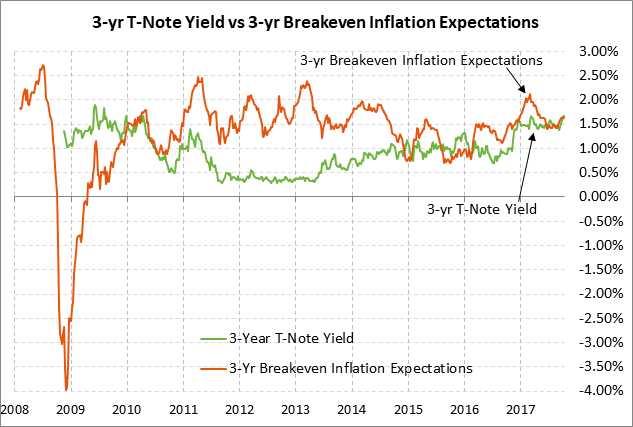

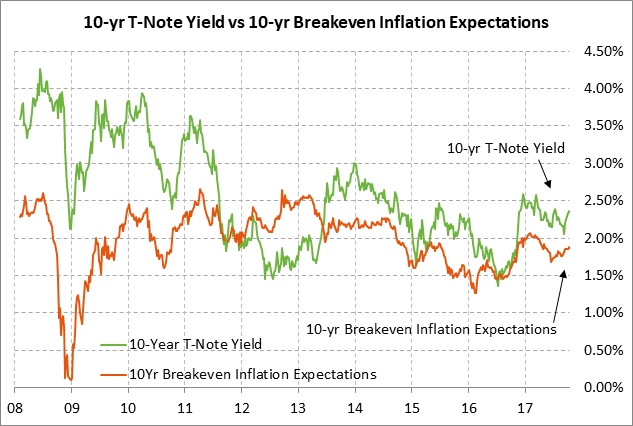

The odds for a December rate hike have risen in the past several weeks due to (1) persistently hawkish comments by key Fed officials, (2) the +13 rise in the 10-year breakeven inflation expectations rate since late-Aug to yesterday’s 5-month high of 1.88%, (3) less-than-expected hurricane damage, and (4) speculation that former Fed Governor Kevin Warsh might be appointed by President Trump as the new Fed chairperson, who is thought to be considerably more hawkish than the current Fed.

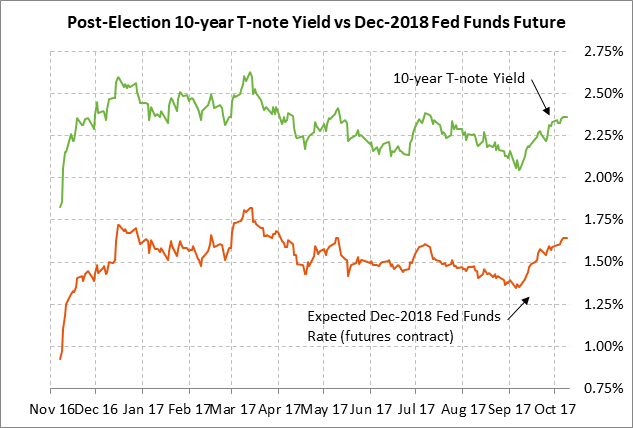

10-year T-note yield rises in close correlation with Fed rate-hike expectations — The rise in expectations for Fed tightening through end-2018 has dragged 10-year T-note yields higher in close correlation. Specifically, the Dec 2018 federal funds futures contract since Sep 5 has risen by +28 bp to the current level of 1.63%. The 1.63% yield on the Dec 2018 federal funds futures contract illustrates the market’s expectation for the Fed to raise the funds rate by another +50 bp over the next 14 months from the current target mid-point of 1.125% (1.00-1.25% target range).

The rise in Fed rate-hike expectations has been a primary factor causing the 10-year T-note yield to rise in recent weeks. In fact, the 10-year T-note yield since Sep 5 has risen by +30 bp to 2.36%, which is very close to the +28 bp rise in the Dec 2018 federal funds futures rate over the same time frame.

U.S. JOLTS job openings expected to ease slightly from record high — The market consensus is for today’s Aug JOLTS job openings report to show a -10,000 decline to 6.16 million, giving back a small portion of July’s +54,000 rise to 6.17 million. The series soared by +414,000 in June and then rose by another +54,000 in July to a record high of 6.17 million, illustrating that there is a plethora of jobs available in the U.S. Many of those job openings will turn into an actual job hire once the hiring process is complete, although some of those job openings may go begging if companies cannot find qualified people to fill the position.

Today’s Aug JOLTS report is likely to see some distortions from Hurricane Harvey, which made landfall on Aug 25 in Texas. However, the main effects from Harvey and Irma will be seen in the September report. Last Friday’s extremely weak Sep payroll report of -33,000 was mainly due to hurricane distortions. The markets generally ignored the -33,000 decline because the employment figure in the household survey soared by +906,000 and the Sep unemployment rate fell to a new 16-3/4 year low of 4.2%.

3-year and 10-year T-note auctions — The Treasury today will sell $24 billion of 3-year T-note and $20 billion of 10-year T-notes. The 10-year T-note auction will be the second and final reopening of the 2-1/4% note of Aug 2017 that the Treasury first sold in August. The Treasury will then conclude this week’s $56 billion coupon package by selling $12 billion of 30-year T-bonds on Thursday. The quotes late yesterday for the benchmark securities were 1.63% for the 3-year and 2.35% for the 10-year.

The 12-auction averages for the 3-year are: 2.82 bid cover ratio, $53 million in non-competitive bids, 4.6 bp tail to the median yield, 17.8 bp tail to the low yield, and 53% taken at the high yield. The 12-auction averages for the 10-year are: 2.28 bid cover ratio, $17 million in non-competitive bids, 5.4 bp tail to the median yield, 15.1 bp tail to the low yield, and 37% taken at the high yield.

Indirect bidders, a proxy for foreign investors and central banks, have taken an average of only 52.5% of the last twelve 3-year T-note auctions, which is well below the average of 61.0% for all recent coupon securities. However, indirect bidders have taken 62.6% of the last twelve 10-year T-note auctions, which is moderately above the 61.0% coupon average.