- Odds of a Dec rate hike reach a new high as focus remains on new Fed Chair appointment

- U.S. employment claims will continue to be distorted by hurricanes

- U.S. factory orders expected to show continued strength

- U.S. trade deficit expected to narrow mildly

Odds of a Dec rate hike reach a new high as focus remains on new Fed Chair appointment — There are four speaking engagements by Fed officials today including Fed Governor Jerome Powell (voter), San Francisco Fed President John Williams (non-voter), Philadelphia Fed President Patrick Harker (voter), and Kansas City Fed President Esther George (non-voter). The markets will of course be listening carefully for any comments on inflation and for any thoughts on whether the Fed should raise interest rates another notch in December. Fed Chair Yellen on Wednesday delivered comments to a community banking event but did not mention monetary policy.

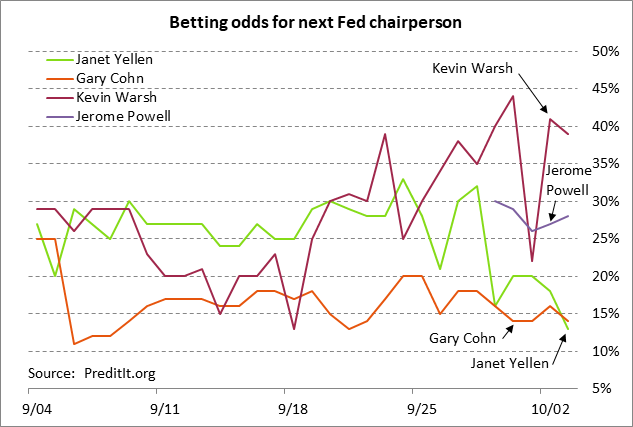

However, the market’s main area of interest at present is the next Fed chairperson. President Trump last Friday said he would make an announcement within two or three weeks. The bond market reacted negatively to reports late last week that former Fed Governor Kevin Warsh has a good shot at the position. The markets view Mr. Warsh as being substantially more hawkish than Ms. Yellen or Fed Governor Powell. Mr. Warsh a year ago said that the Fed missed a long window to tighten rates in 2013-15 and that the Fed seems to care too much about the impact of monetary policy on stock and asset prices. When he was a Fed governor, Mr. Warsh opposed QE2.

The latest betting odds at PredictIt.org for the next Fed chairperson are: Kevin Warsh 40%, Jerome Powell 26%, Gary Cohn 12%, Janet Yellen 10%, Neel Kashkari 8%, John Taylor 5%, Glenn Hubbard 3%, John Allison 1%.

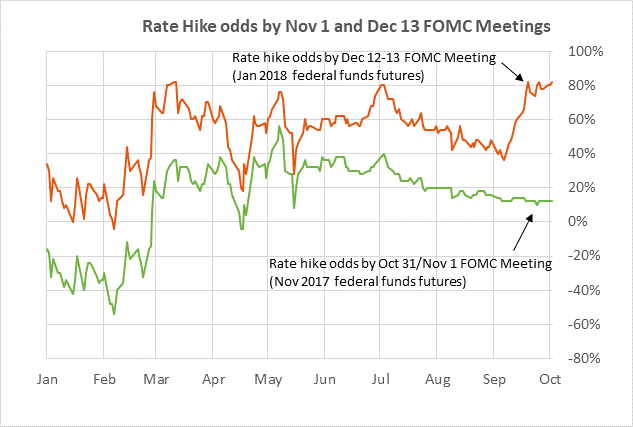

Meanwhile, the odds for a rate hike at the Dec 12-13 meeting on Wednesday rose to 82%, the highest level yet, according to the Jan 2018 federal funds futures contract. The odds of a Fed rate hike have risen because of the speculation that former Fed Governor Warsh may be named the next Fed chairperson, and also because of increased inflation expectations. The 10-year breakeven inflation expectations rate rose to a 4-3/4 month high of 1.89% last week but has since settled back to 1.86% due to the 4-session sell-off in crude oil prices.

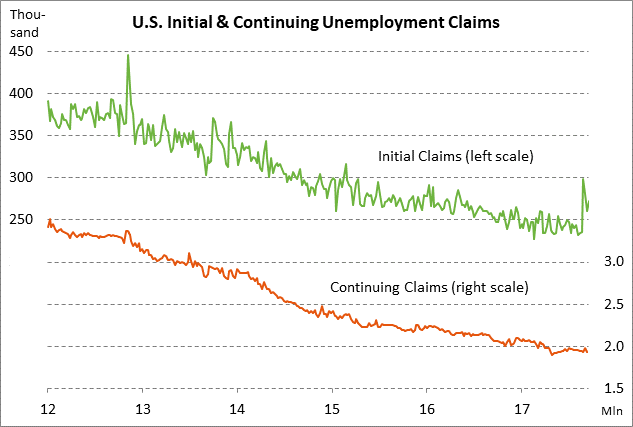

U.S. employment claims will continue to be distorted by hurricanes — The unemployment claims data will continue to be distorted by Hurricanes Harvey (landfall in Texas on Aug 25) and Hurricane Irma (landfall in Florida on Sep 10). Initial claims spiked higher by +62,000 in the week ended Sep 1 due to Hurricane Harvey. Claims have since come down by a net -26,000 from the peak but are still up by +37,000 from the pre-Harvey level. The market consensus is for today’s initial claims report for the week ended Sep 29 to show a -7,000 decline to 265,000 and for the continuing claims report for the week ended Sep 22 to show a +16,000 increase to 1.950 million.

On the labor front, the markets are mainly looking ahead to Friday’s Sep U.S. unemployment report. The Sep unemployment report will be distorted by Hurricanes Harvey and Irma, substantially reducing the importance of the report for monetary policy. The consensus is for a +80,000 increase in payrolls, which would be well below Aug’s +156,000 and the 12-month trend average of +175,000.

The good news is that Wednesday’s Sep ADP report showed an increase of +135,000, which was in line with expectations and provided support for ideas that Sep payrolls will show only a moderate drop from hurricane effects. In any case, job growth should quickly recover from the hurricanes as businesses resume operations and as new jobs emerge for hurricane cleanup and rebuilding efforts. Friday’s Sep unemployment rate is expected to be unchanged from Aug at 4.4%, which would be +0.1 point above the 16-year low of 4.3% posted earlier this year in May and July.

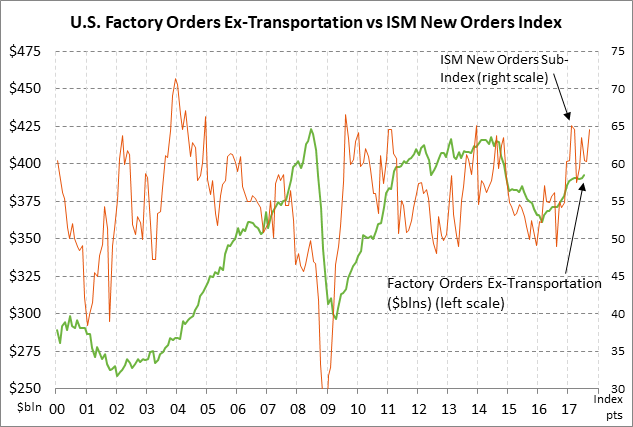

U.S. factory orders expected to show continued strength — The market consensus is for today’s Aug factory orders report to show a +1.0% increase, recovering after July’s aircraft-induced decline of -3.3%. U.S. factory orders in general remain in strong shape with factory orders ex-transportation rising by +0.5% m/m and +5.7% y/y in July. Moreover, the outlook for factory orders looks positive considering that this past Monday’s Sep ISM manufacturing new orders sub-index rose by +4.3 points to 64.6, which was just -0.5 points below the 8-year high of 65.1 posted earlier this year in February.

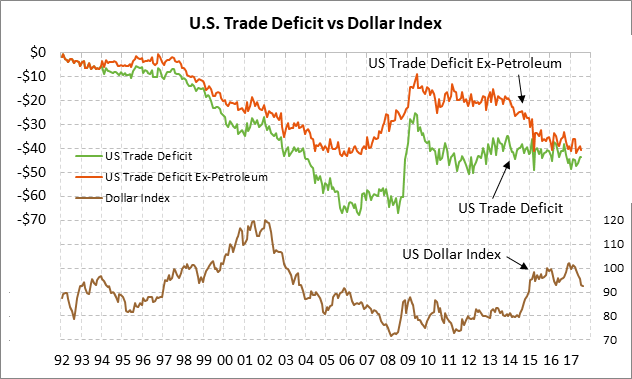

U.S. trade deficit expected to narrow mildly — The market consensus is for today’s Aug U.S. trade deficit to narrow mildly to -$42.7 billion from July’s -$43.7 billion. The expected report of -$42.7 would be a 1-year low and would be mildly narrower than the 12-month trend average of -$44.4 billion.

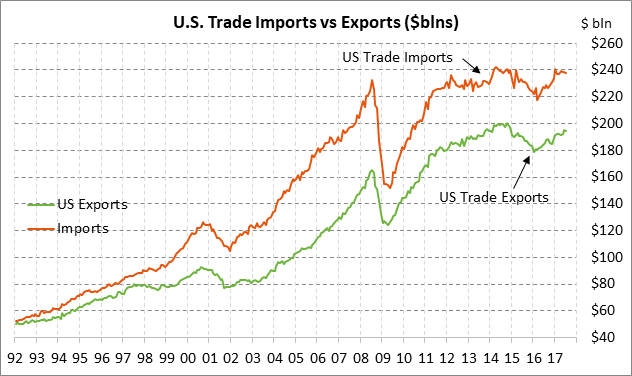

The good news for the U.S. trade deficit is that exports have risen fairly steadily over the last 1-1/2 years and were up +4.9% y/y in July. However, imports have risen at a similar rate and were up +5.1% y/y in July, which has prevented the U.S. trade deficit from showing much improvement. The U.S. deficit should see some narrowing pressure in coming months as this year’s sharp decline in the dollar has more impact on boosting exports and undercutting imports.

The wide U.S. trade deficit continues to be a bearish underlying factor for the dollar since about $1.2 billion worth of dollars flow overseas every calendar day. However, those excess dollars are a drop in the bucket for the FX markets, which trade an average of $5 trillion worth of currencies every day with 88% of that trade involving U.S. dollars, according to the BIS.