- Markets become more optimistic about a tax cut

- U.S. Q2 GDP expected unrevised from strong +3.0%

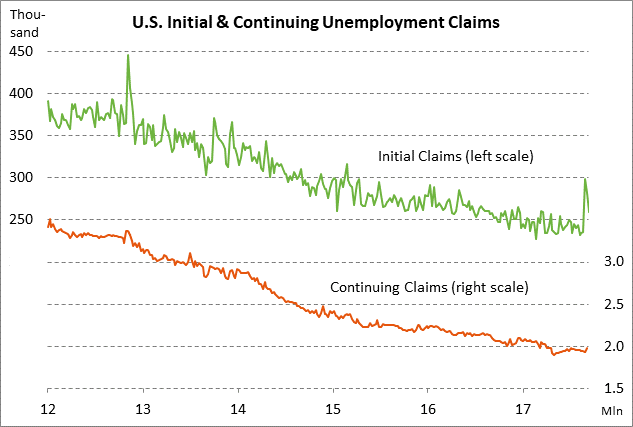

- Claims expected to continue to see hurricane distortions

- 7-year T-note auction to yield near 2.14%

Markets become more optimistic about a tax cut — The U.S. markets on Wednesday became a bit more optimistic that a tax deal might get done after President Trump introduced the plan and a 9-page outline of the plan became available to the public, the most detailed blueprint yet.

The tax cuts were fairly well outlined in the plan, but there was little detail on the pay-fors, which will be the crux of the problem. If Republicans cannot push through pay-fors, such as ending the deductibility of state income taxes, then they will not be able to reach their tax-cut goals unless they make the tax cuts temporary. Therefore, until a full plan is developed with realistic pay-fors, the markets will be skeptical that taxes can be cut as far as Republicans hope. In addition, the bond market will be concerned that Republicans will be tempted to bust the budget with tax cuts and insufficient pay-fors.

In any case, we believe that the Republican Congress will be able to eventually approve a version of a tax cut plan that is the lowest common denominator within the Republican caucus. After the Obamacare repeal debacle, failure is not an option for Republicans on a tax cut, even if the tax plan turns out to be much smaller than planned.

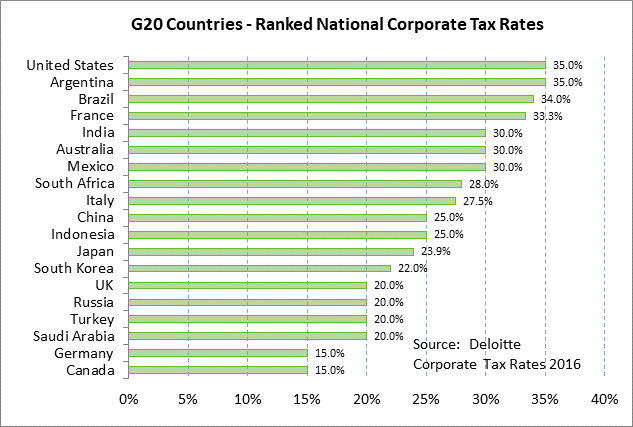

The stock market is pleased with the goal of cutting the top corporate tax rate to 20% from 35%. However, there was no detail in the plan about a repatriation program for causing U.S. corporations to repatriate some or all of the $2.6 trillion of cash they have stashed overseas. Much of that repatriated cash is likely to end up being used for stock buybacks, as it has in past repatriation programs, which would of course be bullish for stocks.

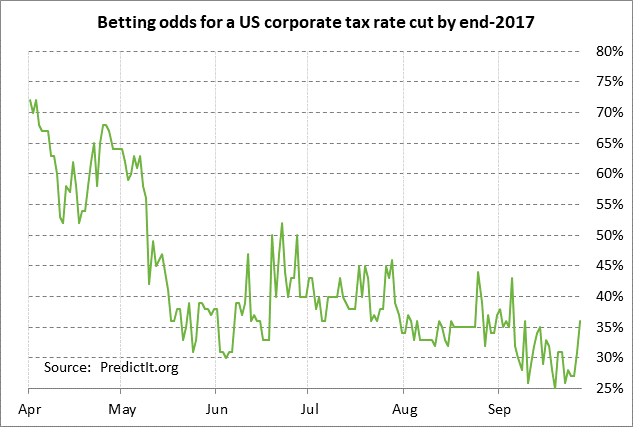

The betting odds for a corporate tax cut by the end of 2017 rose by +5 points on Wednesday to 36% at PredictIt.org, the highest level in three weeks. There was also been relative strength this week in high-tax stocks. The Goldman Sachs stock index of the 50 stocks in the S&P 500 with the highest effective tax rates (GSTHHTAX) has risen by a net +0.91% this week, far outperforming this week’s +0.19% net rise in the S&P 500 index. The high-tax index on Wednesday rose by +0.64% versus the +0.41% increase in the S&P 500 index.

The high-tax index substantially outperformed the S&P 500 index shortly after last November’s election on expectations for quick action on a tax cut, but the index then fell back and under-performed the broad market as the market lost faith in a tax cut. Some of that optimism is now returning.

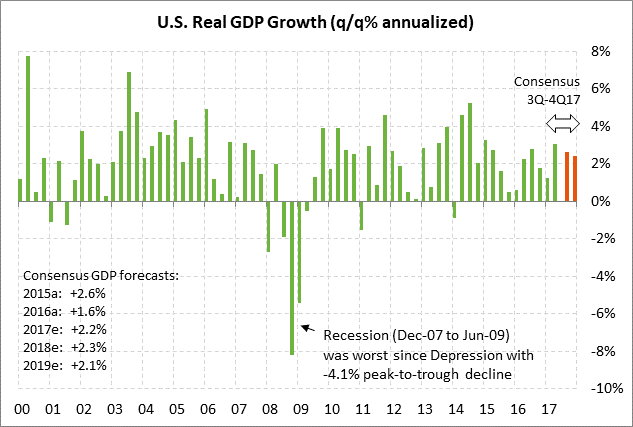

U.S. Q2 GDP expected unrevised from strong +3.0% — The market consensus is that today’s Q2 GDP report will be left unrevised at +3.0%, which represented a solid rebound from Q1’s weak pace of +1.2%. That would produce an average first-half GDP growth rate of +2.1%.

GDP in Q2 received a solid boost from personal consumption, which rose by +3.3% and contributed +2.28 points to the overall GDP figure. Business investment contributed +0.58 points to Q2 GDP, which was helpful but down from +1.27 points in Q2. The other categories of GDP (government, net exports, inventories) were little changed. The fact remains that consumers continue to be the key for the U.S. economy.

Looking forward, the market consensus is for U.S. GDP to settle in at +2.2% in Q3 and +2.3% in Q4. The Fed pegs longer-run U.S. potential GDP at +1.8%, but GDP is expected to be stronger than that in the second half of 2017 on a generally favorable domestic and overseas economic climate. The good news is that the GDP growth in the second half near +2.2% would be enough to keep the economy humming but not high enough to alarm the Fed into accelerating its rate-hike regime.

Claims expected to continue to see hurricane distortions — Today’s initial unemployment claims report for the week ended Sep 22 will continue to see distortions from Hurricanes Harvey (Aug 25 landfall) and Irma (Sep 15 landfall). The market consensus is for today’s initial claims report to show an increase of +11,000 to 270,000 (after last week’s -23,000 to 259,000) and for continuing claims to show a +13,000 increase to +1.993 million (after last week’s +44,000 to 1.980 million).

The initial claims series in last week’s report for the week ended Sep 15 was still +23,000 above the pre-Harvey level and today’s report will show the additional effects from Irma. With the upward impact from hurricanes, the continuing claims series last week was +81,000 above May’s 29-year low of 1.899 million.

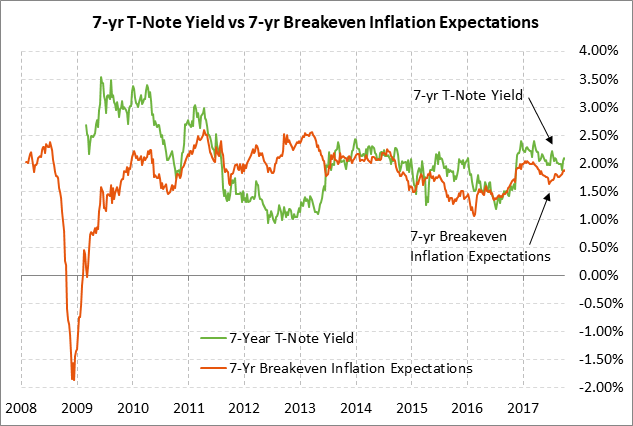

7-year T-note auction to yield near 2.14% — The Treasury today will sell $28 billion of 7-year T-notes, concluding this week’s $101 billion T-note package. Today’s 7-year T-note issue was trading at 2.16% in when-issued trading late Wednesday afternoon, which translates to an inflation-adjusted yield of 0.26% against the current 7-year breakeven inflation expectations rate of 1.90%.

The 12-auction averages for the 7-year are: 2.53 bid cover ratio, 4.5 bp tail to the median yield, 20.4 bp tail to the low yield, and 46% taken at the high yield. The 7-year T-note is the second most popular coupon security among foreign investors and central banks behind the 10-year TIPS. Indirect bidders, a proxy for foreign buyers, have taken an average of 67.5% of the last twelve 7-year T-note auctions, which is well above the average of 60.9% for all recent Treasury coupon auctions.