- Weekly global market focus

- Washington drama dwindles to 2018 budget

- UN vote due today on new North Korean sanctions

- Odds for year-end Fed rate hike fall to a new 4-month low

- U.S. stock market remains resilient

- 3-year T-note auction

Weekly global market focus — The U.S. markets this week will focus on (1) hurricane damage to the U.S. economy after Hurricane Irma hit Florida over the weekend and as Hurricane Jose is in the Atlantic with the potential to threaten the U.S. East Coast in about a week, (2) the potential for a new North Korean provocation as the UN Security Council today is expected to vote on a new sanctions package, (3) whether the U.S. inflation situation is soft enough to cause the Fed to defer a rate hike with Wednesday’s Aug PPI report and Thursday’s Aug CPI report (expected +1.8% y/y vs July’s +1.7%; core expected +1.6% y/y vs July’s +1.7%), (4) oil and gasoline prices, which continue to be buffeted by hurricane factors, and (5) the Treasury’s sale of $56 billion of 3, 10 and 30-year securities on Mon-Wed. Oracle is the only S&P 500 company that will report earnings this week.

In Europe, the focus is mainly on Thursday’s Bank of England meeting, which is expected to produce an unchanged policy amidst rocky Brexit negotiations. The ECB at its meeting last week began the discussion about 2018 QE tapering but said that a decision would have to wait until their next meeting on Oct 26. The German national election is now less than 2 weeks away (Sep 24) with Chancellor Merkel remaining the overwhelming favorite. In China, the focus is on Wednesday evening’s (ET time) Aug industrial production report (expected +6.6% y/y vs July’s +6.4%) and Aug retail sales report (expected +10.5% y/y vs July’s +10.4%).

Washington drama dwindles to 2018 budget — The drama in Washington eased substantially last week after Congress easily approved a debt ceiling suspension and a continuing resolution through Dec 8. The threat of a U.S. government shutdown will not arise again until Dec 9 and a debt ceiling increase will not be needed until February or March when the Treasury’s emergency maneuvers run out.

Congress will be in session this week and the main order of business as far as the markets are concerned is passage of a 2018 budget resolution and Congressional consideration of tax reform. Congress needs to pass a non-binding 2018 budget as the vehicle for passing tax reform through the reconciliation process. Meanwhile, the markets will be carefully watching the development of the Republican tax reform bill that has been placed in the hands of Congressional tax committees.

UN vote due today on new North Korean sanctions — The Trump administration has called for a UN Security Council vote today on a package of sanctions against North Korea that includes an oil embargo, a ban on North Korean textile exports, and a prohibition on North Korean guest workers. China and Russia have expressed opposition to a complete oil embargo against North Korea but may go along with a partial embargo or temporary measures. However, a Trump administration official was quoted as saying that the U.S. would rather see a veto of the package rather than a dilution of the sanctions. If the UN Security Council does approve new North Korean sanctions, then North Korea may lash out with a new provocation that alarms the markets.

If the UN Security Council does not approve stepped-up sanctions today, Treasury Secretary Mnuchin has said he has an executive order ready for President Trump to sign that would give the president the authority to halt trade and put sanctions on any nation that does business with North Korea. That executive order could spook the markets if it appears that Mr. Trump might use the order against Russia or China.

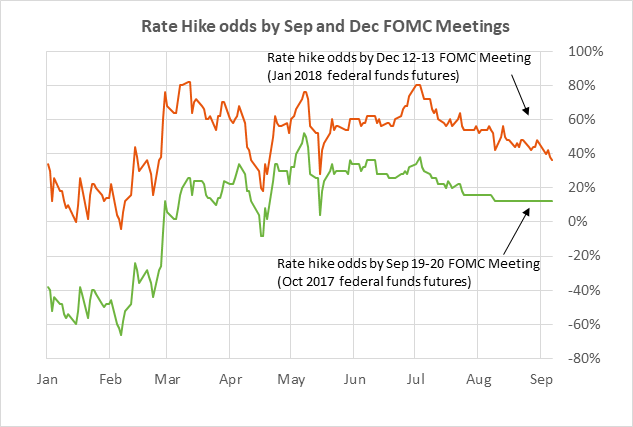

Odds for year-end Fed rate hike fall to a new 4-month low — The odds for a Fed rate hike by December fell to a 4-month low of 36% last Friday, based on the Jan 2018 federal funds futures contract. The odds for a Fed rate hike by year-end have fallen to 36% from 60% in July mainly because of (1) low inflation figures, (2) the severe hurricane damage from Hurricanes Harvey and Irma, and (3) the ECB’s slow consideration of QE tapering. However, the market consensus is that the Fed at its meeting next week (Sep 19-20) will announce the start date for its balance sheet reduction program, which may be as soon as Oct 1.

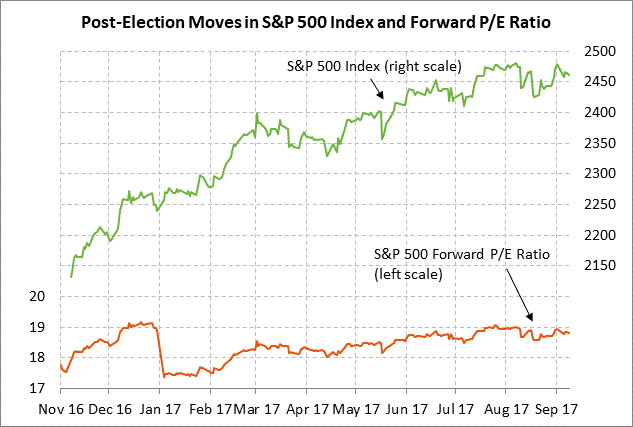

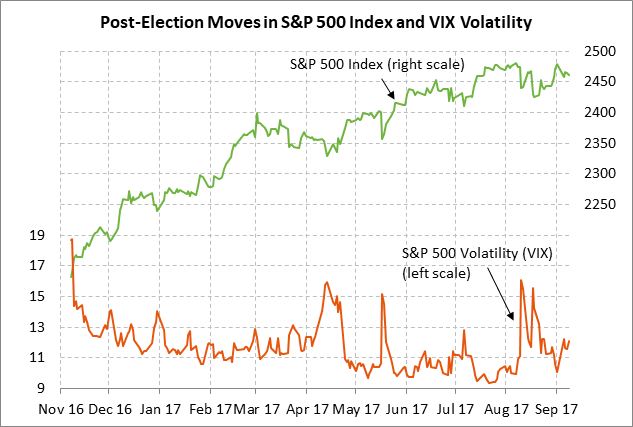

U.S. stock market remains resilient — The U.S. stock market last week remained resilient with a weekly decline of only -0.61% despite the damage from Harvey and the impending damage from Hurricane Irma. Stocks last week received a boost from (1) the elimination of the near-term threat of a U.S. government shut-down and Treasury default after Congress last week approved a 3-month debt ceiling suspension and CR, (2) last Friday’s fall in the 10-year T-note yield to a new 10-month low of 2.01% along with the 4-month low in expectations for a Fed rate hike by year-end, and (3) last Friday’s 2-3/4 year low in the dollar index which is supportive for U.S. exports and the value of repatriated earnings. Yet valuations remain stretched with the S&P 500 forward P/E at 18.8 (vs the 5-year average of 16.4 and the 10-year average of 15.2).

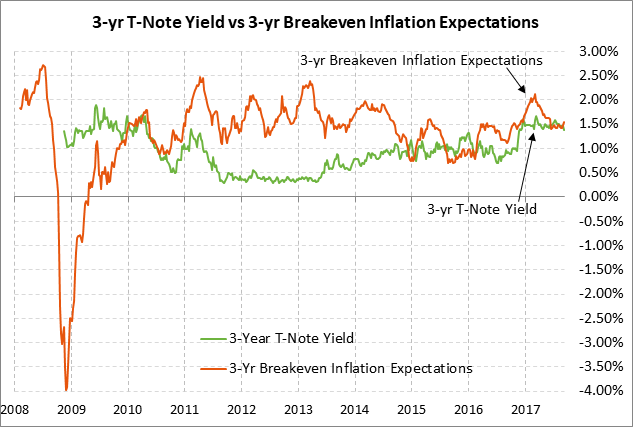

3-year T-note auction — The Treasury today will sell $24 billion of 3-year T-notes. The Treasury will then continue this week’s $56 billion coupon package by selling $20 billion of reopened 10-year T-notes on Tuesday and $12 billion of reopened 30-year bonds on Wednesday. The benchmark 3-year T-note last Friday closed at 1.37%, which translates to an inflation-adjusted yield of -0.16% against the current 3-year breakeven rate of 1.53%. The 12-auction averages for the 3-year are: 2.83 bid cover, $53 million in non-competitive bids, 4.4 bp tail to the median yield, 17.0 bp tail to the low yield, 48% taken at the high yield, and 53.2% taken by indirect bidders (well below the average of 60.9% for all recent Treasury coupon auctions).