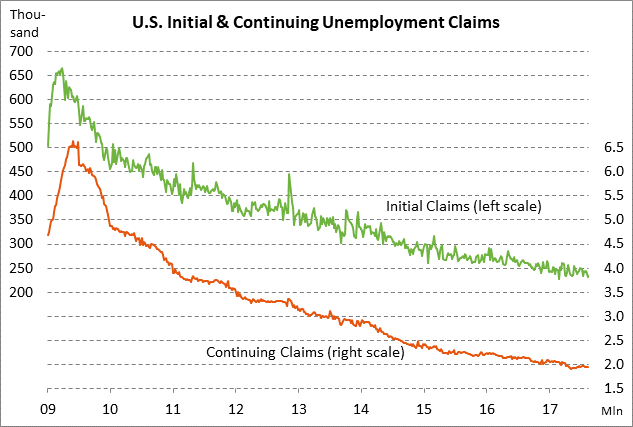

- U.S. unemployment claims will start to be distorted by Harvey

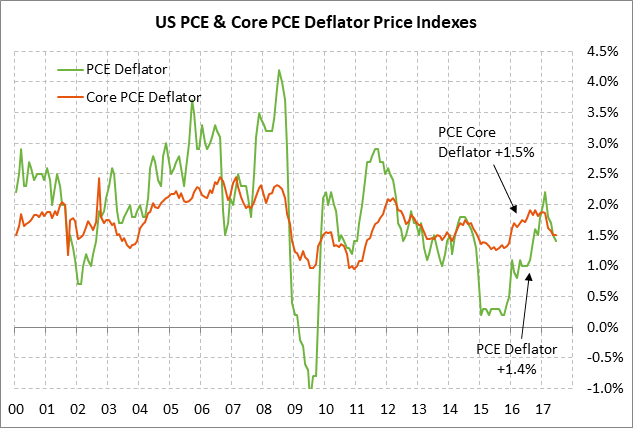

- Fed’s preferred inflation measure expected to remain tepid

- Chicago PMI expected to remain strong

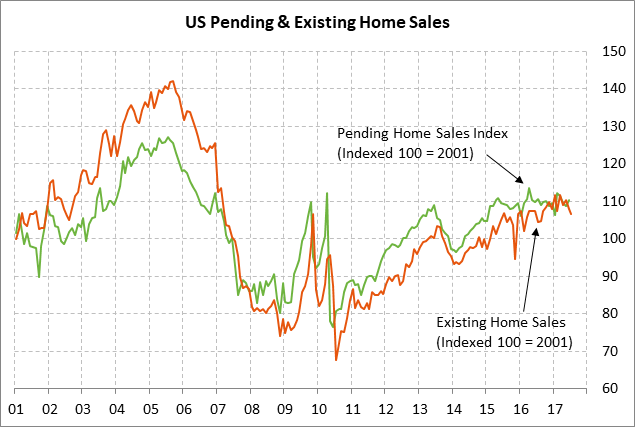

- U.S. pending home sales expected to show a small increase

U.S. unemployment claims will start to be distorted by Harvey — The initial and continuing unemployment claims series both remain in favorable shape, illustrating a tight U.S. labor market where businesses are holding on tightly to their employees. The initial claims series is only +7,000 above the 44-1/2 year low of 227,000 posted in February and the continuing claims series is only +55,000 above the 29-year low of 1.899 million posted in May.

The consensus is for today’s initial claims report to show a +4,000 gain to 238,000 (after last week’s +2,000 to 234,000) and for continuing claims to show a -2,000 decline to 1.952 million (after last week’s unchanged at 1.954 million). Today’s claims report will begin to show the effects of Hurricane Harvey since today’s report is for the week ended Oct 25, which was the day the storm hit the Texas coast.

On the labor front, the market is mainly looking ahead to Friday’s Aug U.S. unemployment report. The consensus is for Aug payrolls to show an increase of +180,000, which by no coincidence would exactly match the 12-month trend average. Payroll growth recently showed some weakness in March (+50,000) and May (+145,000), but otherwise payrolls have shown increases of more than +200,000 in every other month this year.

Expectations for Friday’s payroll report were bolstered by Wednesday’s ADP report, which showed a stronger-than-expected increase of +237,000 (vs expectations of +185,000) and a +24,000 upward revision for July (to +201,000 from +178,000).

Fed’s preferred inflation measure expected to remain tepid — The market is expecting today’s PCE deflator report to remain tepid. The July headline figure is expected to be unchanged at +1.4% y/y and the July core figure is expected to ease slightly to +1.4% y/y from June’s +1.5%. The expected headline and core PCE deflator figures of +1.4% would be well below the Fed’s inflation target of +2.0%.

The U.S. inflation figures have fallen substantially in the past several months. The PCE deflator has fallen by -0.8 points to +1.4% y/y from the 5-year high of +2.2% posted in February. The core PCE deflator has fallen by -0.4 points to +1.5% y/y from the 5-year high of +1.9% posted in Dec-Jan. Similar declines have been seen in CPI figures.

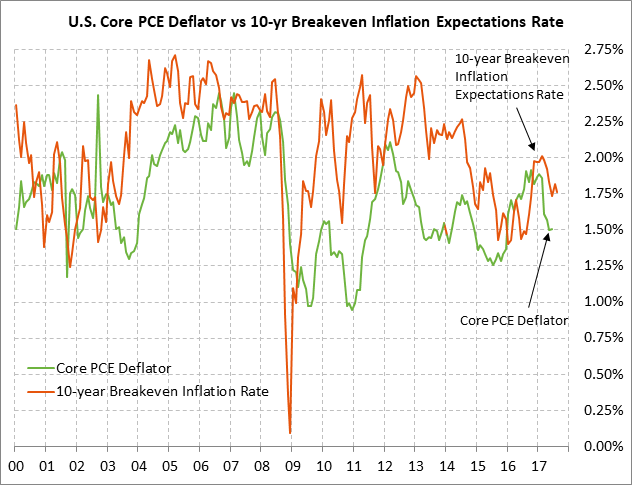

The Fed continues to struggle with the question of whether the recent decline in the inflation figures is simply being caused by transitory factors such as lower cell-phone and prescription drug prices. The alternative is that the decline in the inflation figures could be due to more fundamental disinflationary forces, which would be of much greater concern to the Fed. In fact, several FOMC members have been vocal in saying that they will not favor another rate hike until the inflation outlook turns higher.

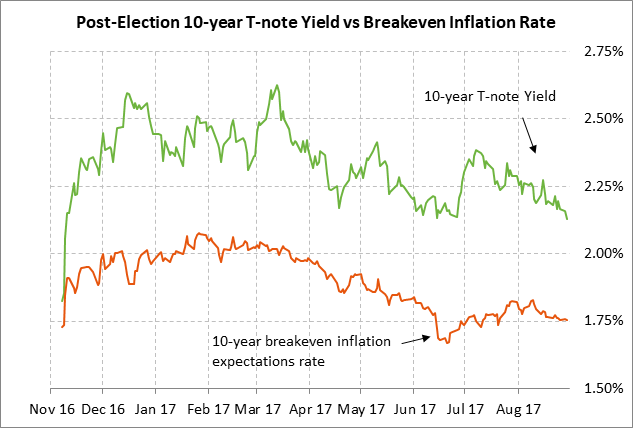

Market-based measures of inflation expectations have fallen as well as the inflation statistics themselves, suggesting that the markets believe that the recent decline in inflation is more than transitory. The 10-year breakeven inflation expectations rate in recent months has eased to 1.75% from the 2% level seen after the November 2016 election.

The weak inflation figures are the key factor that has caused the market to reduce expectations for Fed rate hikes through 2018. The market is now discounting the odds for a Fed rate hike by December at only 44%, based on the January 2018 federal funds futures contract. The market is not fully discounting the next 25 bp rate hike until the end of 2018, which is dramatically more dovish than the Fed-dot forecasts for one more rate hike this year and three rate hikes in 2018.

Chicago PMI expected to remain strong — The market consensus is for today’s Aug Chicago PMI report to show a small -0.4 point decline to 58.5, adding to July’s sharp -6.8 point decline to 58.9. Even after July’s sharp decline, the Chicago PMI figure of 58.9 is still relatively strong and indicates continued strong confidence in the Chicago-area manufacturing sector.

On a national scale, the market is looking ahead to Friday’s Aug ISM manufacturing index, which is expected to show a small +0.2 point gain to 56.5, stabilizing after July’s -1.5 point decline to 56.3. Manufacturing confidence rose moderately after the November 2016 election and remains relatively strong. The Republican agenda has been disappointing thus far, but U.S. manufacturing executives have other things to be pleased about, including (1) strong Q2 GDP of +3.0%, (2) improved European and Chinese growth, and (3) the sharp decline in the dollar this year that has boosted U.S. exports.

U.S. pending home sales expected to show a small increase — The market consensus is for today’s July pending home sales report to show an increase of +0.4% m/m, adding to June’s +1.5% increase. The pending home sales series is a leading indicator for the existing home sales series by 1-2 months as signed contracts turn into closed sales.

U.S. existing home sales remain in generally strong shape at 5.44 million units, which is only -4.6% below March’s 10-year high of 5.70 million units. Demand for homes remains strong due to the strong consumer confidence, rising household income and wealth, and low mortgage rates. However, home sales are being crimped to some extent by a tight supply of homes on the market and by the sharp +39% rise in home prices that has been seen since the housing market bust ended.