- ECB’s dovish meeting helps cool bund and T-note yields

- High U.S. stock market valuation means market is vulnerable to any disappointments

ECB’s dovish meeting helps cool bund and T-note yields — The ECB at its meeting on Thursday left intact its conditional pledge to expand QE if the Eurozone outlook should deteriorate. In a prior Bloomberg survey, about half of the respondents predicted that the ECB would remove that pledge. The fact that the ECB instead left its QE pledge intact was a dovish signal to the market regarding ECB policy intentions. More generally, the ECB did not want to spark any new rise in Eurozone bond yields by removing that pledge. In fact, ECB President Draghi noted in his post-meeting press conference that the last thing the ECB wants is “an unwanted tightening” of financial conditions.

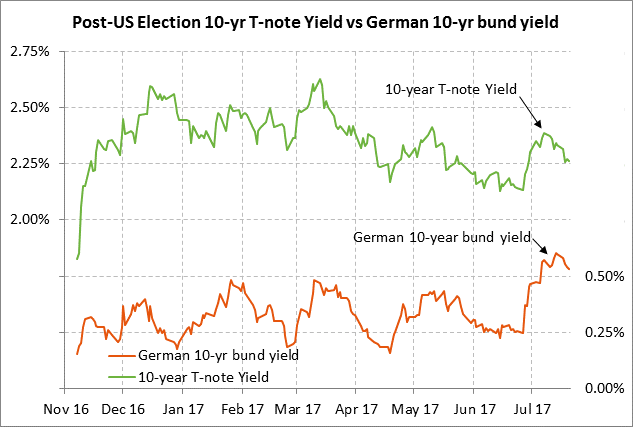

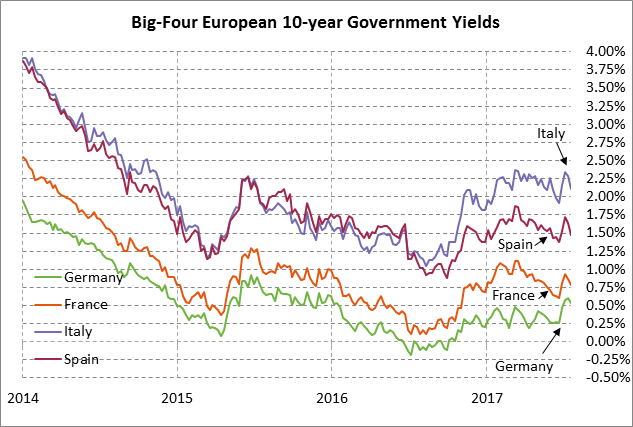

However, tighter financial conditions are exactly what happened when Eurozone bond yields surged after ECB President Draghi in his June 28 speech in Sintra, Portugal said that reflationary forces have replaced deflationary forces and that the parameters of monetary policy could be adjusted as the Eurozone economy continues to improve. The German 10-year bund yield after Mr. Draghi’s Sintra speech soared by 35.8 bp to a 1-1/2 year high of 0.603% on July 12.

Thursday’s dovish ECB meeting outcome caused the German 10-year bund yield to ease by -1.2 bp to 0.530%. The bund yield is now down by -7.3 bp from its mid-July 1-1/2 year high of 0.603%.

We expect the ECB to now lay low through August as it tries to keep the markets soothed and keep bond yields from rising. However, the ECB’s action plan for autumn has now been compressed because the ECB must give the markets at least a 1-2 month notification of what will happen to QE starting in January 2018. The ECB has so far only said that its 60 billion euro per month QE program will last through December 2017.

The ECB has only three meetings left in 2017, i.e., on Sep 7, Oct 26, and Dec 14. That is why the markets have been expecting the ECB to announce its early 2018 QE plans at its Sep 7 meeting, or possibly as late as its Oct 26 meeting. The current market consensus is that the ECB will taper its QE program down to zero during the first nine months of 2018.

The recent -7.3 bp decline in the 10-year bund yield from its early-July high has helped allow the 10-year T-note yield to decline as well. The 10-year T-note yield clearly followed the bund yield higher in the two weeks following Mr. Draghi’s June 28 Sintra speech. During roughly that same 2-week period when the 10-year bund yield surged by 35 bp to 0.60%, the 10-year T-note yield rose by 18 bp to a 2-month high of 2.39% on July 7. Since that high, the 10-year yield has fallen by -13 bp to the current level of 2.26%. The U.S. T-note market will continue to closely watch and partially track the bund market.

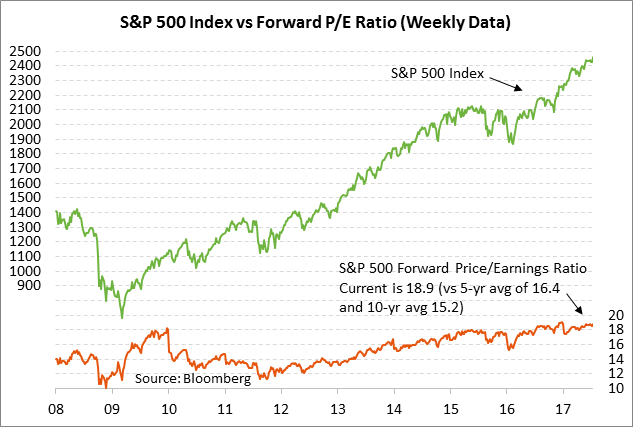

High U.S. stock market valuation means market is vulnerable to any disappointments — Surveys indicate that the majority of market participants believe that the U.S. stock market is overvalued. Nevertheless, the S&P 500 and the Nasdaq 100 this week surged to new record highs. This week’s +0.6% rally in the S&P 500 index pushed the SPX forward P/E ratio (based on expected 2017 earnings) up to 19.0, which is well above the 5-year average of 16.4 and the 10-year average of 15.2. The trailing P/E for the S&P 500 is even higher at 21.8 due in part to relatively weak trailing earnings (i.e., a weak denominator).

Despite high stock market valuations, market participants are nevertheless pushing stock prices even higher, apparently with the idea that global economic growth will continue to improve and that earnings growth will eventually catch up with stock prices. However, the current high level of stock market valuations means that stocks are priced for perfection, which in turn increases the risk of a sharp downside correction on any disappointments.

We look for the stock market to muddle through with a continued mild upside bias based on expectations for strong U.S. earnings growth through 2018. However, there is plenty of fodder for disappointments in this priced-to-perfection market that include the possibility of (1) a more serious turn in the Russia investigation as the Mueller team starts investigating President Trump’s business transactions and funding sources, which Mr. Trump in Wednesday’s NYT interview referred to as “a violation,” (2) deteriorating U.S.-China relations as this week’s U.S.-Chinese dialogue meetings on addressing Mr. Trump’s trade deficit complaints ended with some acrimony, (3) the Fed’s move by the end of the year to start reducing its balance sheet and the Fed’s apparent intent to keep raising interest rates over the next 2-1/2 years, (4) the likelihood that President Trump will appoint a new Fed Chair when Ms. Yellen’s term expires in Feb 2018, which could herald the beginning of a much more hawkish Fed depending on who is chosen as the new Fed chair, (5) the impending end of QE in Europe in 2018 and upward pressure on European interest rates, (6) questions about whether the current renegotiation of NAFTA will negatively affect U.S. trade and supply chains, and (7) the attempt by China to rein in the massive debt growth seen in the past decade without causing the economy to implode.

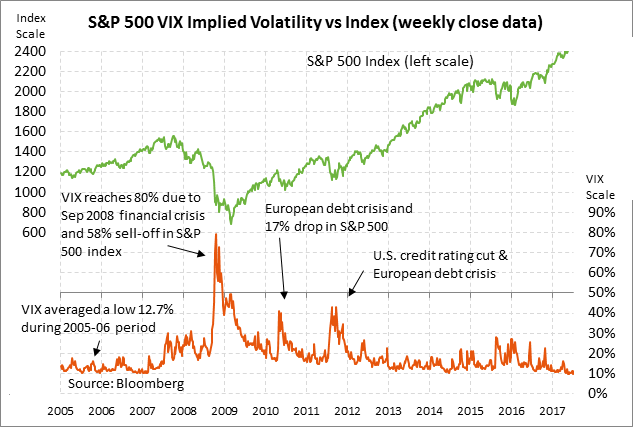

Despite these potential pitfalls, the VIX index (expected 30-day SPX volatility) remains very low. The VIX on Thursday fell to 9.58, just above last Friday’s multi-decade low of 9.51 (on a closing basis). Expected volatility is low, not because there aren’t major factors that could shake up the markets, but because the stock market remains in a bull mode with relatively low realized volatility. However, any negative news for the stock market would obviously spark a big jump in the VIX index from its current remarkably low level.