- U.S. LEI expected to continue chugging along at a solid pace

- U.S. unemployment claims continue to show strong labor market

- 10-year TIPS auction to yield near 0.45%

- ECB’s main job today will be to avoid a further rise in Eurozone bond yields

- BOJ policy expected unchanged

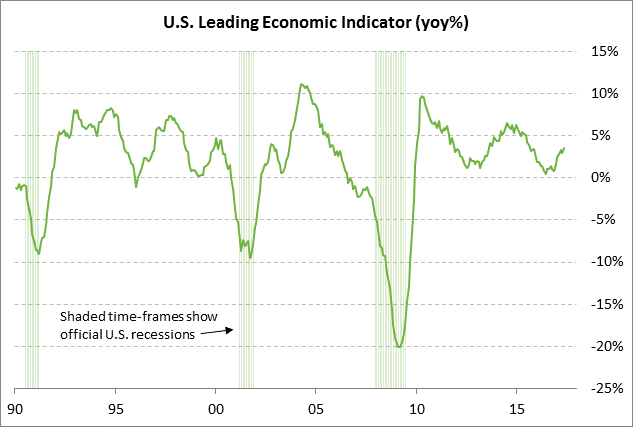

U.S. LEI expected to continue chugging along at a solid pace — The consensus is for today’s June leading indicators report to show an increase of +0.4%, improving slightly from May’s +0.3%. The LEI on a year-on-year basis in May rose to a 1-3/4 year high of +3.5% y/y, which bodes well for near-term U.S. GDP growth.

U.S. GDP dipped to +1.4% in Q1, but the consensus is for next Friday’s Q2 GDP report to improve to +2.6%. The market is then expecting GDP to average near +2.4% in the second half of 2017 and near +2.3% in 2018. The lukewarm GDP growth rate is positive for Fed policy since the economy is growing by enough to support the labor market, but not by enough to cause a surge in inflation, which would force the Fed to quickly raise interest rates.

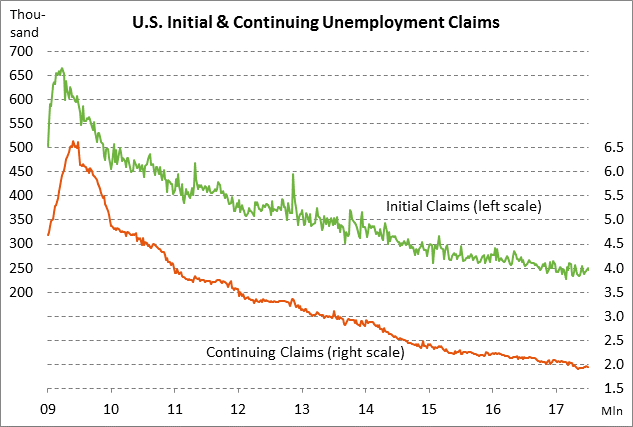

U.S. unemployment claims continue to show strong labor market — The initial and continuing unemployment claims series both remain near decade-plus lows, indicating a strong labor market where businesses are holding on tightly to their current employees. The initial claims series is only +20,000 above the 44-year low of 227,000 posted in February, while the continuing claims series is only +46,000 above its 29-year low of 1.899 million posted in May.

The market consensus is for today’s weekly initial unemployment claims report to show a small decline of -2,000 to 245,000, adding to last week’s -3,000 decline to 247,000. Continuing claims are expected to show a small increase of +5,000 to 1.950 million following last week’s -20,000 decline to 1.945 million. After some shaky payroll data during the spring, the payroll data is again showing solid hiring with a 3-month average monthly increase of +194,000.

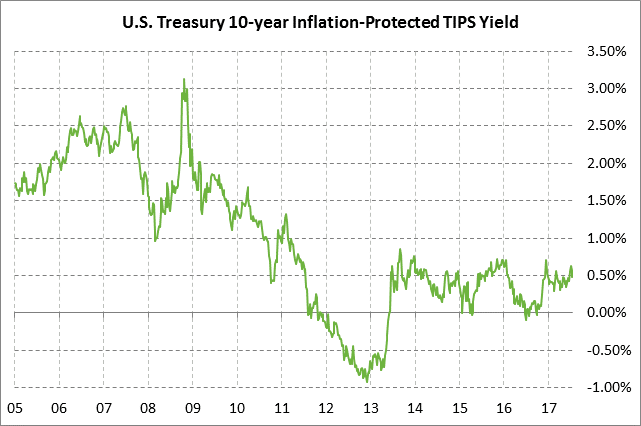

10-year TIPS auction to yield near 0.45% — The Treasury’s sale of $13 billion of 10-year TIPS today will be of a new issue as opposed to a reopening of an existing issue. Today’s 10-year TIPS was trading at 0.45% in when-issued trading late Wednesday afternoon. The benchmark 10-year TIPS posted a 7-month high of 0.64% as recently as July 10 but has since fallen back to 0.48%. The 10-year TIPS is currently trading near the middle of its post-election range and is up by +38 bp from the pre-election level of 0.10% due to expectations for more solid U.S. economic growth and some eventual tax-cut stimulus.

The 12-auction averages for the 10-year TIPS are as follows: 2.36 bid cover ratio, $23 million of non-competitive bids by mostly retail investors, 6.7 bp tail to the median yield, 15.4 bp tail to the low yield, and 52% taken at the high yield. The 10-year TIPS is the most popular coupon security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 68.6% of the last twelve 10-year TIPS auctions, which is well above the average of 60.2% for all recent coupon auctions.

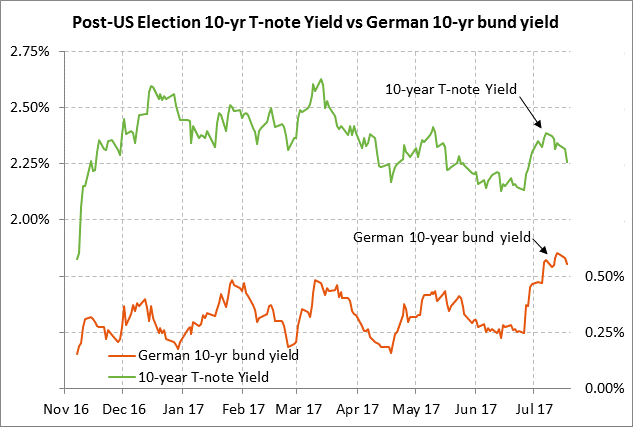

ECB’s main job today will be to avoid a further rise in Eurozone bond yields — The ECB’s main job at its 2-day meeting that concludes today will be to avoid any further rise in Eurozone bond yields. Eurozone bond yields have risen sharply in the past several weeks, tightening financial conditions and causing fresh strength in the euro, which has hurt Eurozone exporters. The 10-year bund yield after ECB President Draghi’s speech in Sintra, Portugal on June 28 surged by 35.8 bp to a 1-1/2 year high of 0.603% on July 12 but has since backed off by -6 bp to 0.542%.

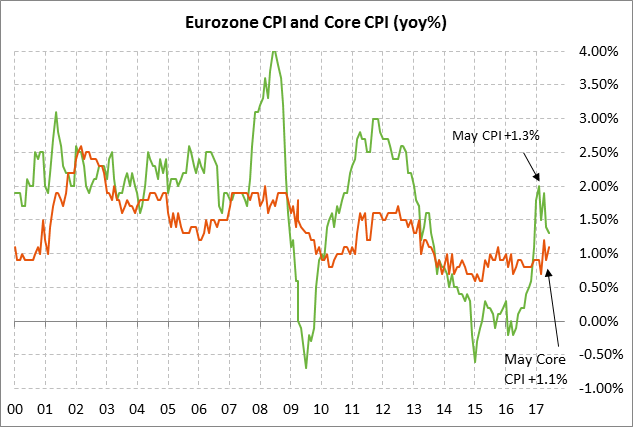

Mr. Draghi in his Sintra speech seemed to be laying the groundwork for the expected QE tapering announcement this September or October. Mr. Draghi said that reflationary forces have replaced deflationary forces and that the parameters of monetary policy could be adjusted as the Eurozone economy continues to improve. The consensus is for Eurozone GDP in 2017 to improve slightly to +1.9% from +1.8% in 2016. Yet the ECB remains concerned about the soft inflation outlook and is in no hurry to force tighter monetary conditions. The Eurozone June CPI of +1.3% y/y (headline) and +1.1% (core) were well below the ECB’s inflation target of just below 2.0%.

In terms of concrete actions, the ECB at today’s meeting will at most tighten its guidance on asset purchases by dropping its promise to increase in QE program in either size or duration if the economic outlook deteriorates. A recent survey by Bloomberg found that about half of the respondents expect the ECB today to drop that QE easing bias.

The Bloomberg survey also found a market consensus that the ECB at its next meeting on Sep 9 will announce an extension of its QE program into 2018, but at a reduced pace that ends the QE program over the first 9 months of 2018. That is more dovish than previous market expectations for tapering of QE over the first 6 months of 2018. The consensus is then for the ECB to raise its refinancing rate by +10 bp in Q4-2018.

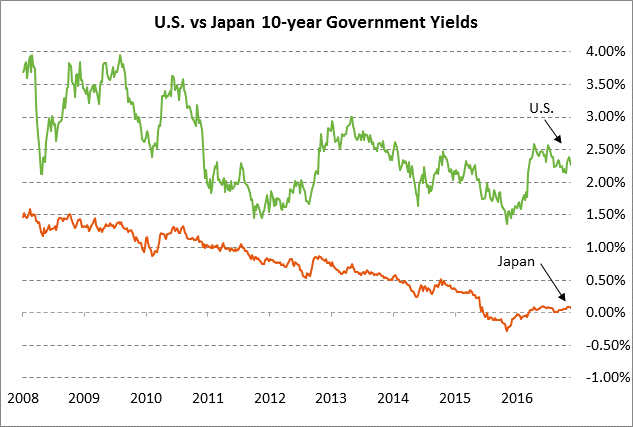

BOJ policy expected unchanged — The unanimous market consensus is that the Bank of Japan at its Wed-Thu policy meeting will leave its policy parameters unchanged with its policy rate at -0.1% and its 10-year JGB target at zero. The BOJ is also expected to reiterate its 80 trillion yen annual QE target even though the BOJ’s recent purchases have fallen somewhat short of that target.

The BOJ recently had to defend the perceived upper 0.1% limit of its JGB target range around zero due to upward pressure on Japanese bond yields caused by the late-June/early-July surge in European and U.S. bond yields. The BOJ on Friday, July 7, announced an unlimited bond purchase at a yield of 0.11%, which was sufficient to scare the market into pushing the yield down to the current level of 0.075%.