- Weekly U.S. market focus

- Senate health bill is delayed

- Fed outlook turns more dovish ahead of next week’s FOMC meeting

- U.S. Q2 earnings season heats up

- T-note yields fall back on easier Fed policy outlook

- SPX rallies to new record high on dovish Fed

Weekly U.S. market focus — The U.S. markets this week will focus on (1) anticipation of next week’s FOMC meeting, (2) this week’s relatively light U.S. economic schedule, (3) any progress on the Senate Republican’s health bill, the final passage of which in Congress could pave the way for a larger U.S. corporate tax cut, (4) the first big week for Q2 earnings reports with a focus on Wall Street banks, (5) the Treasury’s sale of $13 billion of 10-year TIPS on Thursday, and (6) whether oil prices can extend the recovery rally seen in the past three weeks.

In overseas news this week, the focus will mainly be on Thursday’s ECB meeting. The ECB is not expected to announce a 2018 QE tapering until its next meeting on Sep 7. The ECB this week may try to sound dovish to curb the mini taper tantrum seen in the past three weeks that has driven the 10-year German bund yield +35 bp higher to a 1-1/2 year high of 0.60%. The Bank of Japan at its Wed-Thu meeting is expected to leave its monetary policy unchanged.

In China, the markets on Monday will react to Sunday night’s Chinese economic data, which included Q2 GDP (expected +6.8%) and June industrial production and retail sales. In addition, a high-level Chinese government meeting over the weekend on financial regulation resulted in a new cabinet-level committee to coordinate financial oversight. The markets will be waiting to see if that meeting produces a step-up in the government’s financial supervision and deleveraging campaign.

Senate health bill is delayed — Congress now has only two weeks left before it is due to leave Washington for the August recess, although the Senate may have more time since Senate Majority Leader McConnell has said he plans to delay the Senate’s recess by two weeks. The Republican’s health insurance bill faced a setback over the weekend when Mr. McConnell announced that he would delay this week’s planned vote on health insurance until Republican Senator McCain can return to Washington. Mr. McCain last Friday had surgery to remove a blood clot from above his eye and he is resting at his home in Arizona. Meanwhile, the Senate Budget Committee on Sunday said that the CBO score on the Republican’s latest health insurance bill will not be released on Monday as expected. No release date or reason for the delay was given. The Trump administration this week is pushing a theme of “Buy American” but the Russian investigation and news cycle will continue.

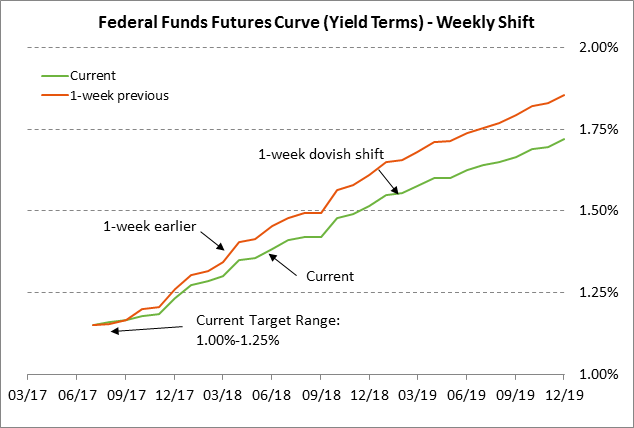

Fed outlook turns more dovish ahead of next week’s FOMC meeting — The outlook for Fed policy turned more dovish last week after Fed Chair Yellen in her Congressional testimony expressed some uncertainty about the inflation outlook. There were also some dovish inflation comments by other Fed officials. Dallas Fed President Kaplan (voter) said last Friday, for example, that he wants to see evidence of progress towards the Fed’s 2.0% inflation target before he would vote to raise interest rates another notch.

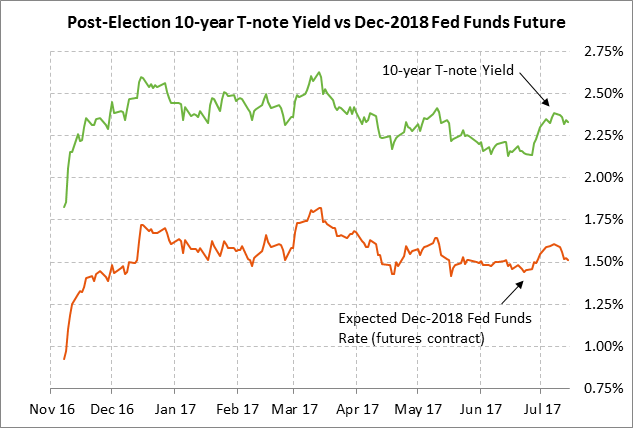

The federal funds futures curve last week turned more dovish by -3 bp for the end of 2017, -9 bp for the end of 2018, and -14 bp for the end of 2019. The market is discounting the odds at only 14% for a rate hike at next week’s FOMC meeting. The odds then rise to +22% by the Sep 19-20 meeting, 24% by the Oct 31/Nov 1 meeting, and 60% by the Dec 12-13 meeting. We expect the FOMC to announce an Oct 1 start date for its balance sheet program at either next week’s FOMC meeting or, more likely, at the following meeting on Sep 19-20.

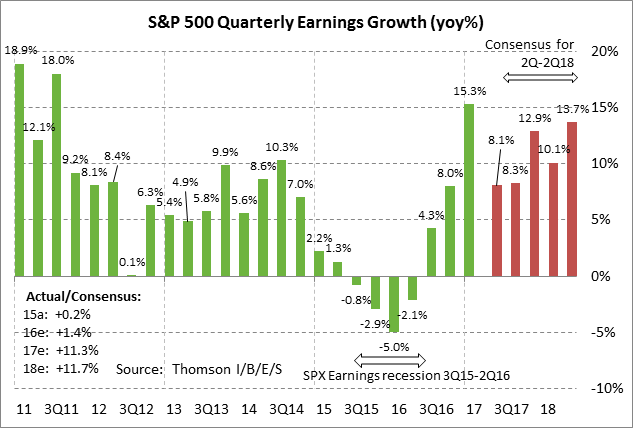

U.S. Q2 earnings season heats up — The Q2 earnings season kicks into a higher gear this week with 70 of the S&P 500 companies scheduled to report. The market consensus for Q2 SPX earnings growth is +8.1% y/y (+5.2% ex-energy), according to Thomson Reuters I/B/E/S. Q2 earnings reports have been positive thus far with 80.0% of reporting companies beating expectations, well above the long-term average of 64% and the 4-quarter average of 71%.

Looking ahead, the market consensus is for SPX earnings growth of +8.3% in Q3, +12.9% in Q4, +10.1% in Q1-2018, and +13.7% in Q2-2018. On a calendar year basis, the consensus is for SPX earnings growth of +11.1% in 2017 and +11.6% in 2018.

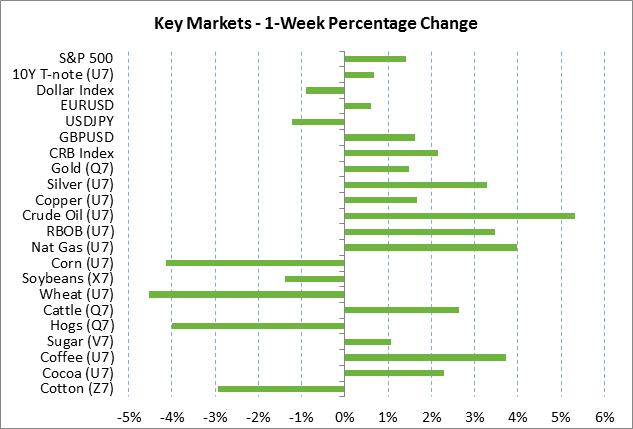

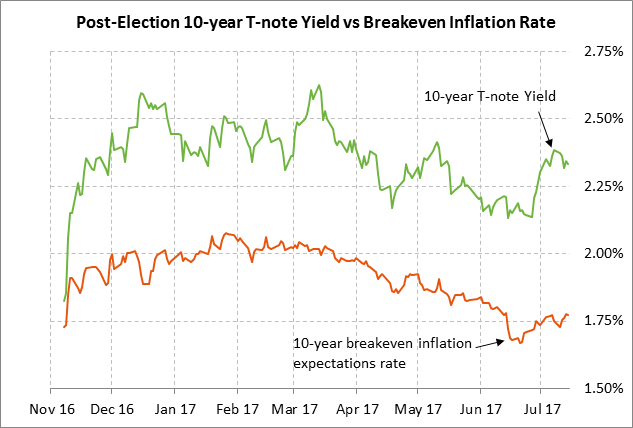

T-note yields fall back on easier Fed policy outlook — The 10-year T-note yield last week fell from the early-July 1-month high of 2.394% to post a new 2-week low and close the week down -5.4 bp at 2.332%. The 10-year yield last week fell mainly because of reduced expectations for Fed rate hikes with the Dec 2018 federal funds futures contract closing the week down -5 bp, the same weekly decline as the 10-year yield. Inflation expectations were a slightly bearish factor last week with a +2.0 bp rise in the 10-year breakeven rate tied to last week’s +5.2% rally in Aug crude oil prices. The T-note yield is still up sharply by a net +19.5 bp in the past three weeks mainly because of the +35 bp surge in the German bund yield on expectations for an ECB QE tapering announcement by September.

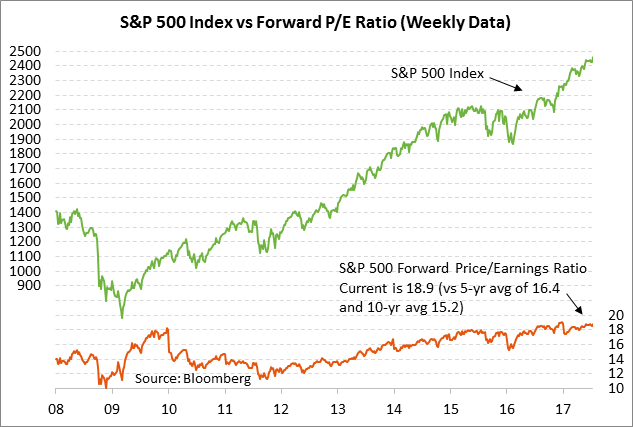

SPX rallies to new record high on dovish Fed — The S&P 500 index last Friday rallied sharply to a new record high and closed the week up +1.41%. Stocks were boosted by the more dovish view of Fed policy and by expectations for a strong Q2 earning season. The stock market also continues to see support from expectations for solid U.S. and global economic growth and from the sharp -6.9% year-to-date decline in the dollar index to a new 10-month low. The stock market is carefully watching the White House-Russian news. Stretched valuations did not prevent last Friday’s new record. The SPX forward P/E earnings ratio of 18.9, is well above the 5-year avg of 16.4 and 10-year avg of 15.2.