PM

- Will Yellen provide hints on timing of balance sheet program or next rate hike?

- Fed Beige Book

- 10-year T-note auction to yield near 2.36%

- EIA report

Will Yellen provide hints on timing of balance sheet program or next rate hike? — Fed Chair Yellen will testify today in her semi-annual hearings before the House Financial Services Committee. The main question is whether Ms. Yellen will provide any hints about when the Fed will raise interest rates another notch or when the Fed will announce and begin its balance sheet reduction program.

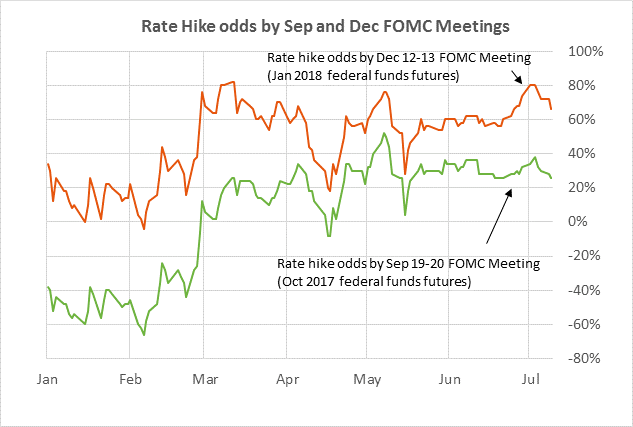

The markets are currently discounting the odds for the Fed’s next rate hike at 12% for the upcoming July 25-26 meeting, 26% for the Sep 19-20 meeting, 28% by the Oct 31/Nov 1 meeting, and 66% by the Dec 12-13 meeting, based on federal funds futures market.

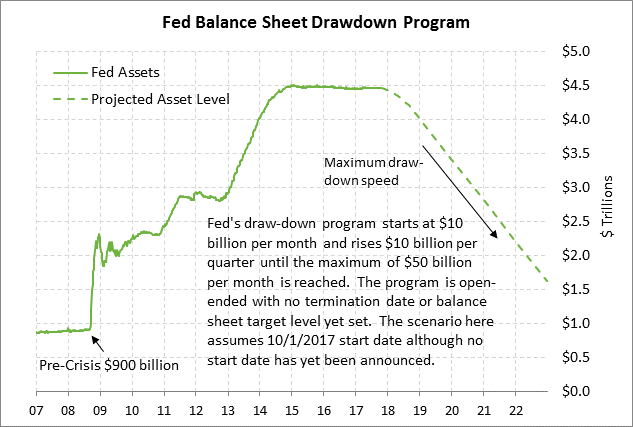

The Fed has so far only said that it plans to begin its balance sheet reduction program “later this year.” We believe the Fed is anxious to get its balance sheet program in place before President Trump makes his announcement later this year on who will be the next Fed Chair when Ms. Yellen’s term expires in February 2018. We suspect the Fed will announce the balance sheet start-date at either its next meeting on July 19-20 or more likely at the Sep 19-20 meeting when Ms. Yellen is scheduled to give a post-meeting press conference. We suspect the Fed will start the program on October 1 in order to make the program concurrent with calendar quarters. One caveat to an October 1 start is that Congress may be in the throes of a government shutdown and/or an impending debt ceiling crisis.

The Fed has already announced that its balance sheet reduction program will start with an overall cap of $10 billion per month, with a cap of $6 billion for Treasury securities and $4 billion for mortgage-backed securities. The cap will then rise by $10 billion every three months until it reaches the maximum of $50 billion per month. The cap will only constrain the roll-off in the first year of the program. After the first year, the amount of maturing securities in the Fed’s portfolio will be less than the Fed’s cap.

The Fed does not plan to announce the ultimate target level for its balance sheet until after it decides on its long-term policy framework. If the Fed decides on a floor system, such as the one it is using now, then the Fed will need a larger balance sheet, whereas the alternative corridor system would allow a smaller balance sheet. Former Fed Chair Bernanke has mentioned an ultimate balance sheet level of $2.5 trillion, which is substantially larger than the pre-crisis $900 billion level simply because the U.S. economy is now larger and the Fed’s liabilities such as currency in circulation are larger.

The markets will also be listening very carefully for Ms. Yellen’s latest take on the inflation outlook. Ms. Yellen has so far brushed off the decline in the inflation statistics in the past several months as the result of idiosyncratic factors such as lower prices for cell phone services and prescription drugs. Ms. Yellen has expressed confidence that inflation over the medium-term will rise to the Fed’s 2.0% target, mainly because of reduced slack in the U.S. economy and her expectation for rising wages. However, other Fed officials are more concerned about the inflation outlook and may be willing to consider slowing down the Fed’s tightening pace until it becomes clear whether inflation will in fact start moving back up to the Fed’s 2.0% target.

The markets also want to see if Ms. Yellen has any new comments about whether the U.S. stock market is overvalued and whether the Fed is concerned enough about financial risk to add it to its list of reasons for raising interest rates. Ms. Yellen recently said that some asset prices had become “somewhat rich.” The Fed has been a bit perturbed that despite the +75 bp Fed rate hike since December, bond yields have dropped and the stock market has rallied sharply. The Fed could interpret that as sign the markets are not taking it seriously and that the Fed’s rate hikes are not yet biting.

Fed Beige Book — The Fed today will release its Beige Book report on the regional U.S. economy in preparation for the July 25-26 FOMC meeting in two weeks. The last Beige Book, released on May 31, said that most of the 12 Fed districts reported that their economies “continued to expand at a modest or moderate pace from early April through late May.” The report also said, “Labor markets continued to tighten, with most Districts citing shortages across a broadening range of occupations and regions.”

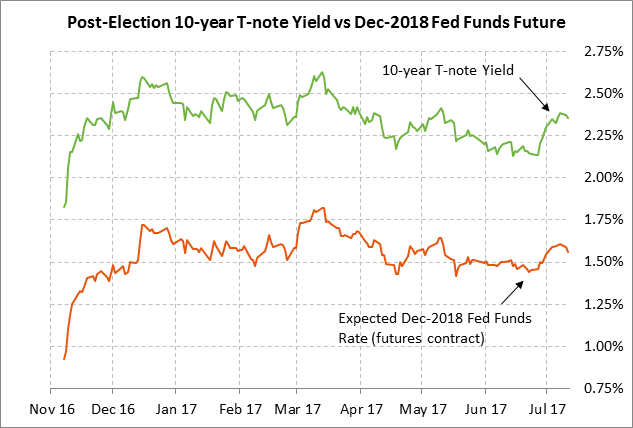

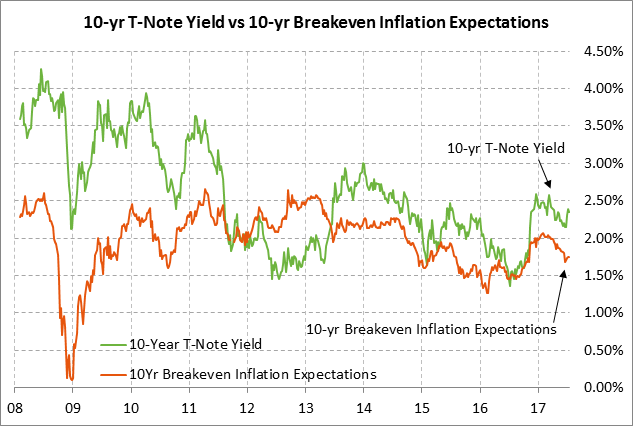

10-year T-note auction to yield near 2.36% — The Treasury today will sell $20 billion of 10-year T-notes in the second and final reopening of May’s 2-3/8% 10-year T-note of May 2027. The Treasury will then conclude this week’s $56 billion coupon package by selling $12 billion of 30-year bonds on Thursday.

Today’s 10-year T-note issue was trading at 2.36% in when-issued trading late Tuesday afternoon. That translates to an inflation-adjusted yield of 0.61% against the current 10-year breakeven inflation expectations rate of 1.75%. The 12-auction averages for the 10-year are as follows: 2.43 bid cover ratio, $16 million in non-competitive bids to mostly retail investors, 5.5 bp tail to the median yield, 14.7 bp tail to the low yield, and 36% taken at the high yield. The 10-year is moderately popular among foreign investors and central banks. Indirect bidders, a proxy for foreign bidders, have taken an average of 62.9% of the last twelve 10-year T-note auctions, which is moderately above the average of 60.2% for all recent coupon auctions.

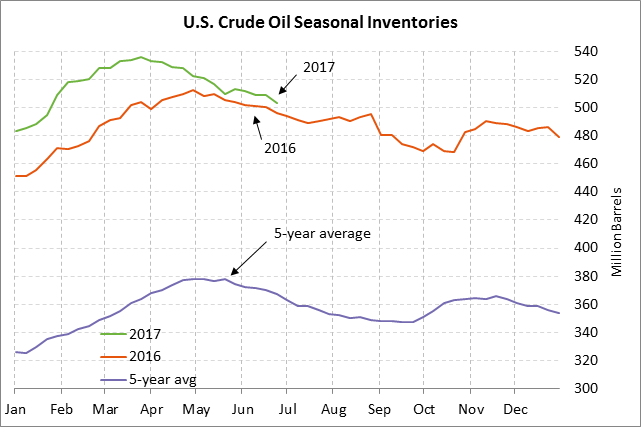

EIA report — The market consensus for today’s weekly EIA report is for a -2.7 million bbl decline in crude oil inventories, a -1.6 million bbl decline in gasoline inventories, a +900,000 bbl rise in distillate inventories, and a +0.5 point increase in the refinery utilization rate to 94.1%.