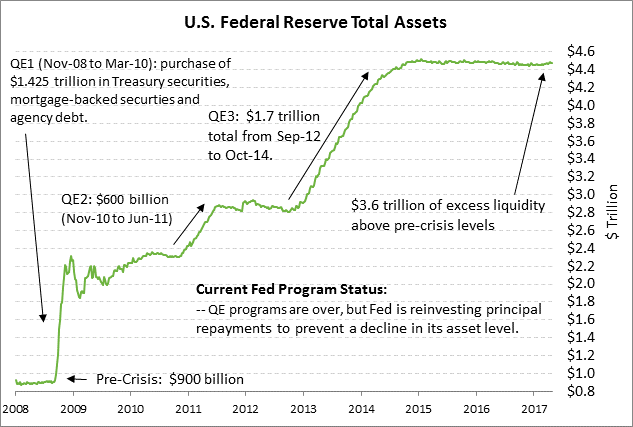

- Fed will be very cautious on balance sheet disclosures to avoid a new taper tantrum as May 2-3 minutes are released today

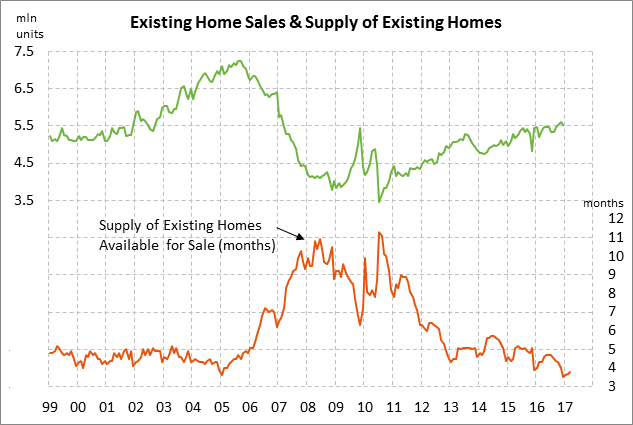

- U.S. April existing home sales expected to back off from 10-year high

- FHFA U.S. home prices expected to see continued squeeze

- 5-year T-note auction to yield near 1.83%

- Weekly EIA report

Fed will be very cautious on balance sheet disclosures to avoid a new taper tantrum as May 2-3 minutes are released today — The markets are waiting to see if today’s minutes from the May 2-3 FOMC meeting provide any information about the Fed’s balance sheet discussions. The FOMC has so far only said it plans to shift its balance sheet reinvestment policy “by later this year.”

The Fed is still in the early stages of its balance sheet discussions and has not provided any details about how fast it will draw down its balance sheet or its eventual balance-sheet target level. The market consensus is that the FOMC will officially announce its balance sheet policy change at its September meeting with the actual draw-down beginning late this year or on January 1. Ms. Yellen would presumably like to have a new balance sheet policy in place before President Trump decides later this year about whether to replace her as Fed Chair when her term expires in Feb 2018.

The markets have not expressed any particular concern thus far about the Fed’s balance sheet draw-down. However, that could change as the date approaches for when the Fed steps aside as a big buyer of Treasury securities to replace maturing securities and starts draining excess reserves from the banking system. The Fed is treading very carefully on its balance sheet communications to avoid another taper tantrum episode. In the taper tantrum episode in 2013, the 10-year T-note yield rose sharply by +60 bp in just 6 weeks after then-Fed Chair Bernanke hinted at the end of QE3. The dollar index soared by 5% in just three weeks.

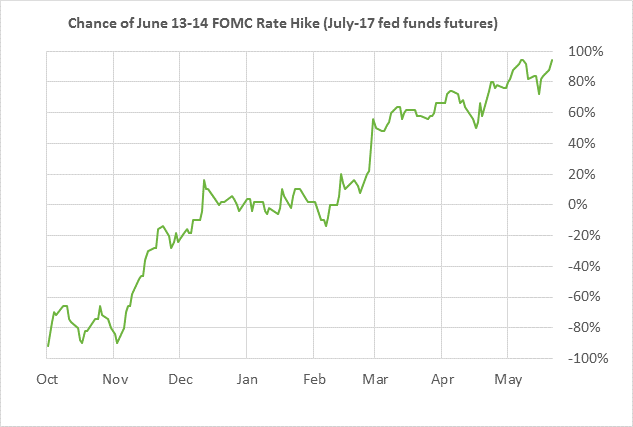

Regarding interest rates, the federal funds futures market is currently discounting the chances for a Fed rate hike at its next meeting on June 13-14 at about 90%. The odds for a June rate hike rose slightly to 80% from 76% after the May 2-3 FOMC meeting when the post-meeting statement said that the Fed viewed the Q1 GDP weakness as transitory and that the fundamentals for consumer spending remained “solid.” The rate-hike odds have since risen to 90% due to the recent improvement in the U.S. economic data and this week’s recovery in stocks.

U.S. April existing home sales expected to back off from 10-year high — The consensus is for today’s April existing home sales report to show a small -1.1% decline to 5.65 million, giving back a little of March’s solid +4.4% gain to a 10-year high of 5.71 million. Tuesday’s April new home sales report showed a large decline of -11.4% to 569,000 units, which set a negative backdrop for today’s existing home sales report. The SPDR S&P Homebuilders ETF (XHB) on Tuesday fell by -0.69% due to the weak new home sales report, but is still up by +11% year-to-date on longer-term housing market optimism.

U.S. existing home sales in March were very strong even though there were few homes available for sale. There were only 3.8 months worth of existing homes available for sale in March, which was just above December’s record low of 3.5 months and far below the long-term average of 7.0 months. Home sales are being boosted by strong consumer confidence, improved household balance sheets, and pent-up demand in the aftermath of the Great Recession.

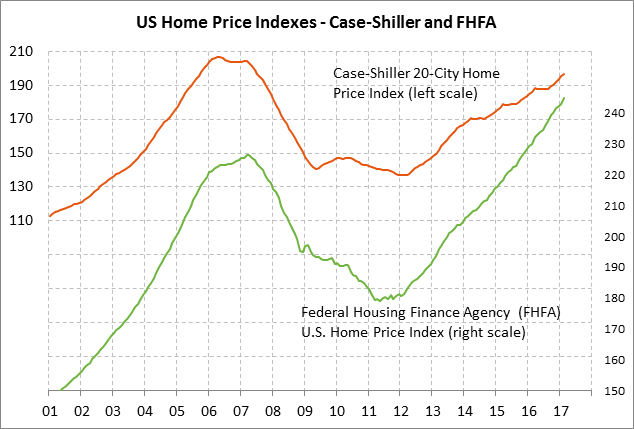

FHFA U.S. home prices expected to see continued squeeze — The consensus is for today’s March FHFA U.S. house price index to show a solid gain of +0.5% m/m, adding to February’s sharp gain of +0.8%. The FHFA index in February was up sharply by +6.4% y/y and by +36.5% from the housing-bust low seen in March 2011.

U.S. home prices have recently accelerated higher due to the combination of strong demand and tight supplies. Strong demand is seen by the fact that U.S. existing home sales reached a 10-year high in March. Meanwhile, tight supplies are illustrated by the fact that the current 3.5-month supply of homes on the market is far below the 7-8 month level that the National Association of Realtors says is consistent with steady home prices.

High home prices have yet to pose much deterrence to potential home buyers. The historically low level of mortgage rates continues to keep homes affordable because of low mortgage payments even as home prices rise. The current 30-year mortgage rate of 4.02% is up by +48 bp since the November 2016 election, but is still far below the average of about 6% seen in the 2003-08 period and levels above 8% seen prior to 2000.

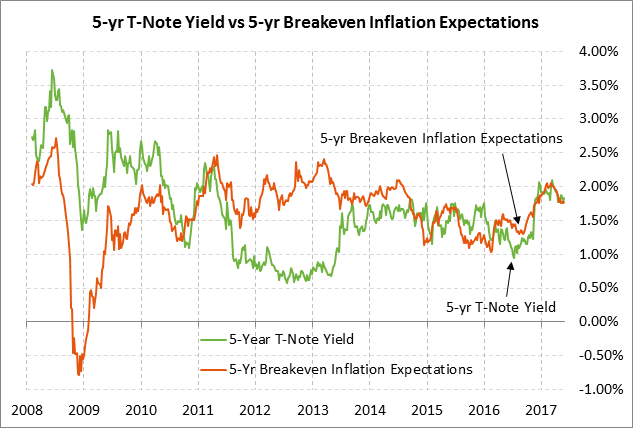

5-year T-note auction to yield near 1.83% — The Treasury today will sell $13 billion of 2-year floating rate notes and $34 billion of 5-year T-notes. The Treasury will then conclude this week’s $101 billion T-note package by selling $28 billion of 7-year T-notes on Thursday. Today’s 5-year T-note issue was trading at 1.83% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of a slightly positive 0.05% against the current 5-year breakeven inflation expectations rate of 1.78%.

The 12-auction averages for the 5-year are as follows: 2.43 bid cover ratio, $43 million in non-competitive bids, 5.1 bp tail to median yield, 12.9 bp tail to the low yield, and 46% taken at the high yield. The 5-year is moderately popular among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.2% of the last twelve 5-year auctions, which is moderately above the average of 59.9% of all recent Treasury coupon auctions.

Weekly EIA report — The market consensus for today’s weekly EIA report is for a -2.0 million bbl decline in U.S. crude oil inventories, a -750,000 bbl decline in gasoline inventories, a -1 million bbl decline in distillate inventories, and an unchanged refinery utilization rate of 93.4%.