- Markets take a heavy hit from double-barreled threat of trade tensions and Italy

- Italy’s upcoming election will effectively be a referendum on the euro

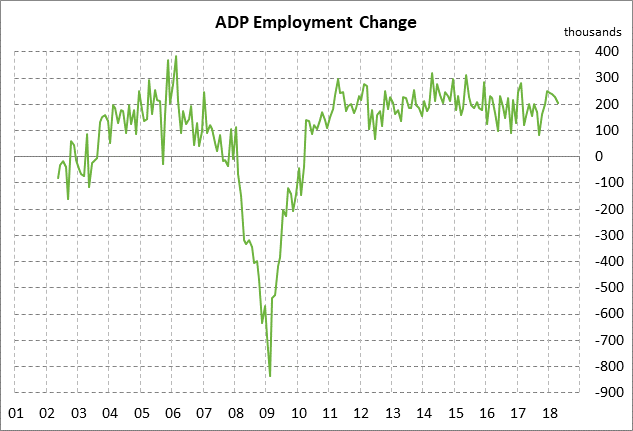

- ADP expected to show firm U.S. labor market

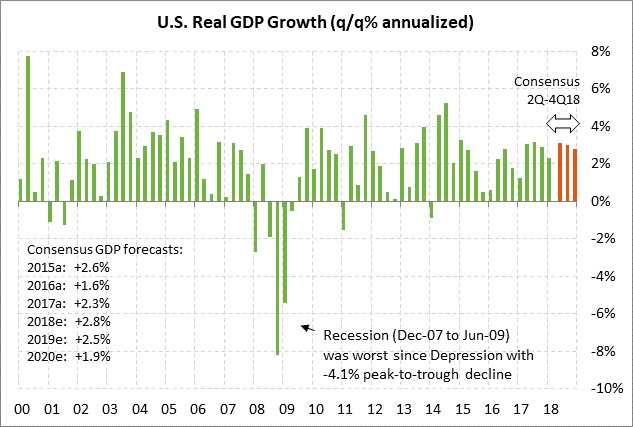

- Q1 U.S. GDP expected unrevised

Markets take a heavy hit from double-barreled threat of trade tensions and Italy — Global stocks on Tuesday took a heavy hit on the combination of renewed trade tensions and Italy’s threat to Eurozone stability. The U.S.-Chinese trade war was “on hold” for only two weeks until the Trump administration yesterday announced that it will release a final list of the $50 billion worth of Chinese products subject to a 25% tariff on June 15 and that those tariffs will be implemented “shortly thereafter.”

Yesterday’s announcement may have only been a negotiating ploy to try to soften up China ahead of U.S. Commerce Secretary Wilbur Ross’s visit to China this Saturday for a new round of negotiations. However, the announcement is more likely a sign that the negotiations are not going well. In any case, the markets now have a more tangible date to worry about since the U.S. tariff on $50 billion worth of Chinese goods could go into effect in as little as 3 weeks. The Trump administration on Tuesday also said that it will release its proposed investment restrictions and exports controls on China by June 30.

If the U.S. goes ahead with its 25% tariff on $50 billion of Chinese goods, then China will almost certainly retaliate with an equal tariff on the $50 billion worth of U.S. products that China has already identified. At that point, President Trump may go ahead with his threat of tariffs on another $100 billion of Chinese products.

Even before yesterday’s U.S.-Chinese trade announcement, trade tensions were already running high since Europe’s temporary exemption from steel-aluminum tariffs expires this Friday (June 1). If the Trump administration does not grant another extension and instead puts those tariffs into effect, then Europe has already prepared the list of $3.3 billion worth of U.S. products that will be hit with a retaliatory tariff.

Italy’s upcoming election will effectively be a referendum on the euro — Italy is headed for new elections, likely in July or August. President Mattarella’s plan to install former IMF official Cottareli as a caretaker premier seems doomed to failure with all the major parties now pushing for near-term elections.

The big question now is how the parties will fare in a new election. If the populists improve their vote count over the March 4 election, then the populists will essentially have a mandate to be as tough on the Eurozone as they wish to be, even including having economist and arch-Euroskeptic Paolo Savona as their finance minister. Italy’s Democrats on Tuesday charged that Five Star and the League have a secret plan to force Italy out of the Eurozone, possibly based on Mr. Savano’s “Plan B” that he published in 2015. The fear is that if an Italian financial and banking crisis gets bad enough, then Italy could be forced out of the Eurozone even without a voter referendum.

According to a recent SWG poll conducted on May 23-28, the League could benefit the most from new elections since its support is at 27.5%, up sharply by about 10 points from 17.4% in the elections. Five Star’s support fell slightly to 29.5% from 32.7%. Berlusconi’s Forza Italia is in bad shape with a drop to 8% from 14%. The Democratic Party rose slightly to 19.4% from 18.7%. The latest polls therefore indicate combined support of 57% for the populist Five Star and League parties, up from just over 50% in the March election.

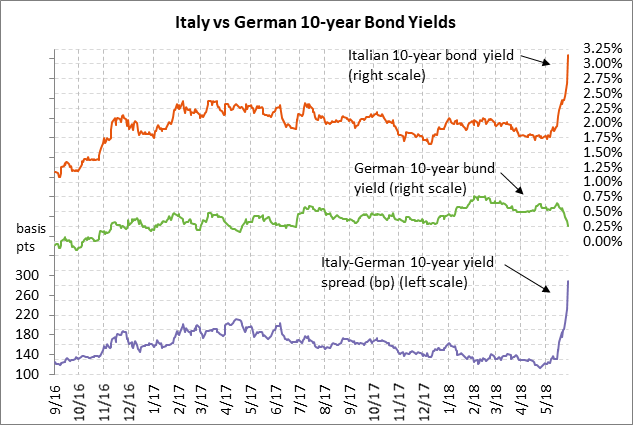

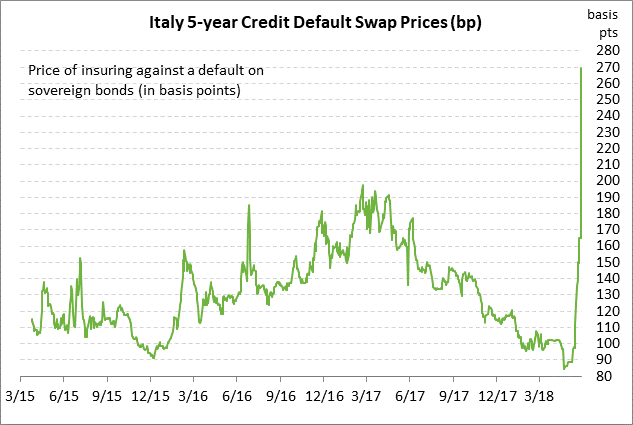

The Italian 10-year bond yield on Tuesday rose by an extraordinary +48 bp to a 4-year high of 3.15%. The 10-year Italy-German bond yield spread soared by +57 bp to a 3-3/4 year high of 290 bp. The 5-year Italian credit default swap, which is the cost of insuring against an Italian sovereign bond default, soared by an extraordinary +104 bp on Tuesday to a 4-3/4 year high of 269 bp, returning to 2013 levels. The iShares Italy stock ETF on Tuesday plunged by -5.8% to an 11-month low, adding to the -10% plunge seen in the last three weeks.

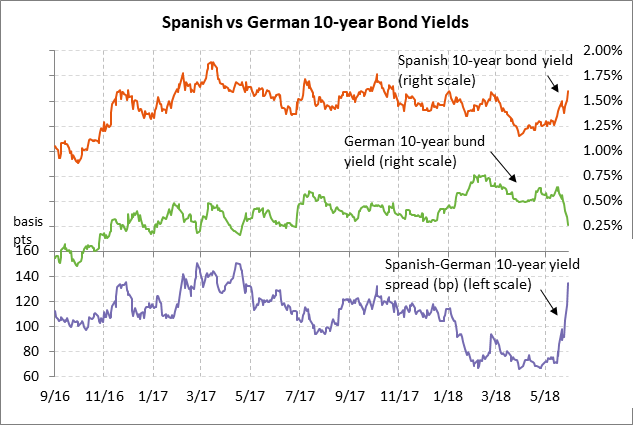

Meanwhile, political uncertainty is running high in Spain ahead of Friday’s expected no-confidence vote against Prime Minister Rajoy’s minority government. However, Mr. Rajoy may be able to hold on to his job for at least a while because the opposition may not be sufficiently united about bringing down his government at this particular time. Moreover, even if there is a new government, it will involve establishment politicians and not an insurgent populist movement such as the populist takeover being seen in Italy. The Spanish-German 10-year yield spread on Tuesday rose by +18 bp to a new 1-year high of 136 bp.

ADP expected to show firm U.S. labor market — The market consensus is for today’s May ADP employment report to show an increase of +190,000, which would be down from April’s +204,000 report but very close to the 12-month trend average of +187,000. The market is mainly looking ahead to Friday’s May payroll report, which is expected to show an increase of +190,000, improving from weak reports of +135,000 in March and +164,000 in April.

U.S. GDP expected unrevised — The market consensus is for today’s Q1 GDP to be left unrevised at +2.3% (q/q annualized). Q1 personal consumption is expected to be revised slightly higher to +1.2% from +1.1%. Looking ahead, the market consensus is for GDP in Q2 to improve substantially to +3.1% as consumer spending recovers and as Q1’s residual seasonal weakness dissipates. On an annual basis, the consensus is for U.S. GDP in 2018 to strengthen to +2.8% from +2.3% in 2017 due largely to the Jan 1 tax cut, which increased consumer buying power and should boost business investment. GDP is then expected to ease mildly to +2.5% in 2019 as fiscal stimulus fades and as higher interest rates take their toll on the economy.