- FOMC minutes may give hints on the odds for a fourth rate hike this year

- U.S. new home sales expected to remain strong

- U.S. business confidence expected to remain strong

- Heavy Treasury supply continues with today’s 5-year T-note auction

- Weekly EIA report

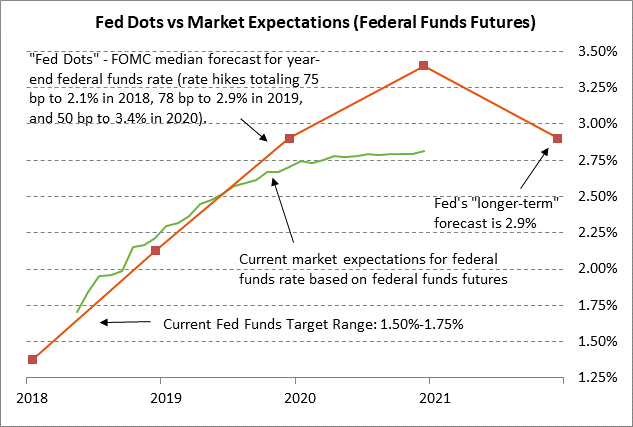

FOMC minutes may give hints on the odds for a fourth rate hike this year — Today’s release of the minutes of the May 1-2 FOMC meeting may give the markets a better idea of whether the Fed ends up raising rates this year four times, which would be one more rate hike than the three hikes forecast by the Fed dots.

The market is currently discounting the odds at 100% that the FOMC at its next meeting on June 12-13 will raise rates for the second time this year to 1.75%-2.00%. The market is expecting the FOMC to leave rates unchanged at the following meeting on July 31-Aug 1, but the market is after that is discounting a 100% chance for a rate hike at the meeting on Sep 25-26. The market is discounting the odds at about 70% for a fourth rate hike at the FOMC’s last meeting of the year on Dec 18-19.

The market is therefore assigning a fairly strong 70% chance that the FOMC will be end up raising rates four times this year, implementing a rate hike at every other meeting (i.e., meetings that have press conferences). Four rate hikes would leave the funds rate target at 2.25%-2.50% by December, i.e., at a mildly positive inflation-adjusted level relative to the Fed’s inflation target of 2.0%. Once the FOMC has done away with a negative real funds rate, then it can move more slowly on raising rates in 2019.

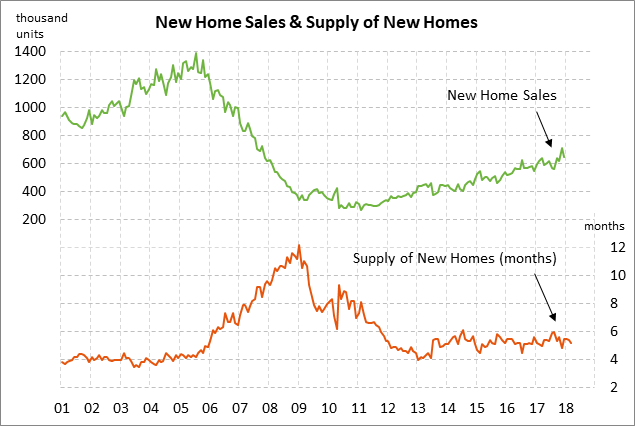

U.S. new home sales expected to remain strong — The market consensus is for today’s April new home sales report to show a -2.2% decline to 679,000, reversing part of March’s +4.0% increase to 694,000. New home sales remain in very strong sharp at only -2.4% below the 10-1/4 year high of 711,000 units posted in Nov 2017. U.S. home builders are bullish on building new homes due to strong demand, tight supplies, and high prices.

However, rising mortgage rates pose at least a mildly negative factor for the housing market. The 30-year mortgage rate last week rose to a 7-year high of 4.61% and has now risen by a total of 80 bp since last September.

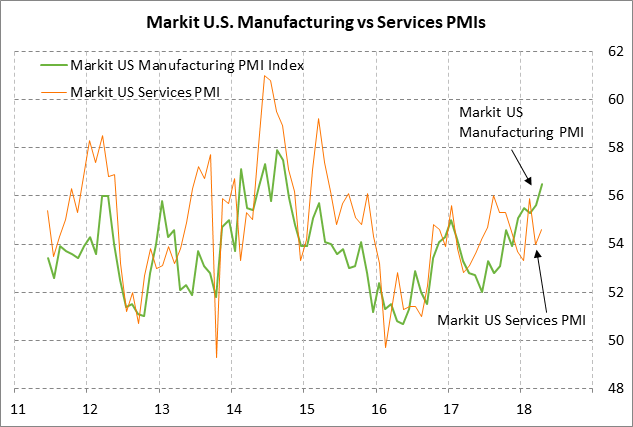

U.S. business confidence expected to remain strong — U.S. business confidence is expected to remain in relatively good shape in today’s PMI reports. U.S. business confidence is being supported by (1) the Jan 1 tax cuts, and (2) the solid U.S. economy. Negative factors include (1) trade tensions and concern about tariffs, (2) the recent rally in the dollar to a 5-month year high, (3) higher gasoline prices, and (4) higher commodity input prices.

The market consensus is for today’s May Markit U.S. manufacturing PMI to be unchanged from April’s 3-1/2 year high of 56.5. Meanwhile, the consensus is for today’s May Markit U.S. services PMI to show a +0.4 point increase to 55.0, adding to April’s +0.6 point increase to 54.6. The April services PMI level of 54.6 was only 1.4 points below the 2-1/2 year high of 56.0 posted last summer.

Heavy Treasury supply continues with today’s 5-year T-note auction — The Treasury today will sell $16 billion of 2-year floating rate notes and $36 billion of 5-year T-notes. The Treasury will then conclude this week’s $115 billion T-note package by selling $30 billion of 7-year T-notes on Thursday.

The $36 billion size of today’s 5-year T-note is up by $2 billion from the $34 billion size that prevailed during most of 2016-17. The Treasury has increased the size of its auctions to finance the larger U.S. budget deficit that has resulted from higher government spending and the Jan 1 tax cuts.

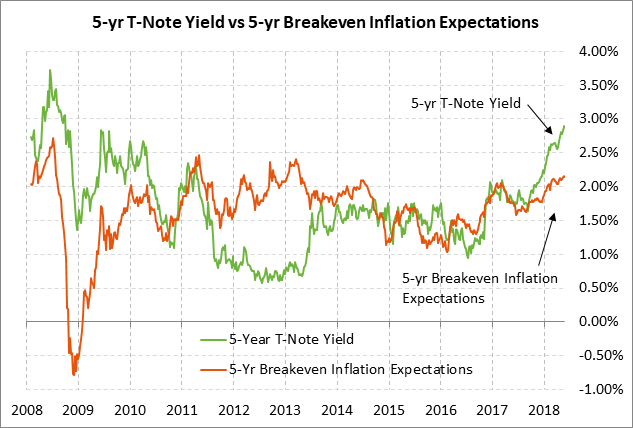

Today’s 5-year T-note issue was trading at 2.90% in when-issued trading late yesterday afternoon, which translates to an inflation-adjusted yield of 0.74% against the current 5-year breakeven inflation expectations rate of 2.16%. The benchmark 5-year T-note yesterday closed at 2.91%, which was just 4 bp below last Thursday’s 9-year high of 2.95%. The 5-year T-note yield has soared by about 130 bp since last September due to the passage of the massive Jan 1 tax cut combined with increased inflation expectations and expectations for more-aggressive Fed rate hikes over the next several years.

The 12-auction averages for the 5-year are as follows: 2.49 bid cover ratio, $60 million in non-competitive bids, 4.4 bp tail to the median yield, 21.7 bp tail to the low yield, and 39% taken at the high yield. The 5-year is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 64.6% of the last twelve 5-year T-note auctions, which matches the median for all recent Treasury coupon auctions.

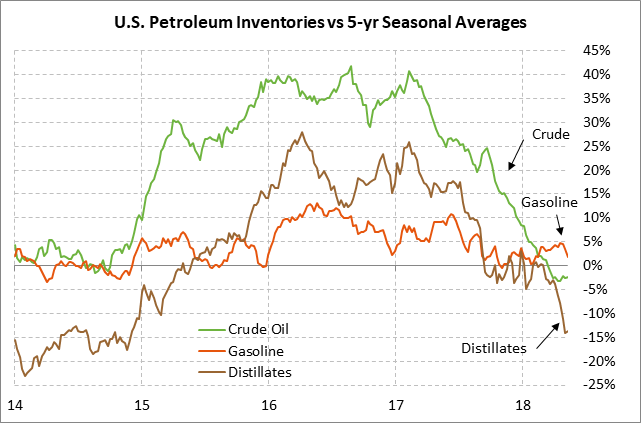

Weekly EIA report — The market consensus for today’s weekly EIA report is for a -2.1 million bbl decline in U.S. crude oil inventories, a -1.5 million bbl decline in gasoline inventories, and a -1.0 million bbl decline in distillate inventories.

U.S. crude oil inventories have fallen since early 2017 and are currently -2.4% below the 5-year seasonal average, which is nearly as tight as April’s 9-1/2 year low of -3.3%. U.S. oil inventories have dropped due to strong domestic demand combined with the sharp +1.8 million bpd jump in U.S. crude oil exports that has been seen since early 2017. Meanwhile, gasoline inventories are ample at 1.9% above their 5-year seasonal average. By contrast, distillate inventories are very tight at -13.6% below average.

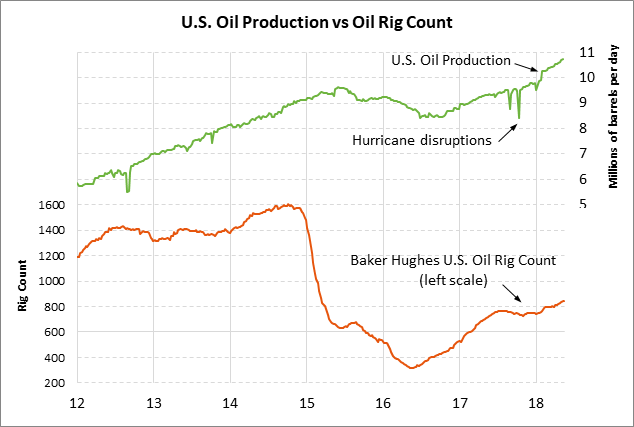

U.S. crude oil production in last week’s EIA report rose to a new record high of 10.723 million bpd, which is up by +15.2% y/y. U.S. oil production is running into bottlenecks in some areas, but production is likely to continue rising sharply as high oil prices allow U.S. oil producers to hedge their production and lock in a profit.