- Weekly global market focus

- U.S. and China agree on “framework” for trade talks and to put trade war on hold

- Italian populists are about to govern as bond risk measures surge

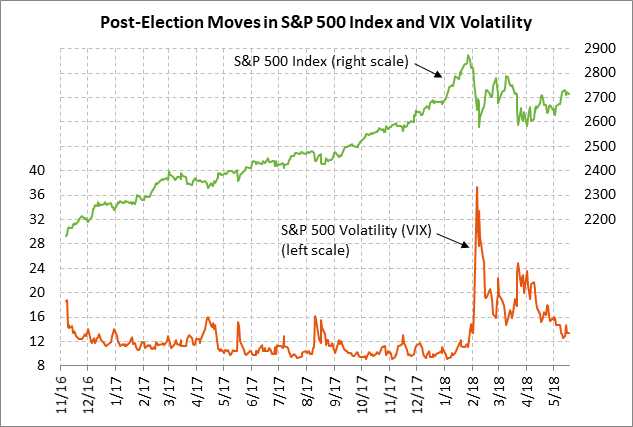

Weekly global market focus — The U.S. markets this week will focus on (1) reaction to the weekend news that the U.S. and China have put their trade war “on hold,” (2) crude oil prices which remain focused on Iranian sanctions and on the outcome of yesterday’s sham presidential election in Venezuela, which could produce new U.S. sanctions, potentially even on crude oil exports, (3) a busy week for Fedspeak capped by comments by Fed Chair Powell on Friday, (4) the ability of the Treasury market to absorb this week’s sale of $115 billion of T-notes, (5) a modest earnings calendar with 22 of the S&P 500 companies scheduled to report, (6) Wednesday’s release of the May 1-2 FOMC meeting minutes, and (7) a light U.S. economic schedule with a focus on housing reports.

In Europe, the focus will mainly be on the new populist government in Italy, which could be approved by Italian President Mattarella early this week. The European markets will also be watching to see if the Trump administration wants to declare a trade truce with Europe, as well as China, ahead of the expiration next Friday (June 1) of Europe’s temporary exemption from U.S. steel and aluminum tariffs. Wednesday’s Eurozone May Markit PMI is expected to show a -0.2 point decline to 56.0, adding to April’s -0.4 point decline. Brexit negotiations will resume this week in Brussels with the main hitch still being the Northern Ireland border.

German Chancellor Merkel will visit China this week and will meet with President Xi on Thursday. Ms. Merkel said she will seek a free-trade ally in China this week, suggesting that she will be looking for allies to counter the Trump administration’s trade threats.

In Asia, the focus will mainly be on trade tensions and whether the June U.S.-North Korean summit will come off as planned. There are no Chinese economic reports this week and the Japanese economic calendar is light.

U.S. and China agree on “framework” for trade talks and to put trade war on hold — Treasury Secretary Mnuchin on Sunday said that, “We’re putting the trade war on hold. So right now, we have agreed to put the tariffs on hold while we try to execute the framework.” The White House said that last week’s U.S.-Chinese trade talks resulted in a “framework” for trade talks and that China agreed to “substantially reduce the trade deficit by increasing their purchases of goods.”

White House economic advisor Larry Kudlow first said that China agreed to reduce the U.S.-Chinese trade deficit by $200 billion but he then walked back that specific number after Chinese officials denied the $200 billion amount. There was apparently an agreement for China to boost its purchases of U.S. products in specific sectors such as agriculture and energy.

There is no way to tell how long the truce might last but the Trump administration has apparently agreed not to impose the 25% tariff on the $50 billion worth of Chinese goods. The 60-day public comment period for that tariff expires tomorrow (May 22), which means that the administration can implement that tariff anytime after tomorrow. In a sign of good faith, China announced that it was withdrawing its trade investigation of U.S. sorghum and would return the 179% deposit on U.S. sorghum imports that China has been collecting. As part of the deal, the Trump administration likely agreed to substantially soften its penalties on ZTE Corp, although there has been no confirmation as yet.

The truce was good news for the markets. President Trump can declare a victory for now due to China’s agreement to boost purchases of U.S. products, while reserving the right to revive his tariff threats at any time. The truce will undoubtedly last until after the planned June 12 U.S.-North Korean summit and possibly even until after the November U.S. mid-term elections. Republicans cannot afford to go into the mid-term elections with politically-key farm states under duress from Chinese agriculture tariffs.

There was also some positive news on NAFTA over the weekend after Treasury Secretary Mnuchin said that the Trump administration is focused on a good NAFTA deal, not on deadlines. That suggested that the administration has given up on a near-term NAFTA deal and is willing let a deal slip into next year’s Congress. House Speaker Ryan’s deadline of last week has now passed for getting a NAFTA deal done that could be approved by the House by year-end.

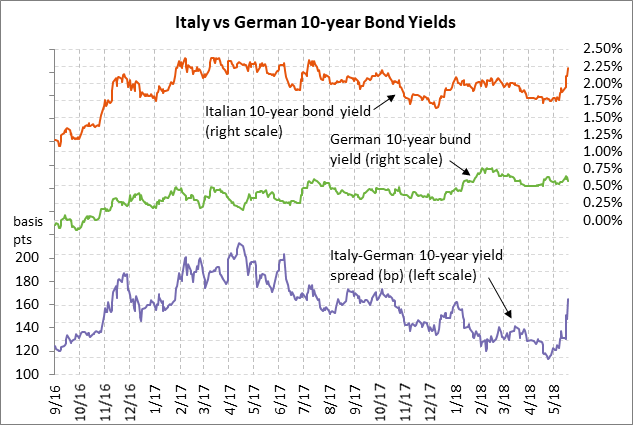

Italian populists are about to govern as bond risk measures surge — Italy’s Five Star and League parties are set to meet with President Mattarella as early as today to seek approval of their coalition to govern. The two parties over the weekend received the approval of their respective members with votes of more than 90% in favor.

The parties in their policy platform watered down their most controversial policies, but the markets nevertheless remain worried about their tendencies toward fiscal largesse and EU antagonism. The coalition government is clearly going to clash with EU members on budget deficits and national debt, although the Italian populists have at least pulled back from their talk in the past about seeking a public referendum about leaving the EU.

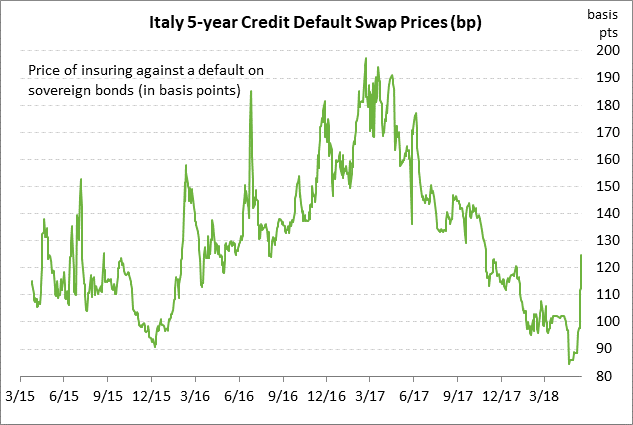

Due to concerns about the incoming populist government, the Italian 10-year bond yield has soared by more than 40 bp in the past three weeks and reached a 10-month high of 2.23% last Friday. The spread of the Italian 10-year yield over bunds last Friday climbed by another +17 bp to a 7-month high 165 bp. The 5-year Italian credit default swap, which is the cost of insuring against an Italian sovereign bond default, has soared by 40 bp in the past month and reached a 6-3/4 month high of 125 bp last Friday.