- FOMC is likely to boost the Fed-dot forecast for rate hikes

- Fed’s balance sheet drawdown will progressively speed up through year-end

- U.S. existing home sales expected to stabilize after 2-month drop

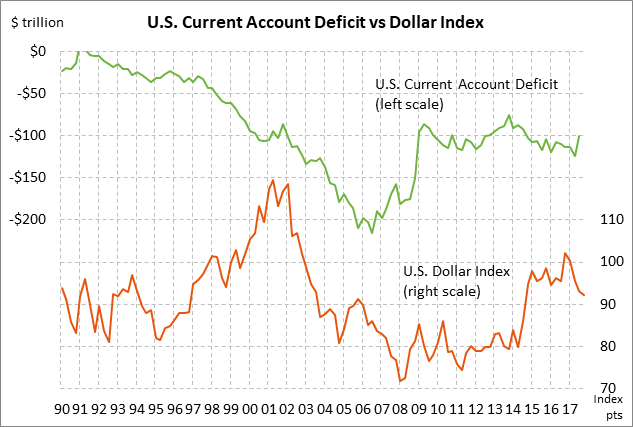

- U.S. current account deficit expected to widen to a 9-year high

- Markets are largely unconcerned as CR expires Friday

- Weekly EIA report

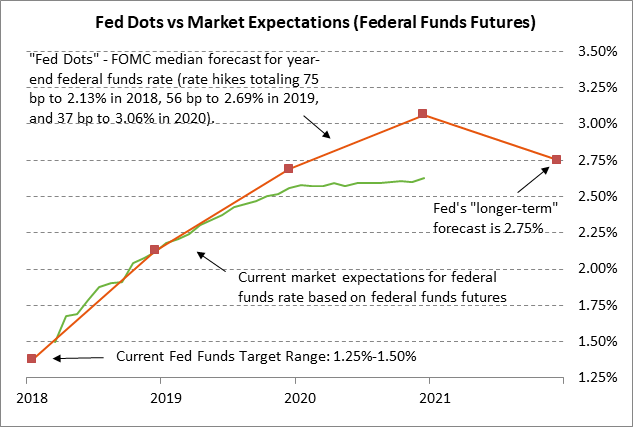

FOMC is likely to boost the Fed-dot forecast for rate hikes — Fed Chair Powell will hold his first press conference today at the conclusion of the 2-day meeting. The markets are discounting the odds at 100% for a +25 bp rate hike today to a new funds rate target of 1.50%/1.75%, according to the federal funds futures market.

The markets will also be watching the extent to which the language used by the FOMC in its post-meeting statement and by Fed Chair Powell in his press conference turns a bit more hawkish, and whether the Fed-dot forecasts for the funds rate are raised. For 2018, the FOMC member forecasts are tightly bunched around three rate hikes for the year, meaning it will be somewhat difficult for the median estimate to move higher. However, the median estimates for 2019 and 2020 could easily move higher since the current estimates are more widely spread out.

For 2018, the market is close to matching the Fed-dot forecast for three rate hikes totaling 75 bp. However, the market is undershooting the Fed dots for both 2019 and 2020. Specifically, for 2019, the market is discounting a further 47 bp of rate hikes in 2019, which is 9 bp less than the Fed-dot forecast of 56 bp (2.3 rate hikes). For 2020, the market is discounting only 7 bp of rate hikes, which is 30 bp less than the Fed-dot forecast of 37 bp (1.5 rate hikes).

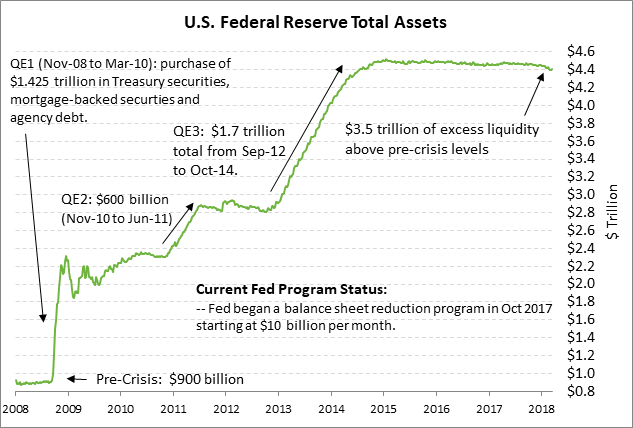

Fed’s balance sheet drawdown will progressively speed up through year-end — The Fed’s balance sheet drawdown program has so far been negligible and has been like “watching paint dry” as former Fed Chair Yellen promised. However, the maximum drawdown amount will increase from $20 billion per month in Q1 to $30 per month in Q2, $40 billion per month in Q3, and $50 billion per month in Q4 and thereafter. The program could therefore have an increasingly negative effect on the Treasury market as it ramps up during this year.

The Fed’s balance sheet has so far fallen by only about $48 billion (or 1%) since the program began last October. That decline is barely noticeable on the chart. The Fed has yet to announce how long its drawdown program will last, or the level the Fed is targeting for the final balance sheet level. The Fed’s balance sheet was near $900 billion before the QE programs started in 2007, but the Fed now needs a much larger balance sheet to account for the larger economy and higher money demand. There has been talk about a final balance sheet level of somewhere around $2.5 trillion, but the final level is highly dependent on how the Fed plans to conduct monetary policy in the future.

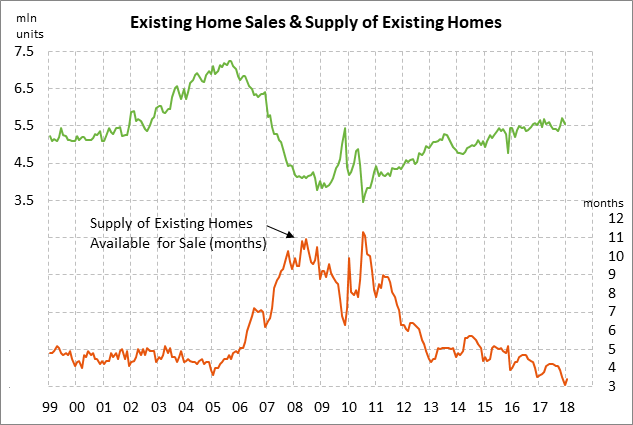

U.S. existing home sales expected to stabilize after 2-month drop — The market consensus is for today’s Feb existing home sales report to show a small +0.4% increase to 5.40 million, stabilizing after Jan’s -3.2% decline to 5.38 million. Despite a 2-month decline, existing home sales remain relatively strong and are only -5.9% below the 11-year high of 5.72 million units posted in Nov 2017. Home sales should continue to see general strength due to the strong economy and consumer confidence. However, there are some headwinds for home sales from high home prices and rising mortgage rates. The 30-year mortgage rate has risen sharply by about 40 bp in the past two months and is near a 4-year high at 4.44%.

U.S. current account deficit expected to widen to a 9-year high — Today’s Q4 current account deficit is expected to widen sharply to -$125.0 billion from -$100.6 billion in Q3. The expected deficit of -$125.0 billion would be a new 9-year high, taking out the current high of -$124.4 billion posted in Q2-2017. U.S. exports are in good shape due to the cheap dollar and the improved global economy but the deficit is widening anyway due to even stronger imports and higher petroleum prices. A new 9-year year high in the U.S. current account deficit today would be an unwelcome development at the White House.

Markets are largely unconcerned as CR expires Friday — The markets are largely unconcerned as the continuing resolution expires at midnight on Friday, threatening a government shutdown if new spending authority is not approved by Congress in time. The markets recognize that the measure will go down to the wire and that only a short government shutdown would occur, if any. There is a already a bipartisan agreement on top-line budget levels and Republicans and Democrats have narrowed their differences to a handful of issues.

Speaker Ryan on Tuesday said that he expects the House to vote on an omnibus spending bill on Thursday. That would mean that the Senate would have only Friday to approve the bill. In that case, a single Senator such as Rand Paul could slow consideration of the bill in the Senate long enough to force at least a one or two day government shutdown. Senator Paul last month already caused a few-hour government shutdown by throwing up obstacles to Senate consideration of the bill as a protest against high spending levels. To avoid that risk, Congress by Friday may pass a short continuing resolution to provide enough time for the full omnibus bill to get through Congress.

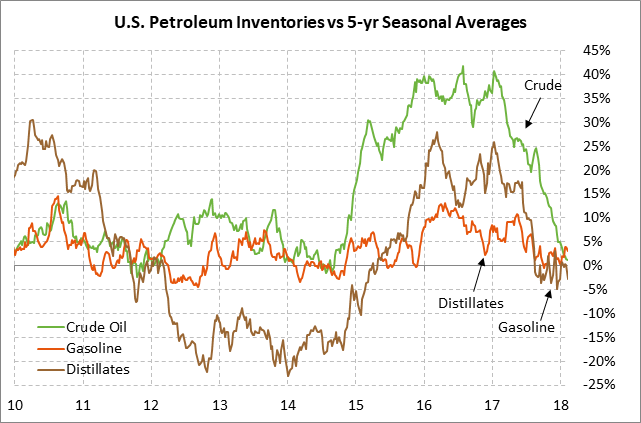

Weekly EIA report — The market consensus is for today’s weekly EIA report to show a +3.2 million bbl rise in U.S. crude oil inventories, a -2.5 million bbl drop in gasoline inventories, a -1.75 million bbl drop in distillate inventories, and an unchanged refinery utilization rate at 90.0%. Crude oil inventories have fallen sharply relative to the 5-year average in recent weeks and are now only +1.2% above that average, the tightest such level in more than 3 years. Meanwhile, gasoline inventories are mildly above average by +3.0% while distillate inventories are mildly below average by -2.7%. U.S. crude oil production in last week’s report rose by +0.1% w/w to a new record high of 10.381 million bpd, which is sharply higher by +14.0% y/y.