- Key meeting today may determine whether Mexican tariffs begin on Monday

- China so far gives Mnuchin the stiff-arm

- Stock market rallies sharply after Powell nods toward easier policy

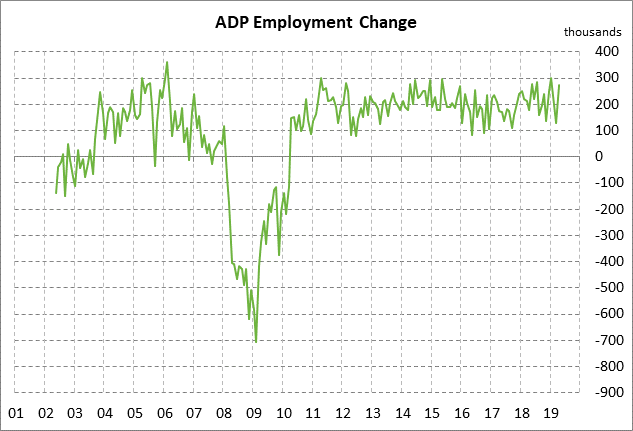

- ADP expected to show solid increase

- ISM non-manufacturing index expected to edge lower

Key meeting today may determine whether Mexican tariffs begin on Monday — Mexican Foreign Minister Ebrard is scheduled to meet today with U.S. Secretary of State Pompeo and other U.S. officials. Mexican officials have expressed optimism about reaching an agreement to avert the 5% U.S. tariff on all Mexican imports that is due to go into effect on Monday (June 10). Mr. Ebrard is already in Washington and said that his talks on Tuesday were “very useful” and that he sees an 80% chance of a deal before Monday.

However, President Trump on Tuesday seemed to imply that he has already decided to go ahead with Monday’s tariff. Speaking from London, Mr. Trump on Tuesday said that, “It’s more likely the tariffs go on and we’ll probably be talking during the time the tariffs are on.” That would be in line with Mr. Trump’s recent modus operandi of applying tariffs first and then negotiating after the opponent is already feeling some tariff pain. Mr. Trump also seems to increasingly view tariffs as a desirable goal in themselves as opposed to just a temporary negotiating lever.

Mr. Trump seems undeterred by opposition from Senate Republicans who held a lunch meeting yesterday and afterwards threatened to vote in favor of a resolution to block the Mexican tariffs. After the meeting, Senator Kevin Cramer (R-ND) was quoted by the Washington Post as saying that he thought there was enough Republican support to get a veto-proof resolution passed in the Senate to block the Mexican tariff. However, it is doubtful that there are enough House Republicans to override a veto in the House, meaning that President Trump probably does not have to worry about Congress blocking his Mexican tariffs.

China so far gives Mnuchin the stiff-arm — The U.S. seemed to be hoping that Treasury Secretary Mnuchin might be able to break the ice with a face-to-face meeting with Chinese officials at the 3-day G20 finance ministers meeting that begins this Friday in Fukuoka, Japan. However, Bloomberg reported on Tuesday that no official meeting has yet been set between Mr. Mnuchin and his Chinese counterparts, although U.S. and Chinese officials do expect to cross paths.

The Trump administration seems to be hoping that Mr. Mnuchin this weekend might be able to nail down a definitive meeting between Presidents Trump and Xi when they attend the G20 summit on June 28-29 in Osaka, Japan. A Trump-Xi meeting still seems likely to take place, although China appears to be giving the U.S. the cold shoulder so far on that meeting. The markets are hoping that a Trump/Xi meeting could get US/Chinese trade talks back on track with a promise from Mr. Trump to defer his threat of a 25% tariff on another $300 billion of Chinese goods.

By contrast, if a Trump/Xi meeting at the end of June does not happen, then the markets can assume that China is even more furious than they have let on in public and that China has no intention of giving Mr. Trump any concessions in the foreseeable future. If there is no Trump/Xi meeting, then the die would likely be cast for Mr. Trump to proceed with his 25% tariff on another $300 billion of Chinese goods.

China would then likely retaliate with a new round of penalty tariffs, the shut-down of Chinese exports of rare earth metals to the U.S., and the blacklisting of some high-profile U.S. companies doing business in China. If the next big round of trade blows occurs, then China might simply give up on US/Chinese trade talks and wait to see if Mr. Trump loses the election next November.

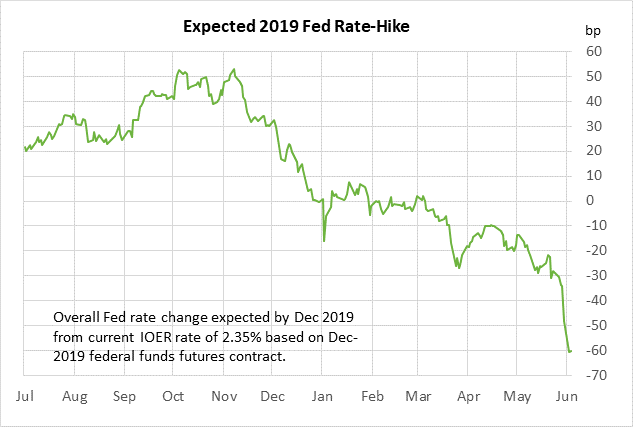

Stock market rallies sharply after Powell nods toward easier policy — The U.S. stock market apparently was not asking for much out of Fed Chair Powell since the S&P 500 index rallied by +2.14% on Tuesday. Mr. Powell didn’t even have to mention a “rate cut” or “easing” to spark that rally. He only had to state the obvious fact that the Fed is “closely monitoring” trade and other developments and “will act as appropriate to sustain the expansion.”

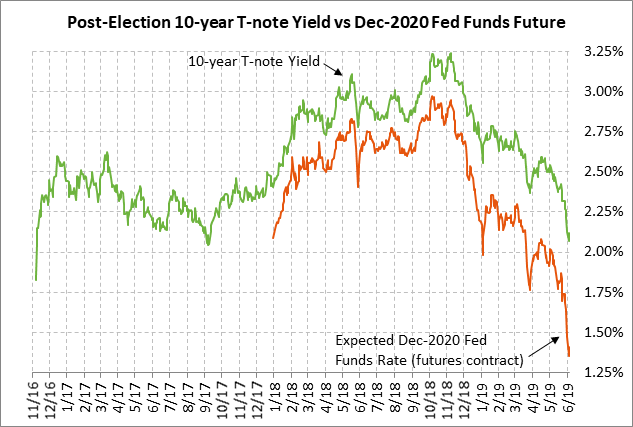

Nevertheless, the stock market rallied sharply on Tuesday on the idea that the Fed is at least open to a rate cut if the situation deteriorates, which the markets seem to expect. The fed funds market on Tuesday backtracked a little from Monday but the market is still expecting a total of -60 bp of rate cuts (2.4 cuts) by the end of 2019 and a total of -94 bp of rate cuts (3.8 cuts) by the end of 2020.

The 10-year T-note yield on Tuesday recovered somewhat from Monday’s 1-3/4 year low of 2.06% and closed the day +5.9 bp at 2.130%. T-note prices on Tuesday gained underlying support from Mr. Powell’s nod in the direction of easing. However, T-note prices fell on long liquidation pressure and on the sharp rally in stocks. In addition, Fed Vice Chair Clarida said on CNBC that the Fed will do what it needs to do but will not be “handcuffed” to financial market moves. That hinted that the Fed sees the recent market moves as far overdone.

ADP expected to show solid increase — The consensus is for today’s May ADP employment report to show an increase of +185,000, returning to more of a trend increase after the volatility seen in the previous two months. The ADP report showed a weak report in March of +129,00 but then recovered by +275,000 in April, producing a 2-month average of +202,000, mildly below the 12-month average of +218,000. Friday’s payroll report is expected to show a solid increase of +180,000 after April’s report of +263,000.

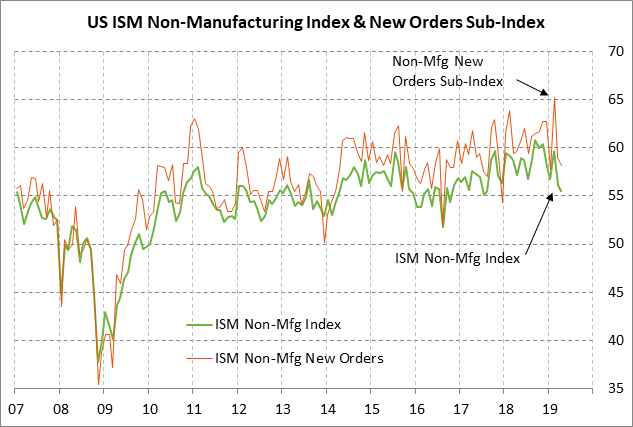

ISM non-manufacturing index expected to edge lower — Today’s May ISM non-manufacturing index is expected to show a small decline of -0.1 to 55.4, adding to April’s -0.6 decline to a 1-3/4 year low of 55.5. Monday’s ISM manufacturing index fell by -0.7 to a 2-1/2 year low of 52.1, illustrating deteriorating confidence in the manufacturing sector.