- Markets wait to see if US/Chinese trade talks survive

- Trump tariff hike would discourage any Fed easing

- Fed is looking towards today’s CPI report for inflation guidance

Markets wait to see if US/Chinese trade talks survive — The 2-day US/Chinese trade talks began late Thursday afternoon at 5PM ET with only 7 hours left until midnight when the Trump administration said it would raise the tariffs to 25% from 10% on $200 billion of Chinese goods.

There is a possibility that Chinese Premier Liu came to Washington with enough concessions to get President Trump to delay that tariff hike or conceivably even win a final agreement by the end of the talks today. However, the Trump administration seemed intent on going through with Thursday night’s tariff hike. Indeed, USTR Lighthizer has reportedly been telling some Republican Senators to expect the administration to go through with the tariff hike.

The markets today will obviously be very pleased if last night’s tariff hike was averted. However, if Trump administration went ahead with last night’s tariff hike, then there are two main questions: (1) will China break off the trade talks for some period of time, and (2) will President Trump make good on his threat to slap a 25% tariff on the remaining $325 billion of Chinese goods. President Trump would presumably allow today’s trade talks to conclude before announcing what he will do about his threat for a 25% tariff on $325 billion of Chinese goods. Based on precedent, Mr. Trump may announce a deadline for the imposition of that new tariff of perhaps 30, 60 or 90 days, thus keeping the pressure on China to negotiate an agreement.

For the markets, this week’s whiplash on the US/Chinese trade talks has been a very unwelcome development. Based on repeated assurances from President Trump and Mnuchin/Kudlow that the talks were going well, the markets had concluded that the talks could be wrapped up as soon as this week with an agreement. However, the markets received a rude awakening last weekend when President Trump viewed the last Chinese agreement revision as a measure to “break” the agreements made thus far, causing Mr. Trump to give China virtually no chance to back down before imposing the next round of tariffs. Mr. Trump successfully made clear that he is playing hardball, but it may also be the case that Chinese President Xi may have concluded that he simply can’t do business with Mr. Trump.

From China’s perspective, the best course going forward (assuming that the tariffs were raised last night) would be to do whatever it reasonably can to prevent or delay Mr. Trump from slapping a 25% tariff on the remaining $325 billion of Chinese goods. However, if Mr. Trump goes ahead with that nuclear move in short order, then China will have little reason to continue the trade talks. At some point, China may simply decide to absorb the tariffs and wait for the end of the Trump administration, however long that takes.

Another big question is the extent to which China will retaliate if the U.S. went ahead with the tariff hike last night. If China retaliates with minimal measures, then Mr. Trump might overlook the retaliation. However, if the retaliation is substantial, then Mr. Trump may well move ahead with the 25% tariff on $325 billion of Chinese goods. That nuclear move might finally force the Chinese concessions that the U.S. is demanding, but it could also finish the US/Chinese trade talks for the duration of the Trump presidency.

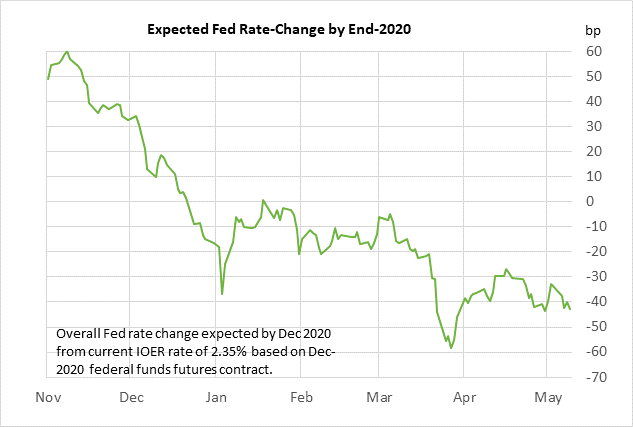

Trump tariff hike would discourage any Fed easing — Fed Chair Powell has given no indication that the Fed is even thinking about easing as its next move. Indeed, the Fed-dots are predicting no rate change this year and a +25 bp rate hike next year. The Fed clearly doesn’t agree with the market consensus for a -43 bp Fed rate cut by the end of 2020 based on the Dec 2020 federal funds futures contract.

If President Trump went ahead with last night’s tariff hike and China retaliates, then the U.S. and Chinese economies will have to deal with a big step-up in tariff levels. The total U.S. tariff amount would nearly double to $62.5 billion from the current $32.5 billion. Atlanta Fed President Bostic yesterday warned that a hike in tariffs to 25% means that “you are going to start to see that passed through into the consumer space.” The tariff impact on higher inflation would start to become dramatic if President Trump slaps a 25% tariff on the remaining $325 billion of Chinese goods, which in large part are consumer goods. To the extent that tariffs push up inflation, the Fed will be even less willing to cut rates even if the economy weakens in response to the tariffs.

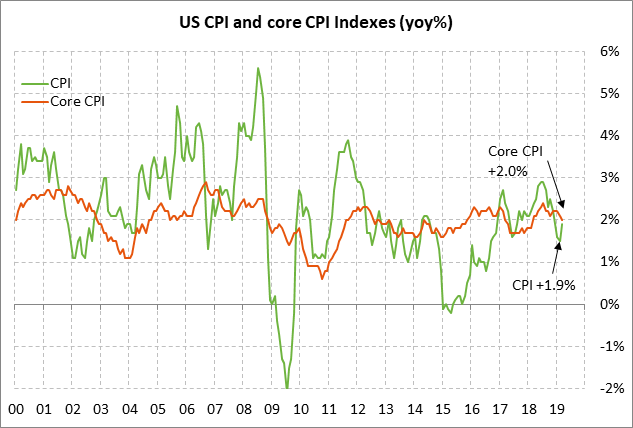

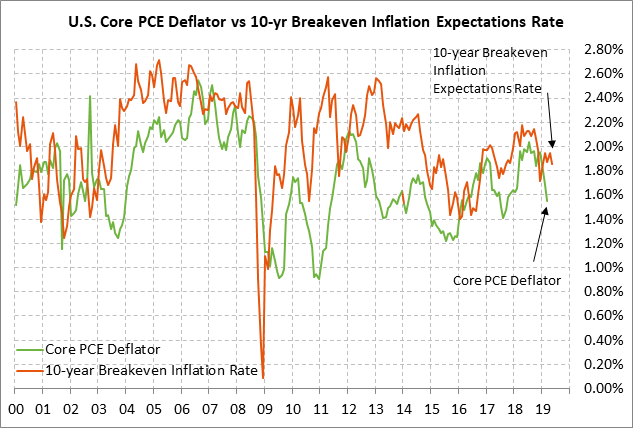

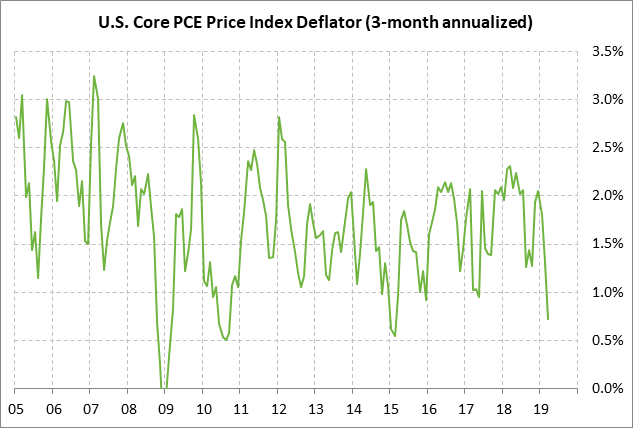

Fed is looking towards today’s CPI report for inflation guidance — The Fed will be watching today’s CPI report to see whether it supports Fed Chair Powell’s recent view that inflation is currently low mostly for transitory reasons. There is little doubt that inflation is currently seeing a dip since the Fed’s preferred inflation measure, the PCE deflator, was at only +1.5% in March and the core deflator was at +1.6%, both well below the Fed’s 2.0% inflation target. On a 3-month annualized basis, the March PCE deflator was even weaker at +1.0% and the core deflator was at a 4-year low of +0.7%.

In any case, the consensus is for today’s April headline CPI to rise to +2.1% y/y from March’s +1.9% and for the core CPI to rise to +2.1% from March’s +2.0%. Yesterday’s April PPI report of +2.2% headline and +2.4% core was 0.1 point weaker than market expectations of +2.3% and +2.5%, respectively, and were unchanged from March.

Meanwhile, the 10-year breakeven inflation expectations rate on Thursday fell to a new 6-week low and closed the day down -1.0 bp at 1.855%. The 10-year breakeven rate in the past two weeks has fallen sharply by -15 bp from the late-April 5-1/4 month high of 1.98% to Thursday’s 6-week low of 1.83%. That decline has been due to lower crude oil prices and concerns about global economic growth caused by the increased US/Chinese trade tensions.