- US/EU trade tensions possible today with Lighthizer/Malmstroem meeting

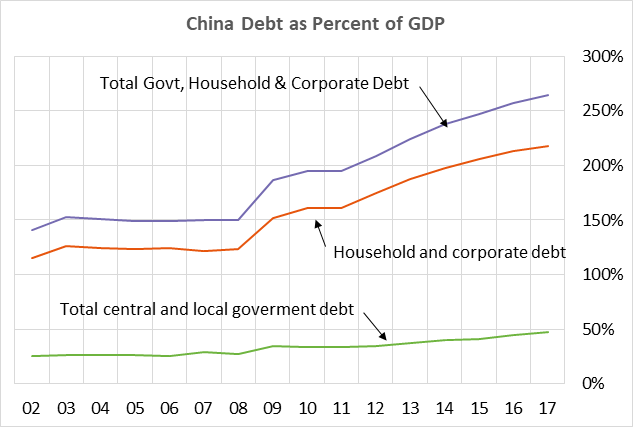

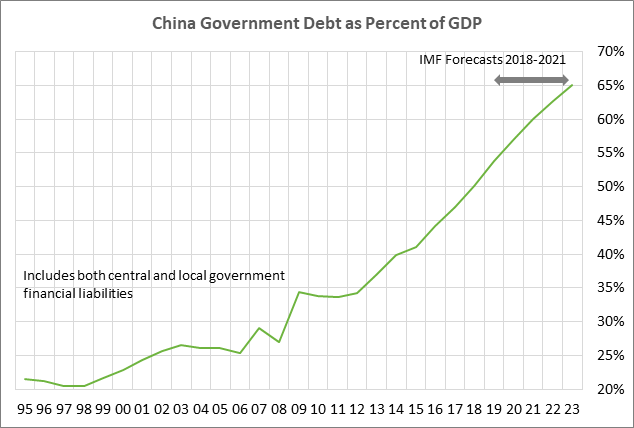

- China’s tax cut is another attempt to boost the economy without a new surge in debt

- UK/EU talks continue today after no progress on Tuesday

- Bank of Canada expected to leave policy unchanged

- U.S. ADP employment expected to remain firm

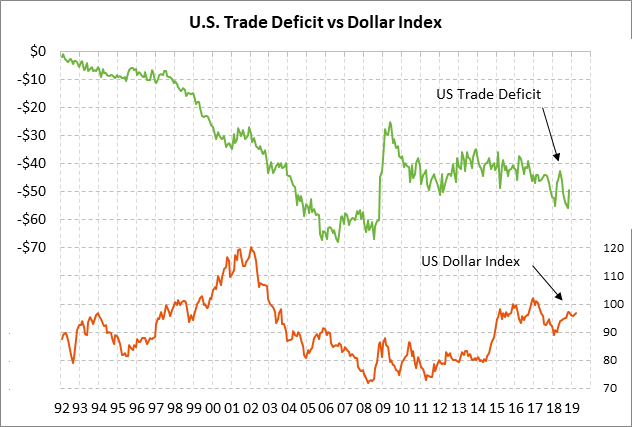

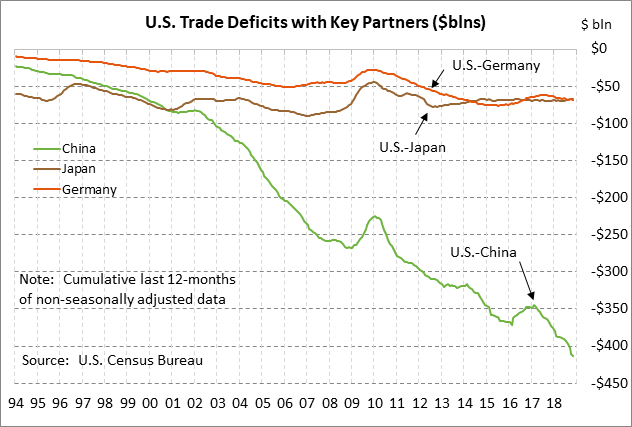

- U.S. trade deficit expected to expand sharply

US/EU trade tensions possible today with Lighthizer/Malmstroem meeting — EU Trade Commissioner Cecilia Malmstroem is scheduled to meet today with USTR Lighthizer in Washington to discuss US/EU trade issues. The US/EU trade talks that were agreed upon last year have yet to officially start because negotiators are waiting for the EU parliament to give negotiators their official mandate.

Today’s Lighthizer/Malmstroem meeting could provide an occasion for President Trump to issue new warnings that he might slap tariffs on European autos since the US/EU trade talks have been slow to start and since the EU continues to refuse to accede to U.S. demands that agriculture be involved in the trade talks in addition to industrial products and autos.

Separately, the auto industry continues to call on the Trump administration to make public the Commerce Dept’s recent report to the White House about whether President Trump should slap tariffs on imported autos on national security grounds. The report likely does, in fact, recommend tariffs on imported autos, in line with Mr. Trump’s view.

China’s tax cut is another attempt to boost the economy without a new surge in debt — China continues to try to thread the needle by implementing targeted fiscal and monetary measures to boost the economy without causing a new surge in debt that threatens the Chinese economy down the road. The Chinese economy is already on its way to a potential debt crisis with total Chinese debt (combined government, corporate, and household) at 271% of GDP in 2018, up by 80% from the 150% level seen in 2007 before the global financial crisis.

The Chinese government on Tuesday announced a big $300 billion tax cut, designed mainly to help the manufacturing, transportation and construction sectors. The tax cuts and other fiscal stimulus measures will boost the government’s budget deficit to 2.8% of GDP from 2.6% in 2018. The government also suggested that further targeted monetary policy stimulus measures will be forthcoming such as more cuts in the bank required-reserve ratio, which would free up more banking lending capacity.

The Chinese government is trying to stabilize the economy after the loss of momentum seen over the past year. The slower economy has been due to the US/Chinese trade war but it has also been due to long-term secular factors such as a decline in Chinese growth towards the more normal rates seen in large developed economies. China’s government cannot stimulate its way to extraordinary growth levels above 6% forever and must accept a slower growth rate. In that vein, the Chinese government on Tuesday met market expectations by adopting a 2019 GDP target of 6.0-6.5%, down from the 2018 target of about 6.5% and the lowest growth target that the Chinese government has ever set. The cut in the GDP target was modest but was at least in a realistic and prudent direction.

UK/EU talks continue today after no progress on Tuesday — The talks on Tuesday between UK and EU officials on the Irish backstop did not go well, according to an EU official quoted by Bloomberg. The talks will nevertheless continue on Wednesday. UK officials early Tuesday warned that there wasn’t likely to be a breakthrough in Tuesday’s talks but that there was hope for progress later in the week. Prime Minister May might travel to Brussels this weekend for further negotiations or perhaps to close a deal.

UK Attorney General Cox and Brexit Secretary Barclay are in Brussels trying to get enough concessions on the Irish backstop to get Parliament to vote in favor of Prime Minister May’s Brexit separation agreement next Tuesday (March 12). If Parliament instead votes against Ms. May Brexit bill, then Parliament is expected to vote against a no-deal Brexit next Wednesday and then vote on Thursday to extend the March 29 Brexit deadline, thus preventing a no-deal Brexit.

Bank of Canada expected to leave policy unchanged — The Bank of Canada at its meeting today is unanimously expected to leave its policy rate unchanged at 1.75%. The Bank of Canada’s guidance still favors further rate hikes based on expectations for a strong enough economy to hit capacity constraints and cause inflation. However, the BOC today will be forced to move in a more dovish direction due to the unexpectedly large slowdown in the Canadian economy in late 2018. Last Friday’s Q4 GDP report of +0.1% q/q and +0.4% (q/q annualized) was much weaker than expected and showed broad-based weakness.

The Bank of Canada today is likely to turn to more dovish wording in its guidance. There is even an outside chance that the bank might drop its reference to higher rates altogether, which would be an unexpectedly dovish outcome that would likely send the Canadian dollar lower. The guidance from the last meeting said that the “policy interest rate will need to rise over time,” with a pace depending on the oil and housing markets and trade tensions.

U.S. ADP employment expected to remain firm — The consensus is for today’s Feb ADP employment report to show another solid increase of +190,000, but down from Jan’s strong increase of +213,000 and the 12-month average of +209,000. Friday’s Feb payroll report is expected at +181,000 after Jan’s strong report of +304,000. U.S. job growth remains surprisingly strong.

U.S. trade deficit expected to expand sharply — The consensus is for today’s Jan trade deficit to expand to a new 10-year high of -$57.9 billion from Dec’s -$49.3 billion. U.S. trade flows continue to be distorted by U.S. tariffs and retaliatory tariffs. In Nov, exports were up +3.7% y/y while imports were up +3.2% y/y. Today’s Jan trade report was delayed by the recent U.S. government shutdown.